This document, concerning Consumer Clothes Dryers is an action issued by the

Department of Energy. Though it is not intended or expected, should any discrepancy

occur between the document posted here and the document published in the Federal

Register, the Federal Register publication controls. This document is being made

available through the Internet solely as a means to facilitate the public's access to this

document.

1

[6450-01-P]

DEPARTMENT OF ENERGY

10 CFR Part 430

[EERE-2014-BT-STD-0058]

RIN 1904-AF59

Energy Conservation Program: Energy Conservation Standards for Consumer

Clothes Dryers

AGENCY: Office of Energy Efficiency and Renewable Energy, Department of Energy.

ACTION: Direct final rule.

SUMMARY: The Energy Policy and Conservation Act, as amended (“EPCA”),

prescribes energy conservation standards for various consumer products and certain

commercial and industrial equipment, including consumer clothes dryers. In this direct

final rule, DOE is adopting amended energy conservation standards for consumer clothes

dryers. DOE has determined that the amended energy conservation standards for these

products would result in significant conservation of energy and are technologically

feasible and economically justified.

DATES: The effective date of this rule is [INSERT DATE 120 DAYS AFTER DATE

OF PUBLICATION IN THE FEDERAL REGISTER]. If adverse comments are

received by [INSERT DATE 110 DAYS AFTER DATE OF PUBLICATION IN

2

THE FEDERAL REGISTER] and DOE determines that such comments may provide a

reasonable basis for withdrawal of the direct final rule under 42 U.S.C. 6295(o), a timely

withdrawal of this rule will be published in the Federal Register. If no such adverse

comments are received, compliance with the amended standards established for consumer

clothes dryers in this direct final rule is required on and after March 1, 2028. Comments

regarding the likely competitive impact of the standards contained in this direct final rule

should be sent to the Department of Justice contact listed in the ADDRESSES section on

or before [INSERT DATE 30 DAYS AFTER DATE OF PUBLICATION IN THE

FEDERAL REGISTER].

ADDRESSES: The docket for this rulemaking, which includes Federal Register notices,

public meeting attendee lists and transcripts, comments, and other supporting

documents/materials, is available for review at www.regulations.gov. All documents in

the docket are listed in the www.regulations.gov index. However, not all documents

listed in the index may be publicly available, such as information that is exempt from

public disclosure.

The docket webpage can be found at www.regulations.gov/docket/EERE-2014-

BT-STD-0058. The docket webpage contains instructions on how to access all

documents, including public comments, in the docket.

3

For further information on how to submit a comment or review other public

comments and the docket, contact the Appliance and Equipment Standards Program staff

at (202) 287-1445 or by email: [email protected].

The U.S. Department of Justice Antitrust Division invites input from market

participants and other interested persons with views on the likely competitive impact of

the standards contained in this direct final rule. Interested persons may contact the

Antitrust Division at [email protected] on or before the date specified in the

DATES section. Please indicate in the “Subject” line of your email the title and Docket

Number of this direct final rule.

FOR FURTHER INFORMATION CONTACT:

Dr. Carl Shapiro, U.S. Department of Energy, Office of Energy Efficiency and

Renewable Energy, Building Technologies Office, EE-5B, 1000 Independence Avenue,

SW, Washington, DC, 20585-0121. Telephone: (202) 287-5649. Email:

ApplianceStandar[email protected]oe.gov.

Mr. Matthew Schneider, U.S. Department of Energy, Office of the General

Counsel, GC-33, 1000 Independence Avenue, SW, Washington, DC, 20585-0121.

SUPPLEMENTARY INFORMATION:

Table of Contents

I. Synopsis of the Direct Final Rule

A. Benefits and Costs to Consumers

4

B. Impact on Manufacturers

C. National Benefits and Costs

D. Conclusion

II. Introduction

A. Authority

B. Background

1. Current Standards

2. Current Test Procedure

3. The Joint Agreement

III. General Discussion

A. Scope of Coverage

B. Fairly Representative of Relevant Points of View

C. Technological Feasibility

1. General

2. Maximum Technologically Feasible Levels

D. Energy Savings

1. Determination of Savings

2. Significance of Savings

E. Economic Justification

1. Specific Criteria

a. Economic Impact on Manufacturers and Consumers

b. Savings in Operating Costs Compared to Increase in Price (LCC and PBP)

c. Energy Savings

d. Lessening of Utility or Performance of Products

e. Impact of Any Lessening of Competition

f. Need for National Energy Conservation

g. Other Factors

2. Rebuttable Presumption

IV. Methodology and Discussion of Related Comments

A. Market and Technology Assessment

1. Product Classes

2. Technology Options

B. Screening Analysis

1. Screened Out Technologies

a. Thermoelectric heating, electric only

b. Microwave, electric only

c. Indirect heating

d. RF drying, electric only

e. Ultrasonic drying, electric only

2. Remaining Technologies

C. Engineering Analysis

1. Efficiency Analysis

a. Baseline Efficiency Levels

b. Incremental Efficiency Levels

2. Cost Analysis

3. Cost-Efficiency Results

5

D. Markups Analysis

E. Energy Use Analysis

F. Life-Cycle Cost and Payback Period Analysis

1. Product Cost

2. Installation Cost

3. Annual Energy Consumption

4. Energy Prices

5. Maintenance and Repair Costs

6. Product Lifetime

7. Discount Rates

8. Energy Efficiency Distribution in the No-New-Standards Case

9. Payback Period Analysis

G. Shipments Analysis

H. National Impact Analysis

1. Product Efficiency Trends

2. National Energy Savings

3. Net Present Value Analysis

I. Consumer Subgroup Analysis

J. Manufacturer Impact Analysis

1. Overview

2. Government Regulatory Impact Model and Key Inputs

a. Manufacturer Production Costs

b. Shipments Projections

c. Capital and Product Conversion Costs

d. Manufacturer Markup Scenarios

3. Discussion of MIA Comments

K. Emissions Analysis

1. Air Quality Regulations Incorporated in DOE’s Analysis

L. Monetizing Emissions Impacts

1. Monetization of Greenhouse Gas Emissions

a. Social Cost of Carbon

b. Social Cost of Methane and Nitrous Oxide

c. Sensitivity Analysis Using Updated 2023 SC-GHG Estimates

2. Monetization of Other Emissions Impacts

M. Utility Impact Analysis

N. Employment Impact Analysis

O. Regulatory Impact Analysis

P. Other Comments

V. Analytical Results and Conclusions

A. Trial Standard Levels

B. Economic Justification and Energy Savings

1. Economic Impacts on Individual Consumers

a. Life-Cycle Cost and Payback Period

b. Consumer Subgroup Analysis

c. Rebuttable Presumption Payback

2. Economic Impacts on Manufacturers

6

a. Industry Cash Flow Analysis Results

b. Direct Impacts on Employment

c. Impacts on Manufacturing Capacity

d. Impacts on Subgroups of Manufacturers

e. Cumulative Regulatory Burden

3. National Impact Analysis

a. Significance of Energy Savings

b. Net Present Value of Consumer Costs and Benefits

c. Indirect Impacts on Employment

4. Impact on Utility or Performance of Products

5. Impact of Any Lessening of Competition

6. Need of the Nation to Conserve Energy

7. Other Factors

8. Summary of Economic Impacts

C. Conclusion

1. Benefits and Burdens of TSLs Considered for Consumer Clothes Dryer

Standards

2. Annualized Benefits and Costs of the Adopted Standards

VI. Procedural Issues and Regulatory Review

A. Review Under Executive Orders 12866, 13563 and 14094

B. Review Under the Regulatory Flexibility Act

C. Review Under the Paperwork Reduction Act

D. Review Under the National Environmental Policy Act of 1969

E. Review Under Executive Order 13132

F. Review Under Executive Order 12988

G. Review Under the Unfunded Mandates Reform Act of 1995

H. Review Under the Treasury and General Government Appropriations Act, 1999

I. Review Under Executive Order 12630

J. Review Under the Treasury and General Government Appropriations Act, 2001

K. Review Under Executive Order 13211

L. Information Quality

M. Congressional Notification

VII. Approval of the Office of the Secretary

I.

Synopsis of the Direct Final Rule

The Energy Policy and Conservation Act, Public Law 94-163, as amended

(“EPCA”),

1

authorizes DOE to regulate the energy efficiency of a number of consumer

1

All references to EPCA in this document refer to the statute as amended through the Energy Act of 2020,

Pub. L. 116-260 (Dec. 27, 2020), which reflect the last statutory amendments that impact Parts A and A-1

of EPCA.

