Policy Statement

Financial Services Authority

October 2012

Mortgage Market Review

Feedback on CP11/31 and final rules

PS12/16

«««

PS12/16

Mortgage Market Review: Feedback on CP11/31 and final rules

© The Financial Services Authority 2012

Contents

Abbreviations used in this paper 3

1. Introduction 5

2. Advice 12

3. Transitional arrangements 16

4. High net worth and business lending 22

Annex 1: Detailed feedback on CP11/31

Annex 2: Table of changes from the draft rules to the nal rules

Annex 3: Cost benet analysis

Annex 4: List of non-condential respondents to CP11/31

Annex 5: Equality Impact Assessment (EIA)

Appendix 1: Made rules (legal instrument):

• Made rules– Mortgage Market Review (Conduct of

Business) Instrument 2012

• Made rules – Prudential sourcebook for Mortgage and

Home Finance Firms, and Insurance Intermediaries

(Non-Bank Lenders) Instrument 2012

This Policy Statement reports on the main issues arising from Consultation Paper 11/31

(Mortgage Market Review: Proposed package of reforms) and publishes final rules.

Please address any comments or enquiries to:

Lynda Blackwell

Conduct Policy Division

Financial Services Authority

25 The North Colonnade

Canary Wharf

London E14 5HS

Telephone:

020 7066 8794

Email: [email protected].uk

Copies of this Policy Statement are available to download from our website –

www.fsa.gov.uk. Alternatively, paper copies can be obtained by calling the FSA

order line:

0845 608 2372.

PS12/16

Mortgage Market Review: Feedback on CP11/31 and final rules

Financial Services Authority 3October 2012

Abbreviations

used in this paper

BIPRU

Prudential sourcebook for Banks, Building Societies

and Investment Firms (FSA Handbook)

CBA

Cost benet analysis

CCA

Consumer Credit Act

CP

Consultation Paper

CRD

Capital Requirements Directive

DSR

Debt Service Ratio

EIA

Equality Impact Assessment

ESIS

European Standardised Information Sheet

EU

European Union

FCA

Financial Conduct Authority

FPC

Financial Policy Committee

FSA

Financial Services Authority

FSB

Financial Stability Board

FSCP

Financial Services Consumer Panel

FSMA

Financial Services and Markets Act 2000

FTB

First-time Buyer

HPP

Home Purchase Plan

IDD

Initial Disclosure Document

PS12/16

Mortgage Market Review: Feedback on CP11/31 and final rules

Annex X

4 Financial Services Authority October 2012

IRB

Internal Rating Based Model

HNW

High net worth

HOLD

Home Ownership for people with Long-term Disabilities

KFI

Key Facts Illustration

LTV

Loan-to-value (ratio)

MCD

Mortgage Credit Directive

MCOB

Mortgages and Home Finance: Conduct of Business

sourcebook (FSA Handbook)

MIPRU

Prudential sourcebook for Mortgage and Home Finance Firms,

and Insurance Intermediaries (FSA Handbook)

MMR

Mortgage Market Review

PERG

Perimeter Guidance Manual (FSA Handbook)

PRA

Prudential Regulation Authority

RDR

Retail Distribution Review

RAO

The Financial Services and Markets Act 2000 (Regulated

Activities) Order 2001

RTB

Right-to-buy

SRB

Sale and rent back

SVR

Standard Variable Rate

SYSC

Senior Management Arrangements, Systems and Controls

(FSA Handbook)

TPA

Third Party Administrator

PS12/16

Mortgage Market Review: Feedback on CP11/31 and final rules

Financial Services Authority 5October 2012

1

Introduction

1.1 In December 2011, we published our proposed package of reforms for the mortgage market

together with a cost benefit analysis (CBA) setting out our best estimates of the impact of

our proposals (CP11/31 Mortgage Market Review: Proposed package of reforms

1

).

1.2 This Policy Statement reports on the responses to that consultation and the decisions we

have reached.

What does this Policy Statement contain?

1.3 This Policy Statement contains feedback on the responses we received to CP11/31. The

main body highlights the key issues respondents raised about the proposals in CP11/31

and the decisions we have made as a result.

1.4 There are a number of annexes and an appendix:

• Annex 1 summarises the feedback we received to the policy questions asked in

CP11/31 and our policy response;

• Annex 2 summarises the main changes made to the draft rules in CP11/31;

• Annex 3 restates the high-level CBA conclusions from CP11/31 and provides a

regional breakdown of the impacts;

• Annex 4 lists the non-confidential respondents to CP11/31;

• Annex 5 contains the Equality Impact Assessment; and

• Appendix 1 contains the amendments being made to the FSA’s Handbook.

2

1 CP11/31, Mortgage Market Review: Proposed package of reforms, (December 2011): www.fsa.gov.uk/static/pubs/cp/cp11_31.pdf

2 Mortgage Market Review (Conduct Of Business) Instrument 2012 and Prudential Requirements For Non-Deposit Taking Lenders

Instrument 2012

PS12/16

Mortgage Market Review: Feedback on CP11/31 and final rules

Annex X

6 Financial Services Authority October 2012

1.5 We have also published separately an update to the Data Pack

3

, which was published as a

supplement to CP11/31.

Who should read this Policy Statement?

Firms

1.6 You should read this Policy Statement if you are:

• a lender or other home finance provider;

• a home finance administrator; or

• a firm that advises on or arranges mortgages or other home finance products.

If you are a body that represents any of these firms, this Policy Statement will also be of

interest to you.

Consumers

1.7 You should read this Policy Statement if:

• you have a mortgage or other home finance product; or

• you are planning to take one out.

If you are a body that represents consumers or an interest group representing those with

protected characteristics, this Policy Statement will also be of interest to you.

4

Outcome of our consultation

1.8 Responses to our consultation have been positive overall, with the industry welcoming the

less prescriptive approach we have taken to the responsible lending requirements and

acknowledging that the latest package would help achieve the MMR’s overall aim of

ensuring continued access to the mortgage market for the vast majority of customers who

can afford it, while addressing the tail of poor mortgage lending seen in the past.

1.9 The entire final MMR package is summarised in Table 1 at the end of this chapter. We are

taking forward, substantively unchanged, the majority of the proposals consulted on in

CP11/31. This includes the removal of the non-advised sales process, the strengthened

arrears charging rules, and the three key elements of the responsible lending reforms, i.e.

3 MMR Data Pack, (October 2012): www.fsa.gov.uk/static/pubs/cp/mmr-datapack2012.pdf

4 The protected characteristics are age, disability, gender, pregnancy and maternity, race, religion and belief, sexual orientation

and transgender.

PS12/16

Mortgage Market Review: Feedback on CP11/31 and final rules

Financial Services Authority 7October 2012

• The affordability assessment: a lender must verify income and be able to demonstrate

that the mortgage is affordable taking into account the borrower’s net income and, as a

minimum, the borrower’s committed expenditure and basic household expenditure.

• The interest rate stress test: the lender must also take account of the impact on

mortgage payments of market expectations of future interest rate increases.

• The interest-only rules: the lender must also assess affordability on a capital and

interest basis, unless there is a clearly understood and believable alternative source

of capital repayment.

1.10 We are also proceeding with the enhanced prudential requirements for non-deposit taking

lenders (‘non-banks’). In the feedback, respondents expressed a preference for standalone

rules for non-banks rather than cross-referencing to the relevant existing rules for banks.

5

The rules made by the FSA Board are not written on a standalone basis and maintain the

cross-referencing to the banking rules. However, we recognise that the banking rules,

derived from EU legislation, can be complex and difficult to navigate and we will therefore

continue to consider ahead of implementation how the regime could be made more

accessible, while preserving delivery of the policy outcomes consulted on in CP11/31.

1.11 Chapters 2 to 4 focus on those conduct areas where we have rethought our approach in

light of the feedback. Those areas are:

• Advice (Chapter 2): where we clarify what we understand by regulated advice and

explain that we are changing our approach to contract variations by allowing them to

be completed without the need for advice, provided there is no increase in the amount

outstanding under the mortgage.

• The transitional rules (Chapter 3): where we explain our changed approach in

allowing lenders to make their own decisions about whether to make exceptions to the

responsible lending rules provided there is no increase in the amount outstanding under

the mortgage.

• Our approach to high net worth and business lending (Chapter 4): where we explain

our decision not to provide a complete carve-out from the MMR proposals but instead

to provide a tailored, higher-level approach for both.

1.12 We have made one other substantive change which we explain in our response to Q14 in

Annex 1. We are requiring lenders to keep responsible lending records for the period the

mortgage remains with the lender, and not just for three years, as consulted on in CP11/31.

5 The relevant prudential rules for banks are set out in the Prudential sourcebook for Banks, Building Societies and Investment Firms

(BIPRU), which forms part of the FSA Handbook: http://fsahandbook.info/FSA/html/handbook/BIPRU

PS12/16

Mortgage Market Review: Feedback on CP11/31 and final rules

Annex X

8 Financial Services Authority October 2012

1.13 Given the extensive consultation with the market previously

6

and the extent of consensus

reached, the detail and background to the majority of the MMR reforms is not repeated in

this Policy Statement. Detailed feedback to CP11/31, together with our policy response is in

Annex 1. We have also summarised in Annex2 the non-material rule changes made in light

of responses and our further internal review.

Cost benefit analysis

1.14 Respondents to the CBA included in CP11/31 felt that the estimated size of the impacts of

the responsible lending proposals appeared reasonable. Annex 3 restates the high-level CBA

conclusions and provides, as requested in feedback, a regional breakdown of the impacts.

1.15 In relation to the advice proposals, a number of respondents felt that we had underestimated

the compliance costs of the removal of the non-advised sales process. We have updated our

compliance cost estimate to reflect the clarifications and changes discussed in Chapter 2.

The updated compliance cost estimate is in Annex 3.

Equality and diversity implications of the MMR

1.16 The feedback to CP11/31 confirmed our analysis that none of the MMR proposals directly

discriminate against any protected groups.

7

There are, however, some elements of our

responsible lending, distribution and disclosure and niche market proposals that could

cause adverse effects and possible inadvertent indirect discrimination. The detail of this and

the mitigants we propose are set out in the Equality Impact Assessment at Annex 5.

EU and international developments

1.17 In finalising our rules, we continue to pay close attention to impending European legislation.

The Directive on Credit Agreements Related to Residential Property, known commonly as

the Mortgage Credit Directive (MCD), is at an important stage. Both Council (representing

Member States) and Parliament have now adopted views on the proposed Directive. This

has allowed three-way negotiations involving the Commission, Council and Parliament to

begin. Agreement through these discussions (known as a ‘trilogue’) would pave the way for

the legislation. Failing that, the proposal would go through a second reading in Parliament,

which might significantly extend the time before the Directive becomes law.

6 DP09/3, Mortgage Market Review, (October 2009): www.fsa.gov.uk/pubs/discussion/dp09_03.pdf

CP10/2, Mortgage Market Review: Arrears and Approved Persons, (January 2010): www.fsa.gov.uk/pubs/cp/cp10_02.pdf

CP10/16, Mortgage Market Review: Responsible Lending, (July 2010): www.fsa.gov.uk/pubs/cp/cp10_16.pdf

CP10/28, Mortgage Market Review: Distribution & Disclosure, (November 2010): www.fsa.gov.uk/pubs/cp/cp10_28.pdf

7 See footnote 4 on page 7.

PS12/16

Mortgage Market Review: Feedback on CP11/31 and final rules

Financial Services Authority 9October 2012

1.18 We have been engaging with the European institutions over the possibility of a directive for

many years. They have welcomed learning of the UK regulatory experience and the depth

of our MMR research and analysis.

1.19 Many parts of the Commission’s original proposal closely match MMR concerns, including

the need for greater professionalism among firms, having close regard to the consumer’s

interests, and the need for a robust assessment of individual affordability. The changes we

are making in these areas are in line with the proposed Directive.

1.20 In one or two respects the proposed legislation is less closely aligned with the UK proposed

regulatory approach. One of these is the scope, which in the form originally proposed by

the Commission would apply a standard approach to a great many niche mortgage markets

(such as buy-to-let, bridging, high net worth and shared equity). Not all of these are

markets that we currently regulate.

1.21 A second clear difference is the European proposal’s greater focus on disclosure, which is

likely to mean that some further rule change will be needed to introduce extra disclosure

requirements. This does not mean we should not proceed with our MMR approach of

re-focusing our disclosure regime on key messages, but firms should be aware that further

information may be required to be given on top of this in future. In other respects, we

consider that we now know enough about the likely form of the directive to finalise the

MMR rules.

1.22 Our revised rules will also ensure UK regulation reflects key Financial Stability Board (FSB)

Principles for sound mortgage underwriting.

8

The first two of these FSB Principles deal

with assessing affordability. The MMR changes will mean that these Principles – on income

verification and a reasonable debt service coverage – are clearly met. MMR requirements

for lenders to have clearly documented responsible lending policies also help deliver FSB

Principles requiring an implementation and supervisory framework.

1.23 As with the Directive, the MMR analysis has allowed us to contribute to the Principles, and

ensure the approaches align.

Implementation timetable

1.24 Our Board has now made the rules in Appendix 1. With the exception of MCOB11.8.1E

(discussed further below), the rules will come into effect on 26 April 2014, in 18 months’ time.

1.25 We have given careful consideration to all of the feedback received about the implementation

timetable. We recognise that the cumulative impact of the MMR will lead to significant

changes on the part of firms to policies, processes, systems and staff training and this will

make the usual 12-month period challenging for firms, particularly the smaller firms.

8 FSB Principles for Sound Residential Mortgage Underwriting Practices, Financial Stability Board, (April 2012):

www.financialstabilityboard.org/publications/r_120418.pdf

PS12/16

Mortgage Market Review: Feedback on CP11/31 and final rules

Annex X

10 Financial Services Authority October 2012

1.26 We have also had regard to current market conditions. We concluded in CP11/31 that with

subdued conditions persisting in the mortgage market, both the micro and macroeconomic

impact of the MMR is small. This remains valid given the housing market conditions.

Allowing an extra six months for implementation will not introduce significant consumer

protection risks. Therefore we are giving firms 18 months to implement the MMR reforms.

1.27 MCOB11.8.1E, however, comes into effect now (on 26 October 2012). This is a new

evidential provision aimed at protecting those borrowers who find themselves ‘trapped’

with their current lender. We are switching this provision on with immediate effect as it is

aimed at protecting not only those borrowers who may find themselves trapped in future

following the implementation of the MMR, but also those borrowers who find themselves

trapped today because they do not meet current tightened lending criteria. This is discussed

more fully in our response to Q16 in Annex 1.

UK regulatory reform

1.28 The FSA Board has made the rules in Appendix 1, which contain references to the FSA, to

current UK financial services legislation and to other parts of the existing FSA Handbook.

These references will need to be reviewed and updated to reflect the assumption of

responsibility for financial services regulation by the Financial Conduct Authority (FCA)

and the Prudential Regulation Authority (PRA) in 2013, and to reflect any other relevant

amendments to the Financial Services and Markets Act 2000 (FSMA) and to the current

FSA Handbook as a result of UK regulatory reform.

1.29 Updated provisions will be made by the Boards of the FCA and PRA when they acquire

their legal powers.

Next steps

1.30 We are now planning a firm engagement programme for the implementation period, to help

firms understand the MMRreforms, encourage firms to carefully address any systems

changes that may be needed as a result of them, and to keep firms informed of the next

steps in our implementation strategy.

1.31 We also intend to conduct a formal review of the impact of our proposals not more than

five years after implementation.

PS12/16

Mortgage Market Review: Feedback on CP11/31 and final rules

Financial Services Authority 11October 2012

Table 1 – Summary of the MMR regulatory reform package

Mortgage Market Review

Key proposals consulted on and position unchanged

Responsible lending

Lender responsible for affordability checks.

Income to be veried in all cases.

As a minimum, committed and basic essential expenditure to be taken into account.

Stress testing against future interest rate increases.

Interest-only where credible repayment strategy.