7

products and certain industrial equipment. (42 U.S.C. 6291–6317) Title III, Part B of

EPCA

2

established the Energy Conservation Program for Consumer Products Other Than

Automobiles. (42 U.S.C. 6291–6309) These products include consumer clothes dryers,

the subject of this direct final rule. (42 U.S.C. 6292(a)(7))

Pursuant to EPCA, any new or amended energy conservation standard must,

among other things, be designed to achieve the maximum improvement in energy

efficiency that DOE determines is technologically feasible and economically justified.

(42 U.S.C. 6295(o)(2)(A)) Furthermore, the new or amended standard must result in

significant conservation of energy. (42 U.S.C. 6295(o)(3)(B))

In light of the above and under the authority provided by 42 U.S.C. 6295(p)(4),

DOE is issuing this direct final rule amending energy conservation standards for

consumer clothes dryers.

The adopted standard levels in this direct final rule were proposed in a letter

submitted to DOE jointly by groups representing manufacturers, energy and

environmental advocates, consumer groups, and a utility. This letter, titled “Energy

Efficiency Agreement of 2023” (hereafter, the “Joint Agreement”

3

), recommends specific

energy conservation standards for consumer clothes dryers that, in the commenters’ view,

would satisfy the EPCA requirements in 42 U.S.C. 6295(o). DOE subsequently received

letters of support from States—including New York, California, and Massachusetts

4

—

2

For editorial reasons, upon codification in the U.S. Code, Part B was redesignated Part A.

3

Available at www.regulations.gov/comment/EERE-2014-BT-STD-0058-0055.

4

Available at www.regulations.gov/comment/EERE-2014-BT-STD-0058-0056.

8

and utilities—including San Diego Gas and Electric (“SDG&E”) and Southern California

Edison (“SCE”)

5

—advocating for the adoption of the recommended standards.

In accordance with the direct final rule provisions at 42 U.S.C. 6295(p)(4), DOE

has determined that the recommendations contained in the Joint Agreement are compliant

with 42 U.S.C. 6295(o). As required by 42 U.S.C. 6295(p)(4)(A)(i), DOE is also

simultaneously publishing elsewhere in this Federal Register a notice of proposed

rulemaking (“NOPR”) that contains standards identical to those adopted in this direct

final rule. Consistent with the statute, DOE is providing a 110-day public comment

period on the direct final rule. (42 U.S.C. 6295(p)(4)(B)) If DOE determines that any

comments received provide a reasonable basis for withdrawal of the direct final rule

under 42 U.S.C. 6295(o) or any other applicable law, DOE will publish the reasons for

withdrawal and continue the rulemaking under the NOPR. (42 U.S.C. 6295(p)(4)(C)) See

section II.A of this document for more details on DOE’s statutory authority.

The amended standards that DOE is adopting in this direct final rule are the

efficiency levels recommended in the Joint Agreement (shown in Table I.1). The

standards are expressed in terms of the combined energy factor (“CEF

D2

”), measured in

pounds per kilowatt-hour (“lb/kWh”), as determined in accordance with DOE’s consumer

clothes dryer test procedure at title 10 of the Code of Federal Regulations (“CFR”) part

430, subpart B, appendix D2 (“appendix D2”). The CEF metric includes active mode,

standby mode, and off mode energy use. The amended standards recommended in the

5

Available at www.regulations.gov/comment/EERE-2014-BT-STD-0058-0057.

9

Joint Agreement are represented as trial standard level (“TSL”) 3 (hereinafter the

“Recommended TSL”) and are described in section V.A of this document. The Joint

Agreement’s standards for consumer clothes dryers apply to all products listed in Table

I.1 and manufactured in, or imported into, the United States starting on March 1, 2028.

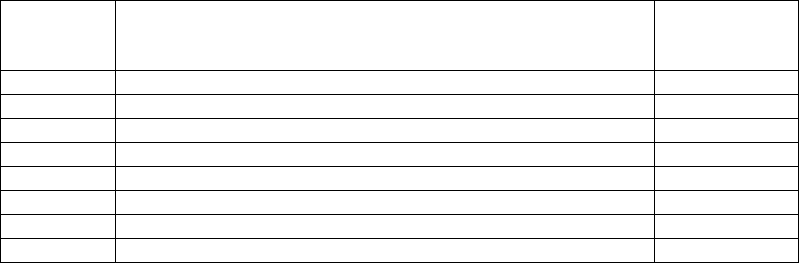

Table I.1 Energy Conservation Standards for Consumer Clothes Dryers

(Compliance Starting March 1, 2028)

Product Class

Minimum CEF

D2

(lb/kWh)

(i) Electric, Standard (4.4 cubic feet (“ft3”) or greater capacity)

3.93

(ii) Electric, Compact (120 volts (“V”)) (less than 4.4 ft3 capacity)

4.33

(iii) Vented Electric, Compact (240V) (less than 4.4 ft3 capacity)

3.57

(iv) Vented Gas, Standard (4.4 ft3 or greater capacity)

3.48

(v) Vented Gas, Compact (less than 4.4 ft3 capacity)

2.02

(vi) Ventless Electric, Compact (240V) (less than 4.4 ft3 capacity)

2.68

(vii) Ventless Electric, Combination Washer-Dryer

2.33

A. Benefits and Costs to Consumers

Table I.2 summarizes DOE’s evaluation of the economic impacts of the adopted

standards on consumers of consumer clothes dryers, as measured by the average life-

cycle cost (“LCC”) savings and the simple payback period (“PBP”).

6

The average LCC

savings are positive for all product classes, and the PBP is less than the average lifetime

of consumer clothes dryers, which is estimated to be 14 years (see section IV.F of this

document).

6

The average LCC savings refer to consumers that are affected by a standard and are measured relative to

the efficiency distribution in the no-new-standards case, which depicts the market in the compliance year in

the absence of new or amended standards (see section IV.F.9 of this document). The simple PBP, which is

designed to compare specific efficiency levels, is measured relative to the baseline product (see section

IV.C of this document).

10

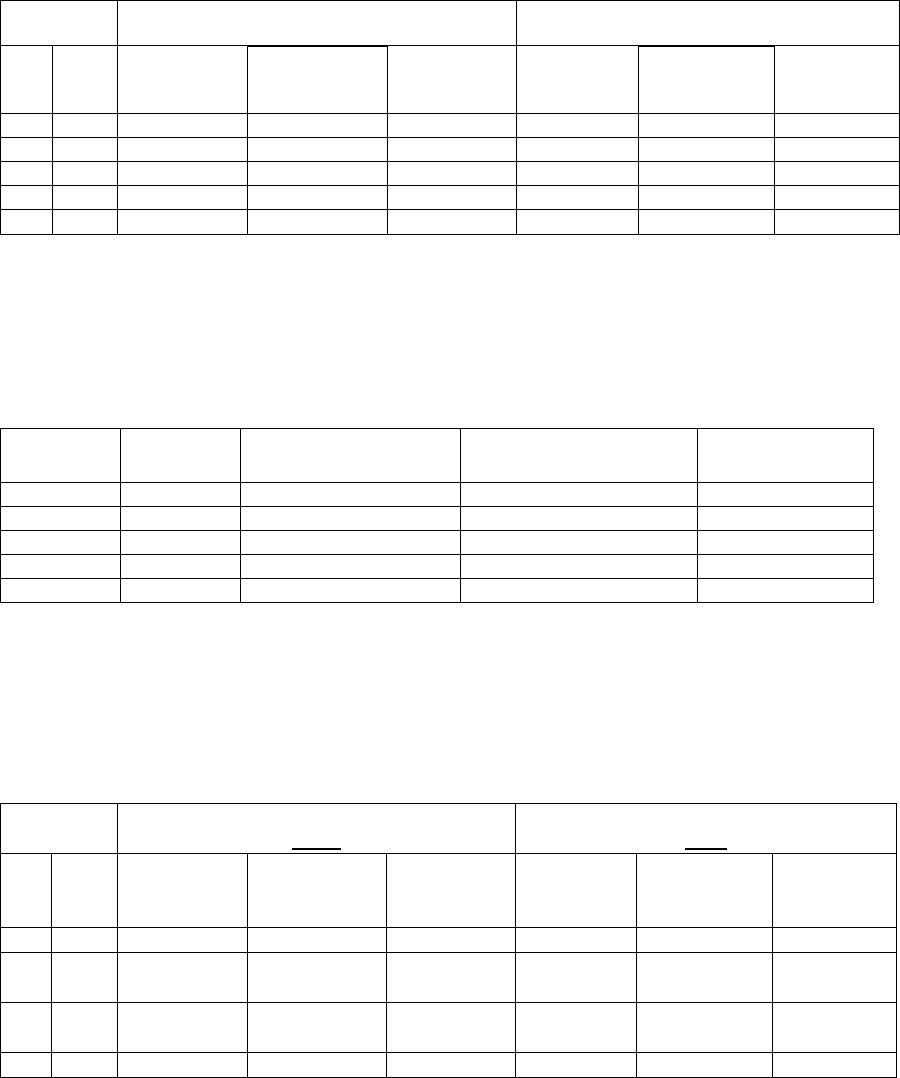

Table I.2 Impacts of Adopted Energy Conservation Standards on Consumers of

Consumer Clothes Dryers

Consumer Clothes Dryer Class

Average LCC Savings

(2022$)