Distribution

All interactive sales (e.g. face to face and telephone) advised, except where the customer is a mortgage

professional, or high net worth mortgage customer

9

, or business borrower

10

, where execution-only optional.

Execution-only allowed for non-interactive sales (e.g. internet and postal).

Requirement on intermediaries to assess affordability removed.

Every seller required to hold a relevant mortgage qualication.

Firms must act in the customer’s best interests.

Disclosure

IDD replaced with a requirement for rms to disclose ‘key messages’ to the customer.

The ‘trigger points’ for presentation of the KFI changed to reduce information overload for customers.

Arrears management

The number of times fees for missed payments can be charged limited.

The arrears charges and forbearance rules widened to cover all payment shortfalls.

The costs which can and cannot be recovered through arrears charges claried.

Lenders prevented from removing concessionary rates because of payment problems.

Non-deposit taking mortgage lenders (non-banks)

Risk-based capital requirement.

Increase in quality of capital.

High-level systems and controls to manage liquidity risk.

Application on a solo-basis and not to rms in run-off.

Key proposals consulted on and position reconsidered

Responsible lending

Transitional arrangements (see Chapter 3).

Record-keeping requirements (see Q14 Annex 1).

Distribution

Need for advice in relation to post-contract variations (see Chapter 2).

High net worth mortgage customers and business lending

Tailored regulatory approach recognising particular lending characteristics (see Chapter 4).

9 The definition of high net worth mortgage customer has been amended. See Chapter 4.

10 Business borrowers have been added as another group who can opt-out in the light of the feedback to CP11/31 (see Chapter 4)

PS12/16

Mortgage Market Review: Feedback on CP11/31 and final rules

Annex X

12 Financial Services Authority October 2012

2

Advice

Advised sales

2.1 A summary of the feedback to all of the questions asked about distribution in CP11/31 and

our policy responses are set out in Annex 1.

2.2 In this chapter, we consider two particular issues raised in the feedback:

• the boundary between providing information and giving advice; and

• advising on contract variations.

2.3 This is an area where we have revised our approach in light of the feedback to CP11/31

11

and our subsequent discussions with respondents.

Boundary between information provision and regulated advice

2.4 In CP11/31 we proposed removing the non-advised sales process and requiring that sales

involving some form of ‘interactive dialogue’ between the firm and the customer should

generally be advised.

2.5 This approach was welcomed by intermediaries and most consumer groups. However, it

was a source of concern for some lenders and their representatives.

2.6 It is clear both from feedback to CP11/31 and our subsequent discussions with firms that

there has been a misunderstanding about the scope of our advice proposals. Some firms

interpreted our proposals as meaning that every customer conversation would be construed

as providing regulated advice and therefore subject to our advice rules.

2.7 We recognise that this would have major implications for firms who use unqualified

‘pre-screeners’ to gather background information and provide general information to

11 CP11/31, Mortgage Market Review: Proposed package of reforms, (December 2011): www.fsa.gov.uk/static/pubs/cp/cp11_31.pdf

PS12/16

Mortgage Market Review: Feedback on CP11/31 and final rules

Financial Services Authority 13October 2012

customers prior to any sale commencing, as those ‘pre-screeners’ would need to be

appropriately trained and qualified.

2.8 We did not intend that every conversation with a customer would be subject to our advice

rules. The Regulated Activities Order

12

defines what regulated mortgage advice is, i.e.

advice on the merits of the customer entering into (or varying the terms of) a particular

regulated mortgage contract or contracts. As a result of this, our view is, and always has

been, that where a firm steers a customer towards particular identifiable products that the

customer could enter into, that is regulated advice. It is perfectly possible for a firm to have

a discussion about mortgage products in general or to gather information about the

customer’s general mortgage needs, without that being regulated advice.

2.9 The Perimeter Guidance on regulated activities connected to mortgages (PERG)

13

explains

the distinction. Given the confusion about the boundary apparent from the feedback to

CP11/31, we propose to review PERG over the course of the next year. The aim would be

to ensure that any changes considered appropriate following that review would be made in

time to be implemented alongside the MMR rules.

Contract variations by lenders

2.10 The biggest challenge to our advice proposals concerned the impact on contract variations

undertaken by lenders, such as rate switches, further advances, amending the term and

amending the repayment type. Where we refer to contract variations we also mean new

contracts with the existing lender that have the same effect.

2.11 Lenders and their trade bodies were concerned that all contract variations would be

captured by the advice requirements and that this contradicted the near-final Approved

Persons rules.

14

These rules explicitly exclude lender staff involved in these transactions

from being Approved Persons where there is no additional borrowing. The concern was

that under our advice proposals, these individuals would be required to give advice, but

would not be approved to do so.

2.12 We agree that it would be inappropriate for this to be the case and therefore we have

amended our approach to bring it into line with the Approved Persons near-final rules.

We think that it is appropriate that purely administrative contract variations are

undertaken on an execution-only basis, where the total sum outstanding under the

mortgage will not increase. Where the total sum outstanding will increase, for example

where there is a further advance, advice will be required.

12 The Financial Services and Markets Act 2000 (Regulated Activities) (Amendment) (No. 1) Order 2003:

www.legislation.gov.uk/uksi/2003/1475/article/13/made

13 http://fsahandbook.info/FSA/html/handbook/PERG/4

14 PS10/9, Mortgage Market Review – Arrears and Approved persons – Including feedback to CP10/2, (July 2010):

www.fsa.gov.uk/pubs/policy/ps10_09.pdf

PS12/16

Mortgage Market Review: Feedback on CP11/31 and final rules

Annex X

14 Financial Services Authority October 2012

2.13 In relation to rate switches (including retention deals), we believe that requiring advice

across all interactive channels is not a proportionate approach and therefore execution-only

sales should be permitted in some circumstances.

2.14 For example, where a borrower is coming to the end of their current deal and the firm has

written to them outlining all available products (without steering the borrower towards any

of those products). The borrower can select the product they want and send the instructions

back to the lender to make the change.

2.15 However, some borrowers may wish to complete the switch by telephone or in a branch.

Our general approach would not allow this as a sale over the telephone or in a branch is

an interactive sale and therefore advice would need to be given. However, our view is that

where it is a simple product switch and nothing more, it would be acceptable for the lender

to act on the borrower’s instructions over the telephone, or in the branch, and proceed on

an execution-only basis.

2.16 If the discussion with the borrower goes beyond simply acting on their instructions,

however, it would become an advised interactive sale.

2.17 Forbearance will remain exempt from the advice requirements. We believe it is clear what

constitutes forbearance and firms should refer to MCOB13

15

and the guidance on

mortgage forbearance

16

for further clarity.

2.18 To help demonstrate our approach, the following table outlines when firms are required to

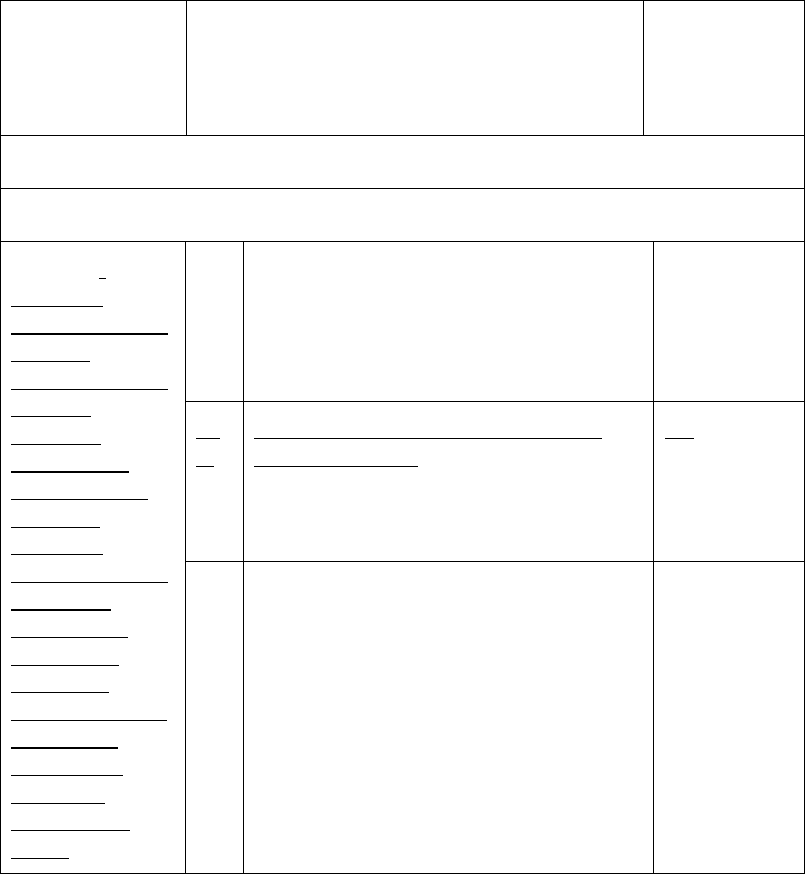

provide advice and when execution-only is permitted for typical contract variations.

17

Table 2 – The application of advice and execution-only to contract variations

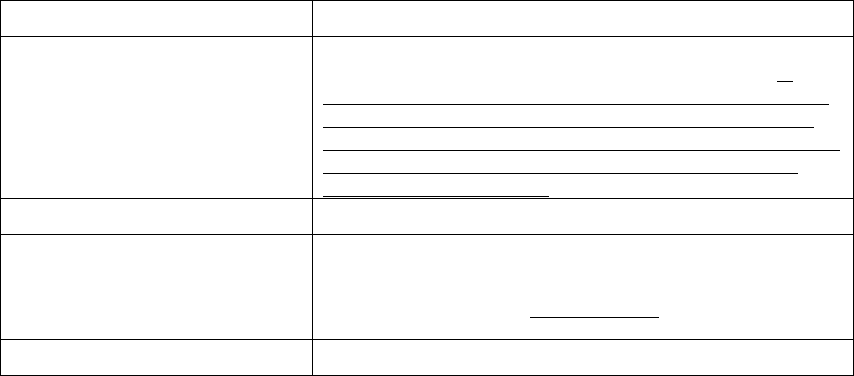

Contract variations Advice or

execution-only

Rate switches

This includes product switches and retention deals. Retention deals are usually lender driven,

once the borrower comes to the end of their current product. Product switches are usually

borrower driven when they will request a new product from their lender. Both have the same

effect and are classed as rate switches under the final rules.

No increase in the current balance outstanding and the firm presents all the

products for which the borrower is eligible via a non-interactive channel (e.g.

in writing). The borrower selects their product via a non-interactive channel.

Execution-only

No increase in the current balance outstanding and the firm presents all the

products for which the borrower is eligible via a non-interactive channel, but

accepts the borrower’s choice of product via an interactive channel.

Execution-only

No increase in the current balance outstanding, but the firm steers the

borrower to a particular product or products (interactive or non-interactive).

Advice

The borrower wants to borrow more and is offered a new product. Advice

15 http://fsahandbook.info/FSA/html/handbook/MCOB/13

16 FG11/15: Forbearance and Impairment Provisions –‘Mortgages’, (October 2011):

www.fsa.gov.uk/library/policy/final_guides/2011/fg11_15.shtml

17

This table is for illustration purposes and is not an exhaustive list.

PS12/16

Mortgage Market Review: Feedback on CP11/31 and final rules

Financial Services Authority 15October 2012

Variations to existing contracts, or new replacement contracts intended to have the same effect,

via an interactive channel.*

*Variations carried out on a non-interactive basis, can be offered on an execution-only basis, including

where there is additional borrowing.

Further advances

This involves an increase in the current amount outstanding. Advice

Addition or removal of a party to the contract

Involving no increase in the current amount outstanding. Execution-only

Involving an increase in the current amount outstanding. Advice

Change in monthly payment – (including extending term or changing the payment method)

Involving no increase in the current amount outstanding. Execution-only

Involving an increase in the current amount outstanding. Advice

Porting – This involves taking the existing mortgage to a new property

Involving no increase in the current amount outstanding. Execution-only

Involving an increase in the current amount outstanding. Advice

Consent to let – Allowing the borrower to let their property, which was previously owner-occupied

Involving no increase in the current amount outstanding. Execution-only

Involving an increase in the current amount outstanding. Advice

2.19 We are also clarifying how the responsible lending rules will apply to contract variations.

This is discussed in detail in Chapter 3.

PS12/16

Mortgage Market Review: Feedback on CP11/31 and final rules

Annex X

16 Financial Services Authority October 2012

3

Transitional arrangements

Introduction

3.1 In this chapter we consider the transitional arrangements and the related issue of contract

variations. A summary of the feedback to all questions asked about the transitional

arrangements is set out under Q15 to Q19 in Annex 1.

3.2 This is an area where we have revised our approach in light of the feedback to CP11/31

18

and our subsequent discussions with respondents.

Transitional arrangements and contract variations

3.3 In CP11/31 we proposed some transitional arrangements designed to mitigate the impact of

the new responsible lending rules on existing borrowers who:

• cannot demonstrate affordability for their new mortgage as required by the new

affordability requirements; or

• do not have an acceptable repayment strategy, according to the new

interest-only requirements.

3.4 We proposed several conditions that would have to be met for the borrower to qualify for

the transitionals.

19

3.5 The vast majority of respondents agreed that we should take steps to mitigate the impact of

our responsible lending proposals on borrowers. However, most respondents felt that, as

drafted, the proposals were too restrictive to help many borrowers and too complex to be

widely adopted by lenders.

18 CP11/31, Mortgage Market Review: Proposed package of reforms, (December 2011): www.fsa.gov.uk/static/pubs/cp/cp11_31.pdf

19

See the eligibility criteria set out at paragraph 3.358 in CP11/31.

PS12/16

Mortgage Market Review: Feedback on CP11/31 and final rules

Financial Services Authority 17October 2012

3.6 We agree that it would benefit borrowers to have more flexibility than was permitted in the

original proposals. For example, we can see that borrowers may benefit from taking on

higher payments to fix their rate in periods where interest rates are expected to rise.

Similarly, we can see that they may benefit from some material variations to a mortgage,

such as a change in term.

3.7 We have amended the rules. The final rules:

• simplify when an affordability assessment is required for all existing borrowers when

they make changes to their existing mortgage – either as a contract variation, or as a

new replacement contract;

• only require an affordability check where there is additional borrowing, or a material

impact on affordability; and

• simplify the transitional arrangements, to make them more flexible and more practical.

In particular, we are allowing lenders to make their own assessment about making

exceptions to the affordability and interest-only rules.

Existing borrowers – contract variations and new regulated

mortgage contracts

3.8 Under both our existing rules and the MMR proposals, an affordability assessment is

required whenever a lender enters into a regulated mortgage contract with a customer,

whether or not there is an impact on affordability. For example, an affordability assessment

is required when a customer moves to a new rate with their existing lender, if the

transaction is structured as a new mortgage contract, even where they are not borrowing

any more money. By contrast, an affordability assessment is not required for the same

transaction if it takes effect through a contract variation, even where there might be a

material impact on affordability.

3.9 To address this, we have amended the rules so that an affordability assessment is not

required for an existing borrower, staying with their existing lender, if there is no increase

in the current amount outstanding (i.e. no additional borrowing) – unless there is a material

impact on affordability. This is the case whether the transaction takes effect through a

contract variation, or a new regulated mortgage contract.

3.10 So, for example, an affordability assessment will not be required for a change that does not

have a material impact on affordability, such as a rate switch or retention deal; or where

the borrower is porting their mortgage or moving to a new property (with no increase in

the current amount outstanding).

3.11 However, an affordability assessment will be required where there is additional borrowing, or

there is deemed to be a material impact on affordability. Whether a change has a material

PS12/16

Mortgage Market Review: Feedback on CP11/31 and final rules

Annex X

18 Financial Services Authority October 2012

impact on affordability will vary according to the circumstances of the case. We will assume,

in the absence of evidence to the contrary, that the following changes are likely to be material:

• extending the term of the loan beyond the borrower’s expected retirement;

• changing the repayment type; or

• removing a party to the contract.