Simple Payback Period

(years)

Electric, Standard (4.4 ft

3

or

greater capacity)

$252

0.6

Electric, Compact (120V) (less

than 4.4 ft

3

capacity)

$66 2.2

Vented Electric, Compact (240V)

(less than 4.4 ft

3

capacity)

$90 2.0

Vented Gas, Standard (4.4 ft

3

or

greater capacity)

$102 1.9

Ventless Electric, Compact

(240V) (less than 4.4 ft

3

capacity)

$99 0.4

Ventless Electric, Combination

Washer-Dryer

$11 0.0

DOE’s analysis of the impacts of the adopted standards on consumers is described

in section IV.F of this document.

B. Impact on Manufacturers

The industry net present value (“INPV”) is the sum of the discounted cash flows

to the industry from the base year (2024) through the end of the analysis period, which is

30 years from the analyzed compliance date.

7

Using a real discount rate of 7.5 percent,

DOE estimates that the INPV for manufacturers of consumer clothes dryers in the case

without amended standards is $2.12 billion in 2022$.

8

Under the adopted standards,

which align with the Recommended TSL for consumer clothes dryers, DOE estimates the

change in INPV to range from -6.8 percent to -5.7 percent, which is a decrease of

7

DOE’s analysis period extends 30 years from the compliance year. The analysis period for the MIA

ranges from 2024–2056 for the no-new-standards case and all TSLs, except for TSL 3 (the Recommended

TSL). The analysis period for the Recommended TSL ranges from 2024–2057 due to the 2028 compliance

year.

8

The no-new-standards case INPV of $2.12 billion reflects the sum of discounted free cash flows from

2024–2056 (from the reference year to 30 years after the 2027 compliance date) plus a discounted terminal

value.

11

approximately $144.2 million to a decrease of approximately $119.7 million. In order to

bring products into compliance with amended standards, it is estimated that industry will

incur total conversion costs of $180.7 million.

DOE’s analysis of the impacts of the adopted standards on manufacturers is

described in section IV.J and section V.B.2 of this document.

C. National Benefits and Costs

9

DOE’s analyses indicate that the adopted energy conservation standards for

consumer clothes dryers would save a significant amount of energy. Relative to the case

without amended standards, the lifetime energy savings for consumer clothes dryers

purchased in the 30-year period that begins in the anticipated year of compliance with the

amended standards (2028–2057), amount to 2.7 quadrillion British thermal units (“Btu”),

or quads.

10

This represents a savings of 11 percent relative to the energy use of these

products in the case without amended standards (referred to as the “no-new-standards

case”).

The cumulative net present value (“NPV”) of total consumer benefits of the

standards for consumer clothes dryers ranges from $ 9.23 billion (at a 7-percent discount

rate) to $20.08 billion (at a 3-percent discount rate). This NPV expresses the estimated

9

All monetary values in this document are expressed in 2022 dollars and, where appropriate, are

discounted to 2024 unless explicitly stated otherwise.

10

The quantity refers to full-fuel-cycle (“FFC”) energy savings. FFC energy savings includes the energy

consumed in extracting, processing, and transporting primary fuels (i.e., coal, natural gas, petroleum fuels),

and, thus, presents a more complete picture of the impacts of energy efficiency standards. For more

information on the FFC metric, see section IV.H.2 of this document.

12

total value of future operating-cost savings minus the estimated increased product and

installation costs for consumer clothes dryers purchased during the period 2028–2057.

In addition, the adopted standards for consumer clothes dryers are projected to

yield significant environmental benefits. DOE estimates that the standards will result in

cumulative emission reductions (over the same period as for energy savings) of 57.1

million metric tons (“Mt”)

11

of carbon dioxide (“CO

2

”), 13.9 thousand tons of sulfur

dioxide (“SO

2

”), 116.5 thousand tons of nitrogen oxides (“NO

X

”), 527.6 thousand tons of

methane (“CH

4

”), 0.5 thousand tons of nitrous oxide (“N

2

O”), and 0.1 tons of mercury

(“Hg”).

12

The estimated cumulative reduction in CO

2

emissions through 2030 amounts

to 1.3 Mt, which is equivalent to the emissions resulting from the annual electricity use of

more than 260 thousand homes.

DOE estimates the value of climate benefits from a reduction in greenhouse gases

(“GHG”) using four different estimates of the social cost of CO

2

(“SC-CO

2

”), the social

cost of methane (“SC-CH

4

”), and the social cost of nitrous oxide (“SC-N

2

O”). Together

these represent the social cost of GHG (“SC-GHG”). DOE used interim SC-GHG values

(in terms of benefit per ton of GHG avoided) developed by an Interagency Working

Group on the Social Cost of Greenhouse Gases (“IWG”).

13

The derivation of these values

11

A metric ton is equivalent to 1.1 short tons. Results for emissions other than CO

2

are presented in short

tons.

12

DOE calculated emissions reductions relative to the no-new-standards case, which reflects key

assumptions in the Annual Energy Outlook 2023 (“AEO2023”). AEO2023 represents current Federal and

State legislation and final implementation of regulations as of the time of its preparation. See section IV.K

of this document for further discussion of AEO2023 assumptions that affect air pollutant emissions.

13

To monetize the benefits of reducing GHG emissions, this analysis uses the interim estimates presented

in the Technical Support Document: Social Cost of Carbon, Methane, and Nitrous Oxide Interim Estimates

13

is discussed in section IV.L of this document. For presentational purposes, the climate

benefits associated with the average SC-GHG at a 3-percent discount rate are estimated

to be $3.3 billion. DOE does not have a single central SC-GHG point estimate and it

emphasizes the importance and value of considering the benefits calculated using all four

sets of SC-GHG estimates.

DOE estimated the monetary health benefits of SO

2

and NO

X

emissions

reductions, using benefit-per-ton estimates from the Environmental Protection Agency,

14

as discussed in section IV.L of this document. DOE estimated the present value of the

health benefits would be $2.6 billion using a 7-percent discount rate, and $6.3 billion

using a 3-percent discount rate.

15

DOE is currently only monetizing health benefits from

changes in ambient fine particulate matter (PM

2.5

) concentrations from two precursors

(SO

2

and NO

X

), and from changes in ambient ozone from one precursor (for NO

X

), but

will continue to assess the ability to monetize other effects such as health benefits from

reductions in direct PM

2.5

emissions.

Table I.3 summarizes the monetized benefits and costs expected to result from the

amended standards for consumer clothes dryers. There are other important unquantified

effects, including certain unquantified climate benefits, unquantified public health

Under Executive Order 13990 published in February 2021 by the IWG. (“February 2021 SC-GHG TSD”).

www.whitehouse.gov/wp-

content/uploads/2021/02/TechnicalSupportDocument_SocialCostofCarbonMethaneNitrousOxide.pdf.

14

U.S. EPA. Estimating the Benefit per Ton of Reducing Directly Emitted PM2.5, PM2.5 Precursors and

Ozone Precursors from 21 Sectors. Available at www.epa.gov/benmap/estimating-benefit-ton-reducing-

pm25-precursors-21-sectors.

15

DOE estimates the economic value of these emissions reductions resulting from the considered trial

standard levels (“TSLs”) for the purpose of complying with the requirements of Executive Order 12866.

14

benefits from the reduction of toxic air pollutants and other emissions, unquantified

energy security benefits, and distributional effects, among others.