3.12 This approach is consistent with our approach to advice and contract variations, as

discussed in Chapter 2.

3.13 These changes to the rules will mean that the transitional arrangements are required in

many fewer situations.

The revised approach to transitional arrangements

3.14 Despite this change, there will be situations where the responsible lending rules continue to

bite for existing borrowers. This includes where:

• there are material changes to affordability (such as those set out in paragraph 3.11 above);

• the borrower does not have an acceptable repayment strategy for an interest-only

mortgage; or

• the borrower wishes to move their mortgage to another lender.

3.15 We recognise that in such scenarios, while an affordability assessment should apply because

there may be a material impact on affordability, there may be some situations where, due to

extenuating circumstances, such a change may be in the interests of the borrower and lead

to a better outcome than remaining in their current situation. We also recognise that it is

not possible for us to predict every such circumstance in the rules.

3.16 Therefore, our revised approach allows lenders flexibility to make their own decisions

about making exceptions to the affordability and interest-only rules for existing borrowers.

This will apply whether or not it materially affects affordability, as long as:

• there is no increase in the current amount outstanding (i.e. no additional borrowing),

except product or arrangement fees, which may be added to the mortgage balance

(firms are reminded of the new provisions that will apply when adding fees or

charges to a loan

20

(MCOB 4.6A); and also our existing rules on excessive charges

(MCOB 12.5)); and

• the lender has judged that the proposed transaction is in the customer’s best interests.

20 See paragraphs 5.121 to 5.130 in CP11/31.

PS12/16

Mortgage Market Review: Feedback on CP11/31 and final rules

Financial Services Authority 19October 2012

3.17 These transitional arrangements will be able to be used by lenders to take on borrowers

from other lenders.

3.18 We have considered whether additional borrowing should be allowed under the transitional

arrangements. A few respondents to CP11/31 supported this. However, we cannot see a

way to control the gaming issues that would arise, or the opportunity for borrowers to take

on mortgage commitments which they cannot afford, which would defeat the objective of

our responsible lending rules. We are not, therefore, allowing additional borrowing.

3.19 There is one exception to this. Where the additional funds are being advanced by the

existing lender for essential repairs or maintenance work to the property, we are allowing

this, subject to certain criteria, including that:

• the value of the property is at risk if the repairs or maintenance work are not carried out;

• the additional borrowing is to be used for the repairs or maintenance work; and

• the firm has credible evidence of the cost of the repairs or maintenance work.

3.20 The aim of the transitional arrangements is to help existing borrowers who are being

prevented from borrowing because of the stricter MMR requirements. We are therefore

retaining an eligibility condition, which states that the transitional arrangements will not

apply where a borrower has, since the implementation of the MMR, taken on additional

borrowing and increased the size of their mortgage (other than to finance any relevant

product or arrangement fee, or essential repairs or maintenance work). This is to prevent

the transitional arrangements being used where the inability to meet lending criteria is a

result of changed circumstances or real underlying affordability issues and not the MMR.

3.21 The transitional arrangements apply to existing borrowers who have a mortgage in place

when the MMR rules come into force. We have amended the transitional arrangements to

make it clear that they also apply to borrowers with mortgages that were entered into

before the introduction of mortgage regulation in 2004 (MCOB11.7.1R(1)(a)).

3.22 We already indicated in CP11/31 that we will expect lenders to have robust systems and

controls around the use of the transitional arrangements. As a result of our amended

approach, we also expect firms to include:

• an exceptions policy, which should form part of the lender’s wider responsible

lending policy;

• record keeping, including a record of the rationale behind each lending decision made

under the transitional arrangements; and

• producing clear management information to monitor the application of these exceptions.

3.23 Table 3 illustrates the circumstances where an affordability assessment is required for a

post-sale contract variation, and where the transitional arrangements apply.

PS12/16

Mortgage Market Review: Feedback on CP11/31 and final rules

Annex X

20 Financial Services Authority October 2012

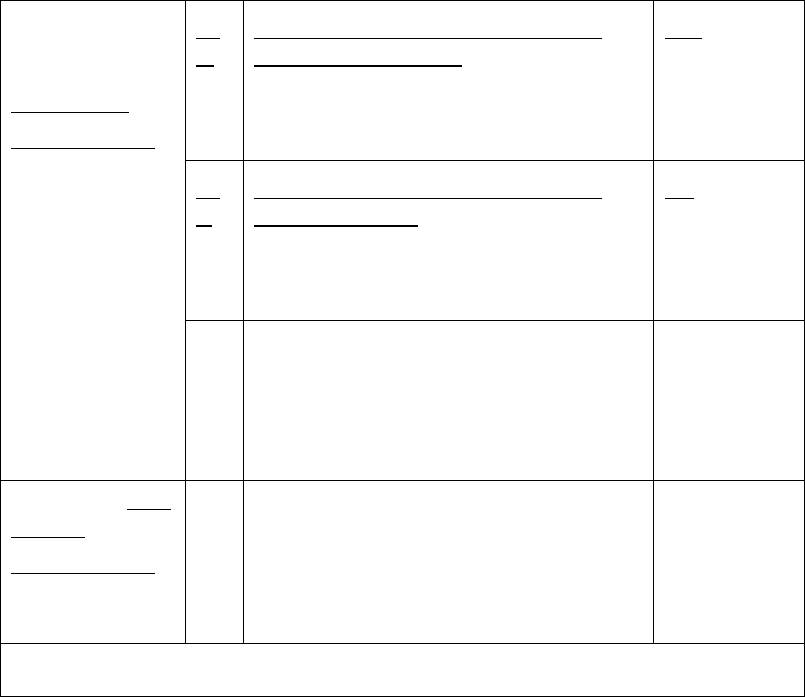

Table 3 – Existing borrowers – affordability assessments and

transitional arrangements

Post-sale variations Responsible lending requirements

When is an affordability assessment required (for a variation to an existing contract, or a new

replacement contract intended to have the same effect with the existing lender)?

Full requirements are set out in MCOB 11.6

Rate switches

This includes product switches and retention deals. Retention deals are usually lender driven, once the

borrower comes to the end of their current product. Product switches are usually borrower driven, when they

will request a new product from their lender. Both have the same effect and are classed as rate switches under

the final rules.

Involving no increase in the current amount

outstanding.

No affordability assessment is required (even if the rate

switch results in higher payments).

Involving an increase in the current amount

outstanding.

An affordability assessment will be required.

Further advances

Involving an increase in the current amount

outstanding.

An affordability assessment will be required.

Addition or removal of a party to the contract

Involving no increase in the current amount

outstanding.

This is likely to be a material change, and if so an

affordability assessment will be required.

Involving an increase in the current amount

outstanding.

An affordability assessment will be required.

Changes that have a material impact on affordability (e.g. extending term beyond expected retirement,

or changing the payment method)

Involving no increase in the current amount

outstanding.

An affordability assessment will be required.

Involving an increase in the current amount

outstanding.

An affordability assessment will be required.

Porting – This involves taking the existing mortgage to a new property

Involving no increase in the current amount

outstanding.

No affordability assessment is required.

Involving an increase in the current amount

outstanding.

An affordability assessment will be required.

Forbearance

An affordability assessment is not required for

a variation made solely for the purposes of

forbearance (as per MCOB 11.6.3R(3)).

Not applicable.

PS12/16

Mortgage Market Review: Feedback on CP11/31 and final rules

Financial Services Authority 21October 2012

Transitional arrangements Responsible lending requirements

When can the transitional arrangements be applied (for a variation to an existing contract, a new

replacement contract intended to have the same effect, or a new contract with the same or a

different lender)?

Full requirements are set out in MCOB 11.7.

Involving no increase in the current amount

outstanding (whether or not there is a material

impact on affordability).

The transitional arrangements may be applied.

Involving an increase in the current amount

outstanding (except for essential repairs or

maintenance work).

An affordability assessment will be required, so the

transitional arrangements cannot be applied.

PS12/16

Mortgage Market Review: Feedback on CP11/31 and final rules

Annex X

22 Financial Services Authority October 2012

4

High net worth and

business lending

Lending to high net worth customers

4.1 In CP10/16

21

, we indicated that this could be a market where our approach to affordability

may need to vary. Almost all respondents thought that high net worth (HNW) customers

would benefit from an alternative approach because of the complex nature of their incomes

and the potentially short loan terms (typically five years).

4.2 In CP11/31

22

, we therefore proposed some tailoring for HNW customers, including:

• permitting HNW customers to opt-out of advice;

• making provision for interest roll-up mortgages; and

• a tailored approach to disclosure.

4.3 We have also been considering whether a more fundamental change in our approach to

HNW customers would be appropriate, including considering whether our regime should

apply at all to those customers with higher levels of income or wealth, on the basis that it is

perfectly reasonable for these customers to take greater risks and that regulation is not

needed to protect them from the decisions they make. While they still ultimately face the

loss of their home, they are more likely to have access to a range of professional advisers,

and will have more options available to them in the event that they experience financial

difficulties – for example, by downsizing rather than becoming homeless. So we asked an

open question in CP11/31 about whether it would be appropriate to allow some form of

carve-out from mortgage regulation.

4.4 We suggested that there might be two ways to do this – either by completely disapplying

the mortgage rules or by allowing HNW customers to elect whether to forgo the protection

of the rules.

21 CP10/16, Mortgage Market Review: Responsible Lending, (July 2010): www.fsa.gov.uk/pubs/cp/cp10_16.pdf

22 CP11/31, Mortgage Market Review: Proposed package of reforms, (December 2011): www.fsa.gov.uk/static/pubs/cp/cp11_31.pdf

PS12/16

Mortgage Market Review: Feedback on CP11/31 and final rules

Financial Services Authority 23October 2012

Feedback to CP11/31

4.5 As we explain in more detail in Annex 1, most respondents to the consultation recognised

that HNW customers merit a different regulatory approach to that proposed for the

mainstream mortgage market. There was some limited support for an approach that would

allow HNW customers to opt-out of mortgage regulation, although firms operating in this

sector felt that this approach would be difficult to operate in practice.

4.6 However, many respondents felt that wealth does not necessarily equate to financial

capability, and did not agree that customers with a greater degree of wealth would

necessarily make sound financial decisions. They were therefore cautious about completely

disapplying the protection of the mortgage rules.

4.7 However, many respondents involved in lending to HNW customers felt that the MMR

proposals (and some aspects of existing MCOBrequirements) did not fit well with the

bespoke service offered to many HNW customers, and therefore would need to be

amended. For example:

• firms would not generally consider it necessary or appropriate to drill down into the

details of basic expenditure, such as utility bills and council tax, for very wealthy

customers; and

• wealthy customers tend to be very asset-rich, and mortgage payments may be serviced

through these assets (including through their sale).

Our approach to high net worth mortgage customers

4.8 We recognise that applying all the MMR proposals, particularly the full affordability

checks, is not proportionate for very wealthy customers and that a different regulatory

approach is appropriate. However, there has not been strong support for carving HNW

customers out of mortgage regulation completely.

4.9 The approach we are taking, therefore, aims to recognise the characteristics of lending to

HNW customers, by applying higher-level requirements than for mainstream mortgages.

This will be based on the following key elements:

• Disclosure – A tailored approach will apply, as proposed in CP11/31.

• Advice – Interactive sales may be conducted on an execution-only basis.

• Responsible lending – Requirements will be set at a higher level than for

mainstream mortgages.

PS12/16

Mortgage Market Review: Feedback on CP11/31 and final rules

Annex X

24 Financial Services Authority October 2012

The definition of a high net worth mortgage customer

4.10 To appropriately apply any of these elements, we first need to define who we consider to be

a ‘high net worth’ customer.

4.11 In CP11/31, we proposed to define a HNW customer as having a minimum net annual

income of £1m or minimum net assets of £3m.

4.12 As we explain in Annex 1, respondents broadly agreed with the proposed definition for net

assets, but did not agree with the proposed definition of net annual income, as they thought

£1m was much too high.

4.13 In response to feedback (as discussed in Annex 1, Q81) in we have amended the income

part of the definition to a net income of £300,000. Therefore, we are defining a HNW

mortgage customer as a customer with a minimum annual net income of £300,000, or

minimum net assets of £3m.

4.14 This definition applies to the customer applying for the mortgage but it is also met where

the obligations of that customer are guaranteed by a person who satisfies the income or

assets criteria.

4.15 We are not being prescriptive about what assets can be taken into consideration in making

up the minimum net asset figure of £3m. It is up to the lender to decide this. Therefore it

would be possible for the mortgaged property to be included in the total (net of any

outstanding mortgage).

4.16 Where there is more than one applicant, at least one of the applicants must meet the

definition in their own right (as per MCOB1.2.3BR). This means that the income or assets

of two or more applicants cannot be added together to meet the definition and thereby

circumvent the responsible lending rules that would otherwise apply.

4.17 Where assets are held jointly (such as may happen in the case of property), a lender should

consider the value of the customer’s actual share of assets.

23

4.18 We are aware that we have recently published a Consultation Paper

24

on restrictions on the

retail distribution of unregulated collective investment schemes and close substitutes. In this

paper, we refer to secondary legislation that allows financial promotions to be exempt from

Financial Services and Markets Act 2000 (FSMA) marketing restrictions if certain

conditions are met.

25

Exemptions are available in the legislation for customers who are

certified as ‘high net worth individuals’.

26

Among the criteria for customers to be

23 In the case of a property held by ‘joint tenants’ both owners are deemed to own 100% of the value of the property. Therefore, the full

value of the asset could be considered for the purposes of an individual meeting the definition of a HNW mortgage customer. If the

property is held by tenants in common, the actual proportion of the individual’s share of the property could be considered.

24 CP12/19, Restrictions on the retail distribution on unregulated collective investment schemes and close substitutes, (August 2012):

www.fsa.gov.uk/static/pubs/cp/cp12-19.pdf

25

The Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (FPO) and the Financial Services and Markets Act

2000 Promotion of Collective Investment Schemes) (Exemptions) Order 2001(PCIS Order). The exemptions in these Orders are

determined by HM Treasury.

26

See article 48 of the FPO and article 21 of the PCIS Order.

PS12/16

Mortgage Market Review: Feedback on CP11/31 and final rules

Financial Services Authority 25October 2012

categorised as high net worth under the orders are having an annual income of more than

£100,000 or having investable net assets of more than £250,000.

4.19 We are choosing to apply a different definition of HNW in the mortgage market. HNW

customers face the same risks when they take out a loan secured against their homes as any

other customer. This includes the risk that they may ultimately lose their home. When setting

the scope of mortgage regulation in 2004, the then government was not persuaded that a

specific exemption for HNW customers was required and felt that they should be afforded

the same protections as any other customer. Our current mortgage rules reflect this and apply

to all regulated mortgage contracts, including those taken out by HNW customers.

4.20 Our changed approach, in the light of the market feedback, recognises that there is a very

small subset of genuinely wealthy customers, whose wealth is significantly above average.

This level of wealth gives these customers specific advantages, in particular, a considerably

reduced risk of becoming homeless in the event that they experience financial difficulties.

The HNW definition for mortgages will therefore exclude most customers, and will ensure

that the tailoring is targeted at the most wealthy.

27

4.21 To make the distinction clearer between the HNW definition that applies in relation to

the mortgage rules and the HNW definitions used elsewhere in the FSA’s Handbook, we

have amended the defined term from ‘high net worth customer’ to ‘high net worth

mortgage customer’.

4.22 In CP11/31 we proposed that, before a firm could treat a customer as being HNW, they

should obtain a written statement from a suitably qualified professional adviser to confirm

that the customer meets the definition of a HNW mortgage customer. In response to

feedback, we have amended this requirement (see MCOB1.2.9CR(1)), to allow firms also

to use evidence that they have obtained through their business relationship with the

customer, for example, if they manage their assets.

The application of the new approach

4.23 The tailoring that we proposed for lending to HNW mortgage customers for disclosure

(MCOB4.9, 5.7, 6.7, 7.7 and 13.7) and charges (MCOB12.6) is proceeding on the basis

consulted on in CP11/31. Firms may decide to either comply with MCOBin full, or to use

the tailored approach, but not to mix and match, on the basis that it would be very

confusing for a borrower.