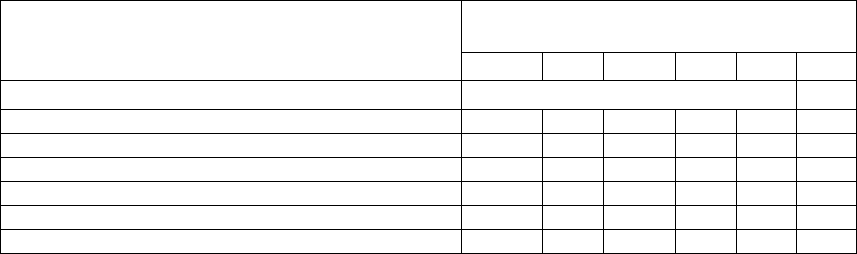

Table I.3 Summary of Monetized Benefits and Costs of Adopted Energy

Conservation Standards for Consumer Clothes Dryers

Billion (2022$)

3% discount rate

Consumer Operating Cost Savings 21.1

Climate Benefits* 3.3

Health Benefits** 6.3

Total Benefits† 30.7

Consumer Incremental Product Costs‡ 1.0

Net Monetized Benefits 20.1

Change in Producer Cash Flow (INPV

‡‡

) (0.14) – (0.12)

7% discount rate

Consumer Operating Cost Savings 9.8

Climate Benefits* (3% discount rate) 3.3

Health Benefits** 2.6

Total Benefits† 15.8

Consumer Incremental Product Costs‡ 0.6

Net Monetized Benefits 9.2

Change in Producer Cash Flow (INPV

‡‡

) (0.14) – (0.12)

Note: This table presents the costs and benefits associated with consumer clothes dryers shipped in 2028–

2057. These results include consumer, climate, and health benefits that accrue after 2057 from the products

shipped in 2028–2057.

* Climate benefits are calculated using four different estimates of the global SC-GHG (see section IV.L of

this document). For presentational purposes of this table, the climate benefits associated with the average

SC-GHG at a 3-percent discount rate are shown; however, DOE emphasizes the importance and value of

considering the benefits calculated using all four sets of SC-GHG estimates. To monetize the benefits of

reducing GHG emissions, this analysis uses the interim estimates presented in the Technical Support

Document: Social Cost of Carbon, Methane, and Nitrous Oxide Interim Estimates Under Executive Order

13990 published in February 2021 by the IWG.

** Health benefits are calculated using benefit-per-ton values for NO

X

and SO

2

. DOE is currently only

monetizing (for SO

2

and NO

X

) PM

2.5

precursor health benefits and (for NO

X

) ozone precursor health

15

benefits, but will continue to assess the ability to monetize other effects such as health benefits from

reductions in direct PM

2.5

emissions. See section IV.L of this document for more details.

† Total and net benefits include those consumer, climate, and health benefits that can be quantified and monetized. For

presentation purposes, total and net benefits for both the 3-percent and 7-percent cases are presented using the average

SC-GHG with a 3-percent discount rate.

‡ Costs include incremental equipment costs as well as installation costs.

‡‡ Operating Cost Savings are calculated based on the life cycle costs analysis and national impact analysis

as discussed in detail below. See sections IV.F and IV.H of this document. DOE’s national impact

analysis includes all impacts (both costs and benefits) along the distribution chain beginning with the

increased costs to the manufacturer to manufacture the product and ending with the increase in price

experienced by the consumer. DOE also separately conducts a detailed analysis on the impacts on

manufacturers (the MIA). See section IV.J of this document and chapter 12 of the direct final rule technical

support document (“TSD”). In the detailed MIA, DOE models manufacturers’ pricing decisions based on

assumptions regarding investments, conversion costs, cashflow, and margins. The MIA produces a range

of impacts, which is the rule’s expected impact on the INPV. The change in INPV is the present value of all

changes in industry cash flow, including changes in production costs, capital expenditures, and

manufacturer profit margins. Change in INPV is calculated using the industry weighted average cost of

capital value of 7.5 percent that is estimated in the MIA (see chapter 12 of the direct final rule TSD for a

complete description of the industry weighted average cost of capital). For consumer clothes dryers, those

values are -$144 million to -$120 million. DOE accounts for that range of likely impacts in analyzing

whether a TSL is economically justified. See section V.C of this document. DOE is presenting the range of

impacts to the INPV under two manufacturer markup scenarios: the Preservation of Gross Margin scenario,

which is the manufacturer markup scenario used in the calculation of Consumer Operating Cost Savings in

this table, and the Preservation of Operating Profit scenario, where DOE assumed manufacturers would not

be able to increase per-unit operating profit in proportion to increases in manufacturer production costs.

DOE includes the range of estimated change in INPV in the above table, drawing on the MIA explained

further in section IV.J of this document, to provide additional context for assessing the estimated impacts of

this direct final rule to society, including potential changes in production and consumption, which is

consistent with OMB’s Circular A-4 and E.O. 12866. If DOE were to include the INPV into the net benefit

calculation for this direct final rule, the net benefits would range from $19.96 billion to $19.98 billion at 3-

percent discount rate and would range from $9.06 billion to $9.08 billion at 7-percent discount rate.

Parentheses () indicate negative values.

The benefits and costs of the adopted standards can also be expressed in terms of

annualized values. The monetary values for the total annualized net benefits are (1) the

reduced consumer operating costs, minus (2) the increase in product purchase prices and

installation costs, plus (3) the value of climate and health benefits of emission reductions,

all annualized.

16

16

To convert the time-series of costs and benefits into annualized values, DOE calculated a present value in

2024, the year used for discounting the NPV of total consumer costs and savings. For the benefits, DOE

calculated a present value associated with each year’s shipments in the year in which the shipments occur

(e.g., 2020 or 2030), and then discounted the present value from each year to 2024. Using the present

value, DOE then calculated the fixed annual payment over a 30-year period, starting in the compliance

year, that yields the same present value.

16

The national operating cost savings are domestic private U.S. consumer monetary

savings that occur as a result of purchasing the covered products and are measured for the

lifetime of consumer clothes dryers shipped in 2028–2057. The benefits associated with

reduced emissions achieved as a result of the adopted standards are also calculated based

on the lifetime of consumer clothes dryers shipped in 2028–2057. Total benefits for both

the 3-percent and 7-percent cases are presented using the average GHG social costs with

a 3-percent discount rate. Estimates of SC-GHG values are presented for all four SC-

GHG discount rates in section IV.L of this document.

Table I.4 presents the total estimated monetized benefits and costs associated with

the adopted standards, expressed in terms of annualized values. The results under the

primary estimate are as follows.

Using a 7-percent discount rate for consumer benefits and costs and health

benefits from reduced NO

X

and SO

2

emissions, and the 3-percent discount rate case for

climate benefits from reduced GHG emissions, the estimated cost of the standards

adopted in this rule is $60.0 million per year in increased equipment costs, while the

estimated annual benefits are $971.4 million in reduced equipment operating costs,

$185.5 million in climate benefits, and $259.9 million in health benefits. In this case, the

net benefit would amount to $1,357 million per year.

Using a 3-percent discount rate for all benefits and costs, the estimated cost of the

standards is $57.2 million per year in increased equipment costs, while the estimated

annual benefits are $1,177 million in reduced operating costs, $185.5 million in climate

17

benefits, and $349.4 million in health benefits. In this case, the net benefit would amount

to $1,654 million per year.

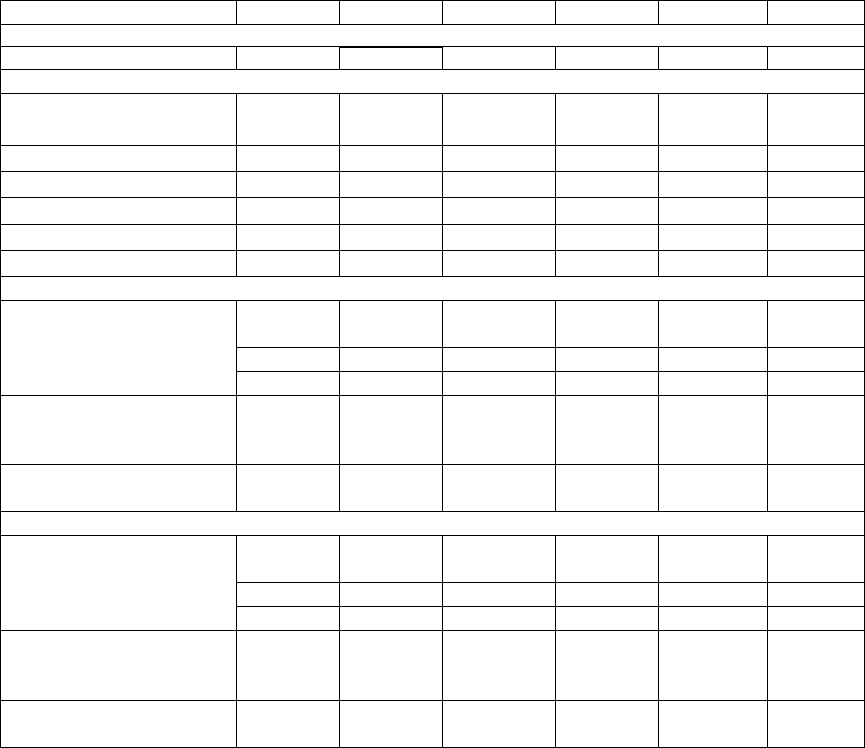

Table I.4 Annualized Benefits and Costs of Adopted Standards for Consumer

Clothes Dryers (2028−2057)

Million/year (2022$)

Primary Estimate

Low-Net-Benefits

Estimate

High-Net-

Benefits Estimate

3% discount rate

Consumer Operating Cost Savings 1,177 1,103 1,230

Climate Benefits* 185.5 178.9 187.8

Health Benefits** 349.4 337.2 353.7

Total Benefits† 1,712 1,619 1,771

Consumer Incremental Product Costs 57.2 58.9 54.4

Net Benefits 1,654 1,560 1,717

Change in Producer Cash Flow (INPV

‡‡

) (12) – (10) (12) – (10) (12) – (10)

7% discount rate

Consumer Operating Cost Savings 971.4 915.5 1,014

Climate Benefits* (3% discount rate) 185.5 178.9 187.8

Health Benefits** 259.9 251.5 262.8

Total Benefits† 1,417 1,346 1,464

Consumer Incremental Product Costs‡ 60.0 61.2 57.7

Net Benefits 1,357 1,285 1,407

Change in Producer Cash Flow (INPV

‡‡

) (12) - (10) (12) - (10) (12) - (10)

Note: This table presents the costs and benefits associated with consumer clothes dryers shipped in

2028−2057. These results include benefits to consumers which accrue after 2057 from the products

shipped in 2028−2057. The Primary, Low-Net-Benefits, and High-Net-Benefits estimates utilize

projections of energy prices from the AEO2023 Reference case, Low Economic Growth case, and High

Economic Growth case, respectively. In addition, incremental equipment costs reflect a medium decline

rate in the Primary Estimate, a constant rate in the Low-Net-Benefits Estimate, and a high decline rate in

the High-Net-Benefits Estimate. The methods used to derive projected price trends are explained in

sections IV.F.1 and IV.H.3 of this document. Note that the Benefits and Costs may not sum up to the Net

Benefits due to rounding.

* Climate benefits are calculated using four different estimates of the global SC-GHG (see section IV.L of

this document). For presentational purposes of this table, the climate benefits associated with the average

SC-GHG at a 3-percent discount rate are shown,

but DOE does not have a single central SC-GHG point estimate,

18

and it emphasizes the importance and value of considering the benefits calculated using all four sets of SC-

GHG estimates. To monetize the benefits of reducing GHG emissions, this analysis uses the interim

estimates presented in the Technical Support Document: Social Cost of Carbon, Methane, and Nitrous

Oxide Interim Estimates Under Executive Order 13990 published in February 2021 by the IWG.

** Health benefits are calculated using benefit-per-ton values for NO

X

and SO

2

. DOE is currently only

monetizing (for SO

2

and NO

X

) PM

2.5

precursor health benefits and (for NO

X

) ozone precursor health

benefits, but will continue to assess the ability to monetize other effects such as health benefits from

reductions in direct PM

2.5

emissions. See section IV.L of this document for more details.

† Total benefits for both the 3-percent and 7-percent cases are presented using the average SC-GHG with a

3-percent discount rate, but DOE does not have a single central SC-GHG point estimate.

‡ Costs include incremental equipment costs as well as installation costs.

‡‡ Operating Cost Savings are calculated based on the life cycle costs analysis and national impact analysis

as discussed in detail below. See sections IV.F and IV.H of this document. DOE’s national impact

analysis includes all impacts (both costs and benefits) along the distribution chain beginning with the

increased costs to the manufacturer to manufacture the product and ending with the increase in price

experienced by the consumer. DOE also separately conducts a detailed analysis on the impacts on

manufacturers (the MIA). See section IV.J of this document and chapter 12 of the direct final rule TSD. In

the detailed MIA, DOE models manufacturers’ pricing decisions based on assumptions regarding

investments, conversion costs, cashflow, and margins. The MIA produces a range of impacts, which is the

rule’s expected impact on the INPV. The change in INPV is the present value of all changes in industry

cash flow, including changes in production costs, capital expenditures, and manufacturer profit margins.

The annualized change in INPV is calculated using the industry weighted average cost of capital value of

7.5 percent that is estimated in the manufacturer impact analysis (see chapter 12 of the direct final rule TSD

for a complete description of the industry weighted average cost of capital). For consumer clothes dryers,

those values are -$12 million to -$10 million. DOE accounts for that range of likely impacts in analyzing

whether a TSL is economically justified. See section V.C of this document. DOE is presenting the range of

impacts to the INPV under two manufacturer markup scenarios: the Preservation of Gross Margin scenario,

which is the manufacturer markup scenario used in the calculation of Consumer Operating Cost Savings in

this table, and the Preservation of Operating Profit Markup scenario, where DOE assumed manufacturers

would not be able to increase per-unit operating profit in proportion to increases in manufacturer

production costs. DOE includes the range of estimated annualized change in INPV in the above table,

drawing on the MIA explained further in chapter 12 of this direct final rule TSD, to provide additional

context for assessing the estimated impacts of this direct final rule to society, including potential changes in

production and consumption, which is consistent with OMB’s Circular A-4 and E.O. 12866. If DOE were

to include the INPV into the annualized net benefit calculation for this direct final rule, the annualized net

benefits, using the primary estimate, would range from $1,642 million to $1,644 at 3-percent discount rate

and would range from $1,345 million to $1,347 million at 7-percent discount rate. Parentheses () indicate

negative values.

DOE’s analysis of the national impacts of the adopted standards is described in

sections IV.H, IV.K, and IV.L of this document.

D. Conclusion

DOE has determined that the Joint Agreement was submitted jointly by interested

persons that are fairly representative of relevant points of view, in accordance with 42

19

U.S.C. 6295(p)(4)(A). After considering the recommended standards and weighing the

benefits and burdens, DOE has determined that the recommended standards are in

accordance with 42 U.S.C. 6295(o), which contains the criteria for prescribing new or

amended standards. Specifically, the Secretary of Energy (“Secretary”) has determined

that the adoption of the recommended standards would result in the significant

conservation of energy and is the maximum improvement in energy efficiency that is

technologically feasible and economically justified. In determining whether the

recommended standards are economically justified, the Secretary has determined that the

benefits of the recommended standards exceed the burdens. The Secretary has further

concluded that the recommended standards, when considering the benefits of energy

savings, positive NPV of consumer benefits, emission reductions, the estimated monetary

value of the emissions reductions, and positive average LCC savings, would yield

benefits that outweigh the negative impacts on some consumers and on manufacturers,

including the conversion costs that could result in a reduction in INPV for manufacturers.

Using a 7-percent discount rate for consumer benefits and costs and NO

X

and SO

2

reduction benefits, and a 3-percent discount rate case for GHG social costs, the estimated

cost of the standards for consumer clothes dryers is $60.0 million per year in increased

product costs, while the estimated annual benefits are $971.4 million in reduced product

operating costs, $185.5 million in climate benefits, and $259.9 million in health benefits.

The net benefit amounts to $1,357 million per year. DOE notes that the net benefits are

20

substantial even in the absence of the climate benefits,

17

and DOE would adopt the same

standards in the absence of such benefits.

The significance of energy savings offered by a new or amended energy

conservation standard cannot be determined without knowledge of the specific

circumstances surrounding a given rulemaking.

18

For example, some covered products

and equipment have most of their energy consumption occur during periods of peak

energy demand. The impacts of these products on the energy infrastructure can be more

pronounced than products with relatively constant demand. Accordingly, DOE evaluates

the significance of energy savings on a case-by-case basis.

As previously mentioned, the standards are projected to result in estimated

national energy savings of 2.7 quads FFC, the equivalent of the primary annual energy

use of 18 million homes. In addition, they are projected to reduce cumulative CO

2

emissions by 57.1 Mt. Based on these findings, DOE has determined the energy savings

from the standard levels adopted in this direct final rule are “significant” within the

meaning of 42 U.S.C. 6295(o)(3)(B). A more detailed discussion of the basis for these

conclusions is contained in the remainder of this document and the accompanying TSD.