4.24 We are applying a different approach for the new advice and responsible lending provisions

for HNW mortgage customers. A firm may decide when to use these provisions

independently of whether they adopt the tailored provisions for disclosure and charges. This

is because we cannot see how a firm’s approach to disclosure (which might be purely driven

by systems or process considerations) should determine whether a lender can apply the new

27 We estimate that borrowers with a net income of £300,000 accounted for around 0.2% of mortgage sales in 2011. See Exhibit 22.6

in MMR Data Pack (October 2012).

PS12/16

Mortgage Market Review: Feedback on CP11/31 and final rules

Annex X

26 Financial Services Authority October 2012

provisions for advice or responsible lending. Therefore a firm may choose different

approaches to the disclosure and charges tailoring, and the advice and responsible lending

provisions for HNW mortgage customers.

Advice

4.25 As proposed in CP11/31, we are allowing a HNW mortgage customer to get a mortgage on

an execution-only basis, even where the sale is interactive – provided the customer has

confirmed in writing that they are aware of the consequences of losing the protections of the

rules on suitability, and have made a positive election to proceed with an execution-only sale.

4.26 Many HNW mortgages are not commoditised in the same way as residential mortgages, so the

structure of the deal and the interest rate may vary according to the individual circumstances

of the customer. Therefore, it will not always be possible for a HNW mortgage customer to

provide the product details that we would normally require for an execution-only sale, such as

the rate of interest and the interest rate type. We have amended the rules for HNW mortgage

customers so that they do not have to provide this information to purchase a product on an

execution-only basis.

4.27 Unlike customers in the mainstream mortgage market, HNW mortgage customers are not

required to get advice in the unlikely event that they fall into one of the vulnerable

categories (i.e. debt consolidation, right-to-buy, equity release or sale and rent back). This is

because of the greater resources available to HNW mortgage customers and the likelihood

that they will have access to the services of other professional advisers.

Responsible lending

4.28 The lender is required to assess whether the customer will be able to pay the sums due (to

cover the sums advanced and the interest) and demonstrate that it is affordable for the

customer, as required by the main overarching responsible lending rule (MCOB11.6.2R).

However, the rules beneath this do not drill down into the same level of granular detail as

for mainstream mortgages, giving the lender some flexibility to meet the requirements in a

way that is appropriate for the customer.

4.29 When making their assessment of affordability for HNW mortgage customers, the lender

may base their assessment on both the income and the assets of the borrower. They must

also consider the expenditure of the borrower, by considering whether they will have

sufficient resources to cover their credit commitments, basic essential expenditure and basic

quality of living costs.

28

However, we are not prescriptive about how they do this, and

expenditure can be considered in general terms (i.e. it may be possible for a lender to

develop a general approach applied across customers or particular groups of customers).

28 We are retaining the use of the terms ‘basic essential expenditure’ and ‘basic quality of living costs’ for business lending and lending

to HNW mortgage customers. While developed for use in our rules for mainstream mortgages, we believe their use in business and

HNW lending will be helpful for firms in understanding the types of expenditure that we expect them to consider.

PS12/16

Mortgage Market Review: Feedback on CP11/31 and final rules

Financial Services Authority 27October 2012

4.30 In addition, the lender will be required to:

• obtain evidence of the income and/or assets that they are basing their affordability

assessment on;

• take account of the impact of likely future interest rates on affordability; and

• take account of known or likely future changes to the income and expenditure of

the customer.

4.31 The interest-only rules continue to apply in their entirety, because we believe that the

interest-only rules are flexible enough to be adapted to the needs of different types of

customers, including HNW mortgage customers.

4.32 The requirement to have a responsible lending policy, and record keeping and monitoring

apply in full, subject to some minor amendments to reflect the revised approach to

responsible lending.

4.33 As we discuss further at Q70, Annex 1, a specific exception has been made for secured

overdrafts for HNW mortgage customers from the rules around extending the terms of a

bridging loan (MCOB11.6.55R).

Disclosure

4.34 We have made some small adjustments to the disclosure rules in light of the amended

approach to execution-only sales for HNW mortgage customers (see MCOB5.4.18BR).

These set out when a firm must provide a KFI, and when a customer has to be told they

can request one.

Business lending

4.35 In CP11/31, we proposed to read across the majority of the MMR proposals to business

lending (i.e. regulated mortgage contracts made for a business purpose), but proposed a

limited amount of tailoring, including rules in relation to interest roll-up mortgages and

professional standards.

4.36 We also asked a wider question about whether it might be appropriate to carve out

business loans from our proposed new regime entirely. There is an argument that if a

business borrower and lender want to take an informed risk, and the business borrower is

happy to use their home as collateral for a business venture, then why should that

individual be prevented from doing so? However, we must also consider those who are less

able to protect their own interests and who arguably do need regulatory protection – such

as a sole trader borrowing against their home as a last resort to keep their business afloat.

PS12/16

Mortgage Market Review: Feedback on CP11/31 and final rules

Annex X

28 Financial Services Authority October 2012

4.37 So a key question for us was how would we draw a line between those small business

borrowers who can take a risk, and should be allowed to do so, and those who cannot?

Also, how would we prevent any potential carve-out from being exploited as a means of

avoiding our new affordability requirements?

4.38 We asked for feedback on these questions and also had a number of discussions with

lenders active in regulated business lending to help inform our policy approach.

Feedback to CP11/31

4.39 As we set out at Q89 in Annex 1, respondents’ views on a carve-out were polarised.

Lenders and trade bodies strongly supported some form of carve-out. But consumer

representatives were very concerned about the risks this would pose.

4.40 Consumer representatives were not convinced that potential business borrowers would

always take an informed business risk, particularly where the boundary between their

personal and business finances is blurred, as it might be when lending is secured on

personal assets to raise business capital.

4.41 In addition, they had strong concerns about the risk of gaming, as customers might claim

that they are borrowing for a business purpose to avoid the strengthened regime put in

place through the MMR.

4.42 In contrast, representatives from the industry thought that business borrowers are better

able to make financial decisions. They felt that the MMR proposals would not be easily

transferable to business lending, as they do not reflect the way that business banking works

in practice, i.e. where the focus of underwriting is the circumstances of the business, and

the ability of the business to repay the loan. They also felt that application of the full set of

MMR proposals to business lending would be disproportionately onerous, given the very

small proportion of business lending that is regulated, and would not add any significant

benefit to these customers.

Our approach to business lending

4.43 We recognise that the full package of MMR proposals is not workable for business lending

and that, to a large extent, business borrowers have higher levels of financial capability

than consumers in general.

4.44 However, we have not been convinced that business lending should be entirely carved out

of mortgage regulation.

4.45 Our view is that some business borrowers, particularly some of the smaller business

borrowers who are captured by mortgage regulation, do need consumer protection when

putting their homes at risk, and we cannot see how gaming would be prevented if business

lending was completely carved-out of mortgage regulation. While we accept that much of

current business lending practice is prudent in today’s constrained market, we see a clear

PS12/16

Mortgage Market Review: Feedback on CP11/31 and final rules

Financial Services Authority 29October 2012

risk of gaming developing if we were to disapply our regime completely. Particularly

outside the traditional business banking environment, where lenders may see opportunities

to increase market share through bypassing our affordability assessments.

4.46 We have therefore not carved business lending out of our mortgage regime. However, we

have applied an alternative approach, which recognises the characteristics of business

lending where this differs from mainstream residential mortgages. This approach will be

based on the following key elements:

• Disclosure – The existing rules are tailored for business loans and that tailoring

will continue.

• Advice – Interactive sales may be conducted on an execution-only basis.

• Responsible lending – Requirements are set at a higher level than for mainstream

mortgages, and recognise that a mortgage may be repaid from the resources of a business.