Under the authority provided by 42 U.S.C. 6295(p)(4), DOE is issuing this direct

final rule amending the energy conservation standards for consumer clothes dryers.

17

The information on climate benefits is provided in compliance with Executive Order 12866.

18

Procedures, Interpretations, and Policies for Consideration in New or Revised Energy Conservation

Standards and Test Procedures for Consumer Products and Commercial/Industrial Equipment, 86 FR

70892, 70901 (Dec. 13, 2021).

21

Consistent with this authority, DOE is also simultaneously publishing elsewhere in this

Federal Register a NOPR proposing standards that are identical to those contained in this

direct final rule. See 42 U.S.C. 6295(p)(4)(A)(i).

II.

Introduction

The following section briefly discusses the statutory authority underlying this

direct final rule, as well as some of the relevant historical background related to the

establishment of standards for consumer clothes dryers.

A. Authority

EPCA authorizes DOE to regulate the energy efficiency of a number of consumer

products and certain industrial equipment. Title III, Part B of EPCA established the

Energy Conservation Program for Consumer Products Other Than Automobiles. These

products include consumer clothes dryers, the subject of this document. (42 U.S.C.

6292(a)(8)) EPCA prescribed energy conservation standards for these products (42

U.S.C. 6295(g)(3)), and directed DOE to conduct future rulemakings to determine

whether to amend these standards. (42 U.S.C. 6295(g)(4)) EPCA further provides that,

not later than 6 years after the issuance of any final rule establishing or amending a

standard, DOE must publish either a notice of determination that standards for the

product do not need to be amended, or a NOPR including new proposed energy

conservation standards (proceeding to a final rule, as appropriate). (42 U.S.C.

6295(m)(1))

22

The energy conservation program under EPCA consists essentially of four parts:

(1) testing, (2) labeling, (3) the establishment of Federal energy conservation standards,

and (4) certification and enforcement procedures. Relevant provisions of EPCA

specifically include definitions (42 U.S.C. 6291), test procedures (42 U.S.C. 6293),

labeling provisions (42 U.S.C. 6294), energy conservation standards (42 U.S.C. 6295),

and the authority to require information and reports from manufacturers (42 U.S.C.

6296).

Federal energy efficiency requirements for covered products established under

EPCA generally supersede State laws and regulations concerning energy conservation

testing, labeling, and standards. (42 U.S.C. 6297(a)–(c)) DOE may, however, grant

waivers of Federal preemption in limited instances for particular State laws or

regulations, in accordance with the procedures and other provisions set forth under

EPCA. (42 U.S.C. 6297(d))

Subject to certain criteria and conditions, DOE is required to develop test

procedures to measure the energy efficiency, energy use, or estimated annual operating

cost of each covered product. (42 U.S.C. 6295(o)(3)(A) and 42 U.S.C. 6295(r))

Manufacturers of covered products must use the prescribed DOE test procedure as the

basis for certifying to DOE that their products comply with the applicable energy

conservation standards adopted under EPCA and when making representations to the

public regarding the energy use or efficiency of those products. (42 U.S.C. 6293(c) and

6295(s)) Similarly, DOE must use these test procedures to determine whether the

products comply with standards adopted pursuant to EPCA. (42 U.S.C. 6295(s)) The

23

DOE test procedures for consumer clothes dryers appear at title 10 of the Code of Federal

Regulations (“CFR”) part 430, subpart B, appendix D1 (“appendix D1”) and appendix

D2 (“appendix D2”).

DOE must follow specific statutory criteria for prescribing new or amended

standards for covered products, including consumer clothes dryers. Any new or amended

standard for a covered product must be designed to achieve the maximum improvement

in energy efficiency that the Secretary determines is technologically feasible and

economically justified. (42 U.S.C. 6295(o)(2)(A) Furthermore, DOE may not adopt any

standard that would not result in the significant conservation of energy. (42 U.S.C.

6295(o)(3)(B))

Moreover, DOE may not prescribe a standard if DOE determines by rule that the

standard is not technologically feasible or economically justified. (42 U.S.C.

6295(o)(3)(B)) In deciding whether a proposed standard is economically justified, DOE

must determine whether the benefits of the standard exceed its burdens. (42 U.S.C.

6295(o)(3)(B)) DOE must make this determination after receiving comments on the

proposed standard, and by considering, to the greatest extent practicable, the following

seven statutory factors:

(1) The economic impact of the standard on manufacturers and consumers of the

products subject to the standard;

24

(2) The savings in operating costs throughout the estimated average life of the

covered products in the type (or class) compared to any increase in the price,

initial charges, or maintenance expenses for the covered products that are

likely to result from the standard;

(3) The total projected amount of energy (or as applicable, water) savings likely to

result directly from the standard;

(4) Any lessening of the utility or the performance of the covered products likely

to result from the standard;

(5) The impact of any lessening of competition, as determined in writing by the

Attorney General, that is likely to result from the standard;

(6) The need for national energy and water conservation; and

(7) Other factors the Secretary considers relevant.

(42 U.S.C. 6295(o)(2)(B)(i)(I)–(VII))

Further, EPCA, as codified, establishes a rebuttable presumption that a standard is

economically justified if the Secretary finds that the additional cost to the consumer of

purchasing a product complying with an energy conservation standard level will be less

than three times the value of the energy savings during the first year that the consumer

25

will receive as a result of the standard, as calculated under the applicable test procedure.

(42 U.S.C. 6295(o)(2)(B)(iii))

EPCA, as codified, also contains what is known as an “anti-backsliding”

provision, which prevents the Secretary from prescribing any amended standard that

either increases the maximum allowable energy use or decreases the minimum required

energy efficiency of a covered product. (42 U.S.C. 6295(o)(1)) Also, the Secretary may

not prescribe an amended or new standard if interested persons have established by a

preponderance of evidence that the standard is likely to result in the unavailability in the

United States in any covered product type (or class) of performance characteristics

(including reliability), features, sizes, capacities, and volumes that are substantially the

same as those generally available in the United States. (42 U.S.C. 6295(o)(4))

EPCA specifies requirements when promulgating an energy conservation standard

for a covered product that has two or more subcategories. A rule prescribing an energy

conservation standard for a type (or class) of product must specify a different standard

level for a type or class of products that has the same function or intended use if DOE

determines that products within such group (A) consume a different kind of energy from

that consumed by other covered products within such type (or class); or (B) have a

capacity or other performance-related feature which other products within such type (or

class) do not have and such feature justifies a higher or lower standard. (42 U.S.C.

6295(q)(1)) In determining whether a performance-related feature justifies a different

standard for a group of products, DOE consider such factors as the utility to the consumer

of such a feature and other factors DOE deems appropriate. Id. Any rule prescribing such

26

a standard must include an explanation of the basis on which such higher or lower level

was established. (42 U.S.C. 6295(q)(2))

Additionally, pursuant to the amendments contained in the Energy Independence

and Security Act of 2007 (“EISA 2007”), Pub. L. 110-140, final rules for new or

amended energy conservation standards promulgated after July 1, 2010, are required to

address standby mode and off mode energy use. (42 U.S.C. 6295(gg)(3)) Specifically,

when DOE adopts a standard for a covered product after that date, it must, if justified by

the criteria for adoption of standards under EPCA (42 U.S.C. 6295(o)), incorporate

standby mode and off mode energy use into a single standard, or, if that is not feasible,

adopt a separate standard for such energy use for that product. (42 U.S.C.

6295(gg)(3)(A)–(B)) DOE’s current test procedures for consumer clothes dryers address

standby mode and off mode energy use, as do the amended standards adopted in this

direct final rule.

Finally, EISA 2007 amended EPCA, in relevant part, to grant DOE authority to

directly issue a final rule (i.e., a “direct final rule”) establishing an energy conservation

standard upon receipt of a statement submitted jointly by interested persons that are fairly

representative of relevant points of view (including representatives of manufacturers of

covered products, States, and efficiency advocates), as determined by the Secretary, that

contains recommendations with respect to an energy or water conservation standard. (42

U.S.C. 6295(p)(4)) Pursuant to 42 U.S.C. 6295(p)(4), the Secretary must also determine

whether a jointly submitted recommendation for an energy or water conservation

standard satisfies 42 U.S.C. 6295(o) or 42 U.S.C. 6313(a)(6)(B), as applicable.

27

The direct final rule must be published simultaneously with a NOPR that proposes

an energy or water conservation standard that is identical to the standard established in

the direct final rule, and DOE must provide a public comment period of at least 110 days

on this proposal. (42 U.S.C. 6295(p)(4)(A)–(B)) While DOE typically provides a

comment period of 60 days on proposed standards, for a NOPR accompanying a direct

final rule, DOE provides a comment period of the same length as the comment period on

the direct final rule—i.e., 110 days. Based on the comments received during this period,

the direct final rule will either become effective, or DOE will withdraw it not later than

120 days after its issuance if: (1) one or more adverse comments is received, and (2)

DOE determines that those comments, when viewed in light of the rulemaking record

related to the direct final rule, may provide a reasonable basis for withdrawal of the direct

final rule under 42 U.S.C. 6295(o). (42 U.S.C. 6295(p)(4)(C)) Receipt of an alternative

joint recommendation may also trigger a DOE withdrawal of the direct final rule in the

same manner. (Id.)

DOE has previously explained its interpretation of its direct final rule authority. In

a final rule amending the Department’s “Procedures, Interpretations and Policies for

Consideration of New or Revised Energy Conservation Standards for Consumer

Products” at 10 CFR part 430, subpart C, appendix A (“Process Rule” or “appendix A”),

DOE noted that it may issue standards recommended by interested persons that are fairly

representative of relative points of view as a direct final rule when the recommended

standards are in accordance with 42 U.S.C. 6295(o) or 42 U.S.C. 6313(a)(6)(B), as

applicable. 86 FR 70892, 70912 (Dec. 13, 2021). But the direct final rule provision in

EPCA does not impose additional requirements applicable to other standards

28

rulemakings, which is consistent with the unique circumstances of rules issued through

consensus agreements under DOE’s direct final rule authority. Id. DOE's discretion

remains bounded by its statutory mandate to adopt a standard that results in the maximum

improvement in energy efficiency that is technologically feasible and economically

justified—a requirement found in 42 U.S.C. 6295(o). Id. As such, DOE’s review and

analysis of the Joint Agreement is limited to whether the recommended standards satisfy

the criteria in 42 U.S.C. 6295(o).

B. Background

1. Current Standards

In a direct final rule published on April 21, 2011, (“April 2011 Direct Final

Rule”) DOE prescribed the current energy conservation standards for consumer clothes

dryers manufactured on and after January 1, 2015. 76 FR 22454.

19

These standards are

set forth in DOE’s regulations at 10 CFR 430.32(h)(3) and are shown in Table II.1.

These standards are consistent with a prior joint proposal submitted to DOE by interested

parties representing manufacturers, energy and environmental advocates, and consumer

groups.

20

The current standards are defined in terms of a minimum allowable CEF, as

measured according to appendix D1. Even though DOE maintained the same energy

19

DOE published a confirmation of effective date and compliance date for the direct final rule on August

24, 2011. 76 FR 52854.

20

Available at: www.regulations.gov/comment/EERE-2007-BT-STD-0010-0049.

29

efficiency descriptor for both appendix D1 and appendix D2, DOE notes that the CEF

values are not equivalent because of the extensive differences in test methods.

21

To avoid

potential confusion that would result from using the same efficiency descriptor for both

test procedures as it relates to the standards discussed in this document, DOE is including

a “D1” or “D2” subscript when referring to the appendix D1 CEF and appendix D2 CEF,

respectively (“CEF

D1

” and “CEF

D2

”).

Table II.1 Federal Energy Efficiency Standards for Consumer Clothes Dryers as

Measured Under Appendix D1

Product Class

CEF

D1

(lb/kWh)

(i) Vented Electric, Standard (4.4 ft

3

or greater capacity)

3.73

(ii) Vented Electric, Compact (120V) (less than 4.4 ft

3

capacity)

3.61

(iii) Vented Electric, Compact (240V) (less than 4.4 ft

3

capacity)

3.27

(iv) Vented Gas

3.30

(v) Ventless Electric, Compact (240V) (less than 4.4 ft

3

capacity)

2.55

(vi) Ventless Electric, Combination Washer-Dryer

2.08

2. Current Test Procedure

On October 8, 2021, DOE published a final rule for the test procedure rulemaking

(86 FR 56608) (the “October 2021 TP Final Rule”), in which it amended appendix D1

and appendix D2, both entitled “Uniform Test Method for Measuring the Energy

Consumption of Clothes Dryers,” to provide additional detail in response to questions

from manufacturers and test laboratories, including additional detail regarding the testing

of “connected” models, dryness level selection, and the procedures for maintaining the

21

While the current standards are based on CEF as determined in accordance with appendix D1,

manufacturers are permitted to use the appendix D2 test procedure to comply with the current standards, as

long as they use a single appendix for all representations. Beginning on the compliance date of the

amended standards established by this direct final rule, manufacturers will be required to use appendix D2

to comply with the amended standards.

30

required heat input rate for gas consumer clothes dryers; additional detail for the test

procedures for performing inactive and off mode power measurements; specifications for

the final moisture content (“FMC”) required for testing automatic termination control

dryers; specification of a narrower scale resolution for the weighing scale used to

determine moisture content of test loads; and specification that the test load must be

weighed within 5 minutes after a test cycle has terminated. In addition, as part of the

October 2021 TP Final Rule, DOE amended the test procedures to update the estimated

number of annual use cycles for consumer clothes dryers; provide further direction for

additional provisions within the test procedures; specify rounding requirements for all

reported values; apply consistent use of nomenclature and correct typographical errors;

remove obsolete sections of the test procedures, including appendix D; and update the

reference to the applicable industry test procedure to the version certified by the

American National Standards Institute (“ANSI”). 86 FR 56608, 56610.

DOE’s current energy conservation standards for consumer clothes dryers are

expressed in terms of CEF

D1

. (See 10 CFR 430.32(h)(3).) Appendix D1 tests timed

drying cycles, and accounts for clothes dryers with automatic termination controls by

applying a higher field use factor to units that have this feature. Appendix D2 tests

“normal” automatic termination cycles and more accurately measures the effects of

automatic cycle termination.

EPCA authorizes DOE to design test procedures that measure energy efficiency,

energy use, water use, or estimated annual operating cost of a covered product during a

representative average use cycle or period of use. (42 U.S.C. 6293(b)(3)) The appendix

31

D2 test procedure, which is required for use to demonstrate compliance with the amended

energy conservation standards established in this direct final rule, measures the energy

consumption of a representative use cycle that dries a load of laundry from an initial

moisture content of 57.5 percent to an FMC of less than 2 percent. 86 FR 56624-56625.

For timer clothes dryers, the test load is dried until the FMC is between 1 and 2.5 percent

of the bone-dry weight of the test load. The measured energy consumption is then

normalized to determine the energy consumption required to dry the test load to 2-percent

FMC, with a field use factor applied to account for the over-drying energy consumption.

For automatic termination control clothes dryers, appendix D2 specifies that a “normal”

program be selected for the test cycle, and for clothes dryers that do not have a “normal”

program, the cycle recommended by the manufacturer for drying cotton or linen shall be

selected. If the drying temperature and drying level settings can be chosen independently

of the program, they shall be set at the maximum drying temperature setting, and at a

“normal” or “medium” dryness level setting. The test is considered valid if the FMC of

the test load is 2 percent or less after the completion of the test cycle. If the FMC is

greater than 2 percent, the test is considered invalid and a new run shall be conducted

using the highest dryness level setting.

The current 2-percent FMC requirement using the DOE test cloth was adopted as

representative of approximately 5-percent FMC for “real-world” clothing, based on data

submitted in a joint petition for rulemaking.

22

DOE determined in the final rule published

22

The petition was submitted by AHAM, Whirlpool Corporation, General Electric Company, Electrolux,

LG Electronics, Inc., BSH, Alliance Laundry Systems, Viking Range, Sub-Zero Wolf, Friedrich A/C, U-

Line, Samsung, Sharp Electronics, Miele, Heat Controller, AGA Marvel, Brown Stove, Haier, Fagor

32

on August 14, 2013, that established the appendix D2 Test procedure that the specified 2-

percent FMC using the DOE test load was representative of consumer expectations for

dryness of clothing in field use. 78 FR 49608, 49620–49622, 49610–49611. DOE did not

amend the FMC requirements in the October 2021 TP Final Rule. 86 FR 56626.

DOE has conducted the rulemaking analysis for this direct final rule based on

CEF

D2

because compliance with the amended energy conservation standards established

in this direct final rule must be determined based on the use of appendix D2. DOE

discusses additional details in section IV.C.1 of this document about how it developed the

engineering baseline, in terms of CEF

D2

, from the current consumer clothes dryer

standards that are in terms of CEF

D1

.