The application of the new approach

4.47 Reflecting the fact that business borrowing is likely to be individually negotiated and so sits

poorly with the standard approach to disclosure, our existing rules are specially tailored

where the regulated mortgage contract is for a business purpose. This relates mainly to

disclosure requirements (as set out in MCOB4.9, 5.7, 6.7, 7.7 and 13.7) and to charges

(MCOB12.6). We are not changing these requirements, or the situations where they can be

used. We currently require a firm to either comply with MCOBin full, or use the tailored

approach in its entirety for any particular regulated business loan. This means that a firm

cannot mix and match whether they use the tailored provisions or full MCOBrequirements

as this would be very confusing for a borrower. This approach continues for these existing

tailored provisions.

4.48 We are, however, applying a different approach for the new advice and responsible lending

provisions. These provisions apply only where the loan is solely for a business purpose.

Examples where this might apply include:

• raising a loan solely for a business purpose on a customer’s previously

unencumbered home;

• taking a further advance that is solely for a business purpose (even though the main

mortgage may have been taken out for the purchase of the home, or other personal use,

such as home improvements or debt consolidation); and

• remortgaging to raise additional funds, as long as the additional funds are being raised

solely for a business purpose (even though the existing outstanding mortgage balance

may have been taken for purchase of the home or other personal use).

PS12/16

Mortgage Market Review: Feedback on CP11/31 and final rules

Annex X

30 Financial Services Authority October 2012

4.49 The new provisions will not include the following scenarios, where there is an element of

personal use to the loan, and where the full MCOBrequirements for advice and responsible

lending will therefore apply:

• remortgaging for several purposes, e.g. debt consolidation and a business purpose; or

• taking a further advance for several purposes, e.g. home improvements and a

business purpose.

4.50 As with our existing tailored approach, we do not capture buy-to-let finance under the

business lending rules. We do not regulate mortgages secured on buy-to-let properties. In cases

where a regulated mortgage contract is secured on the borrower’s home to finance the

purchase of a single buy-to-let property, there is already existing guidance (MCOB1.2.5G(2)),

which states our opinion that this would not be for a business purpose and therefore falls

under the main affordability rules.

4.51 The use of these provisions is not dependent on whether the firm is using the existing

tailored approach for business loan disclosure. This is because we cannot see how a firm’s

approach to disclosure (which might be purely driven by systems or process considerations)

should determine whether a lender can apply the new provisions for advice or responsible

lending. Therefore, a firm may decide to apply the advice and responsible business lending

provisions whether or not they apply the tailored disclosure provisions. We include

guidance on this in the rules (see MCOB1.2.4BG).

4.52 It will still be up to a firm to determine whether a loan is for a business purpose (as set out

in MCOB1.2.5G(2)). To prevent gaming of the new provisions for advice and responsible

lending, we require a firm to have sight of a credible business plan before determining

whether the loan is solely for a business purpose (MCOB1.2.9DR). The aim of this

requirement is for the firm to assess whether there is a legitimate business proposition that

has not been fabricated for the reason of obtaining mortgage finance for other (i.e. personal)

reasons – rather than for underwriting purposes (although we recognise that in practice the

same business plan may also be used by the lender when assessing affordability).

Advice

4.53 We have amended the rules to allow loans solely for a business purpose to be obtained on

an execution-only basis, even in interactive sales, as for HNW mortgage customers and

mortgage professionals. The customer must confirm in writing that they are aware of the

consequences of losing the protections of the rules on suitability, and make a positive

election to proceed with an execution-only sale.

4.54 Many business loans are not commoditised in the same way as residential mortgages, so the

structure of the deal and the interest rate may vary according to the circumstances of the

individual transaction. So it will not always be possible for a business borrower to specify

the product details that we would normally require for an execution-only sale, such as the

rate of interest and the interest rate type. Therefore, where the loan is solely for a business

PS12/16

Mortgage Market Review: Feedback on CP11/31 and final rules

Financial Services Authority 31October 2012

purpose, we are not requiring this information to be given before proceeding with an

execution-only sale.

4.55 Unlike HNW mortgage customers, business borrowers are required to get advice if for

some reason they also fall into one of the vulnerable categories (i.e. debt consolidation,

right-to-buy, equity release or sale and rent back). This situation is relatively unlikely to

occur (given that the purpose of the loan must be solely for a business purpose), but if it

does, our view is that the borrower should receive advice, given that the loan will be

secured against their home.

Responsible lending

4.56 We have applied a different approach to assessing affordability for loans solely for a

business purpose. The main, over-arching responsible lending rule (MCOB11.6.2R) will

still apply, requiring the lender to assess whether the customer will be able to pay the sums

due, and to demonstrate that the mortgage is affordable for the customer. However, the

affordability rules beneath this will not drill down into the same granular detail as for

mainstream mortgages, giving the lender appropriate flexibility in their underwriting of

business loans.

4.57 When a mortgage is being raised for a business purpose, we recognise that the loan may

be repaid from:

• the resources of a business; or

• the personal resources of a borrower (e.g. if funds are being raised for a new

business venture).

4.58 We are accommodating both of these situations in the rules.

4.59 Where the loan is being repaid through the resources of a business, we require the lender

to assess whether that business will be able to repay the mortgage. We are not being

prescriptive about how the lender should do this, and the rule just requires the lender to

base this assessment on the strength of the resources of the business (MCOB11.6.26R(2)

(b)). This may include consideration of factors such as cash flow, assets and liabilities.

4.60 If the borrower is reliant on the business for their personal income, then we require the

lender, as a minimum, to consider in general terms whether a business can support the

borrower’s basic essential and basic quality of living costs.

29

We are not being prescriptive

about how the lender does this, and we are being clear in the rules that this can be done in

general terms. Therefore, it may be possible for a lender to develop a general approach

applied across borrowers, or across particular groups of borrowers. Alternatively, they

might consider how much the borrower draws from the business for their personal use.

29 We are retaining the use of the terms ‘basic essential expenditure’ and ‘basic quality of living costs’ for business lending and lending

to HNW mortgage customers. While developed for use in our rules for mainstream mortgages, we believe their use in business and

HNW lending will be helpful for firms in understanding the types of expenditure that we expect them to consider.

PS12/16

Mortgage Market Review: Feedback on CP11/31 and final rules

Annex X

32 Financial Services Authority October 2012

4.61 Where the loan is being repaid through the personal resources of the borrower, the lender

must make their assessment of affordability through an assessment of the income, assets

and committed expenditure of the borrower, and a general consideration of their basic

essential expenditure and basic quality of living costs. Once again, we are not being

prescriptive about how the lender should do this.

4.62 In addition, whether the mortgage will be repaid by business or personal resources, the

lender is also required to:

• obtain evidence of the income or assets of the borrower, or the resources of the business;

• take account of the impact of likely future interest rates on affordability; and

• take account of known or likely future changes to the financial position of the business.

4.63 The interest-only rules continue to apply in their entirety, because we believe that they are

flexible enough to be adapted to the needs of different types of customers, including those

borrowing for business.

4.64 The requirement to have a responsible lending policy, and record keeping and monitoring,

still apply in full, subject to some minor amendments to reflect the revised approach to

responsible lending.

4.65 As we discuss further at Q70 in Annex 1, we have made a specific exception for secured

overdrafts that are solely for a business purpose from the rules around extending the terms

of a bridging loan (see MCOB11.6.55R).

Disclosure

4.66 We have made some small adjustments to the disclosure rules in light of the amended

approach to execution-only sales for business lending (see MCOB5.4.18BR(2)). These

set out when a firm must provide a KFI, and when a customer has to be told they can

request one.

PS12/16

Mortgage Market Review: Feedback on CP11/31 and final rules

Financial Services Authority A1:1October 2012

Annex 1

Detailed feedback

on CP11/31

Introduction

1. In this Annex we summarise the feedback received to our proposals in CP11/31

1

and set

out our policy response. Feedback to some of our distribution proposals is discussed in

detail in Chapter 2. Feedback to our proposed transitional arrangements is in Chapter 3.

Feedback to our proposed approach to high net worth and business lending is in Chapter 4.

Responsible lending and borrowing

Q1: Do you agree that lenders should detail how they incorporate

anti-fraud controls into their affordability assessments in their

responsible lending policy?

2. The majority of respondents agreed in theory that anti-fraud controls should be

incorporated into firms’ responsible lending policies.