3. The Joint Agreement

On September 25, 2023, DOE received a joint statement of recommended

standards (i.e., the Joint Agreement) for various home appliance products, including

consumer clothes dryers, submitted jointly by groups representing manufacturers, energy

and environmental advocates, consumer groups, and a utility.

23

In addition to the

America, Airwell Group, Arcelik, Fisher & Paykel, Scotsman Ice, Indesit, Kuppersbusch, Kelon, and

DeLonghi, American Council for an Energy Efficient Economy, Appliance Standards Awareness Project,

Natural Resources Defense Council, Alliance to Save Energy, Alliance for Water Efficiency, Northwest

Power and Conservation Council, and Northeast Energy Efficiency Partnerships, Consumer Federation of

America and the National Consumer Law Center. See Docket No. EERE–2011–BT–TP– 0054, No. 3.

23

The signatories to the Joint Agreement include AHAM, American Council for an Energy-Efficient

Economy, Alliance for Water Efficiency, Appliance Standards Awareness Project, Consumer Federation of

America, Consumer Reports, Earthjustice, National Consumer Law Center, Natural Resources Defense

Council, Northwest Energy Efficiency Alliance, and Pacific Gas and Electric Company. Members of

AHAM’s Major Appliance Division that make the affected products include: Alliance Laundry Systems,

LLC; Asko Appliances AB; Beko US Inc.; Brown Stove Works, Inc.; BSH Home Appliances Corporation;

Danby Products, Ltd.; Electrolux Home Products, Inc.,; Elicamex S.A. de C.V.; Faber; Fotile America; GE

Appliances, a Haier Company; L’Atelier Paris Haute Design LLG; LG Electronics; Liebherr USA, Co.;

33

recommended standards for consumer clothes dryers, the Joint Agreement also included

separate recommendations for several other covered products.

24

And, while

acknowledging that DOE may implement these recommendations in separate

rulemakings, the Joint Agreement also stated that the recommendations were

recommended as a complete package and each recommendation is contingent upon the

other parts being implemented. DOE understands this to mean that the Joint Agreement

is contingent upon DOE initiating rulemaking processes to adopt all of the recommended

standards in the agreement. That is distinguished from an agreement where issuance of an

amended energy conservation standard for a covered product is contingent on issuance of

amended energy conservation standards for the other covered products. If the Joint

Agreement were so construed, it would conflict with the anti-backsliding provision in 42

U.S.C. 6295(o)(1), because it would imply the possibility that, if DOE were unable to

issue an amended standard for a certain product, it would have to withdraw a previously

issued standard for one of the other products. The anti-backsliding provision, however,

prevents DOE from withdrawing or amending an energy conservation standard to be less

stringent. As a result, DOE will be proceeding with individual rulemakings that will

evaluate each of the recommended standards separately under the applicable statutory

criteria.

Midea America Corp.; Miele, Inc.; Panasonic Appliances Refrigeration Systems (PAPRSA) Corporation of

America; Perlick Corporation; Samsung Electronics America Inc; Sharp Electronics Corporation; Smeg

S.p.A; Sub-Zero Group, Inc.; The Middleby Corporation; U-Line Corporation; Viking Range, LLC; and

Whirlpool Corporation.

24

The Joint Agreement contained recommendations for 6 covered products: refrigerators, refrigerator-

freezers, and freezers; clothes washers; clothes dryers; dishwashers; cooking products; and miscellaneous

refrigeration products.

34

A court decision issued after DOE received the Joint Agreement is also relevant

to this rule. On March 17, 2022, various States filed a petition seeking review of a final

rule revoking two final rules that established product classes for residential dishwashers

with a cycle time for the normal cycle of 60 minutes or less, top-loading residential

clothes washers (“RCWs”) and certain classes of consumer clothes dryers with a cycle

time of less than 30 minutes, and front-loading RCWs with a cycle time of less than 45

minutes (collectively, “short cycle product classes”). The petitioners argued that the final

rule revoking the short cycle product classes violated EPCA and was arbitrary and

capricious. On January 8, 2024, the United States Court of Appeals for the Fifth Circuit

granted the petition for review and remanded the matter to DOE for further proceedings

consistent with the Fifth Circuit’s opinion. See Louisiana v. United States Department of

Energy, 90 F.4th 461 (5th Cir. 2024). On February 14, 2024, following the Fifth Circuit’s

decision in Louisiana v. United States Department of Energy, DOE received a second

joint statement from this same group of stakeholders in which the signatories reaffirmed

the Joint Agreement, stating that the recommended standards represent the maximum

levels of efficiency that are technologically feasible and economically justified.

25

In the

letter, the signatories clarified that “short-cycle” product classes for RCWs, clothes

dryers, and dishwashers did not exist at the time that the signatories submitted their

recommendations and it is their understanding that these classes also do not exist at the

current time. Accordingly, the parties clarified that the Joint Agreement did not address

short-cycle product classes. The signatories also stated that they did not anticipate that the

25

This document is available in the docket at: www.regulations.gov/comment/EERE-2014-BT-STD-0058-

0058.

35

recommended energy conservation standards in the Joint Agreement will negatively

affect features or performance, including cycle time, for consumer clothes dryers.

The Joint Agreement recommends amended standard levels for consumer clothes

dryers as presented in Table II.2. (Joint Agreement, No. 55 at p. 9)

26

Details of the Joint

Agreement recommendations for other products are provided in the Joint Agreement

posted in the docket.

27

Table II.2 Recommended Amended Energy Conservation Standards for Consumer

Clothes Dryers

Product Class

Minimum Energy

Efficiency Ratio

(lb/kWh)

Compliance Date

Electric, Standard (4.4 cubic feet (“ft

3

”) or greater

capacity)

3.93

March 1, 2028

Electric, Compact (120 volts (“V”)) (less than 4.4 ft

3

capacity)

4.33

Vented Electric, Compact (240V) (less than 4.4 ft

3

capacity)

3.57

Vented Gas, Standard (4.4 ft

3

or greater capacity)

3.48

Vented Gas, Compact (less than 4.4 ft

3

capacity)

2.02

Ventless Electric, Compact (240V) (less than 4.4 ft

3

capacity)

2.68

Ventless Electric, Combination Washer-Dryer

2.33

When the Joint Agreement was submitted, DOE was conducting a rulemaking to

consider amending the standards for consumer clothes dryers. As part of that process,

DOE published a NOPR and announced a public meeting on August 23, 2022 (“August

26

The parenthetical reference provides a reference for information located in the docket of DOE’s

rulemaking to develop energy conservation standards for consumer clothes dryers. (Docket No. EERE-

2014-BT-STD-0058, which is maintained at www.regulations.gov). The references are arranged as follows:

(commenter name, comment docket ID number at page of that document).

27

The Joint Agreement available in the docket at www.regulations.gov/comment/EERE-2014-BT-STD-

0058-0055.

36

2022 NOPR”) seeking comment on its proposed amended standard to inform its decision

consistent with its obligations under EPCA and the Administrative Procedure Act

(“APA”). 87 FR 51734. DOE subsequently held a public webinar on September 13,

2022, to discuss and receive comments on the NOPR TSD.

Although DOE is adopting the Joint Agreement as a direct final rule and no

longer proceeding with its prior rulemaking, DOE did consider relevant comments, data,

and information obtained during that rulemaking process in determining whether the

recommended standards from the Joint Agreement are in accordance with 42 U.S.C.

6295(o). Any discussion of comments, data, or information in this direct final rule that

were obtained during DOE’s prior rulemaking will include a parenthetical reference that

provides the location of the item in the public record.

28

III.

General Discussion

DOE is issuing this direct final rule after determining that the recommended

standards submitted in the Joint Agreement meet the requirements in 42 U.S.C.

6295(p)(4). More specifically, DOE has determined that the recommended standards

were submitted by interested persons that are fairly representative of relevant points of

view and the recommended standards satisfy the criteria in 42 U.S.C. 6295(o).

28

The parenthetical reference provides a reference for information located in the docket of DOE’s

rulemaking to develop energy conservation standards for consumer clothes dryers. (Docket No. EERE-

2014-BT-STD-0058, which is maintained at www.regulations.gov). The references are arranged as follows:

(commenter name, comment docket ID number at page of that document).

37

On March 17, 2022, various states filed a petition seeking review of a final rule

revoking two final rules that established product classes for residential dishwashers with

a cycle time for the normal cycle of 60 minutes or less, top-loading RCWs and certain

classes of consumer clothes dryers with a cycle time of less than 30 minutes, and front-

loading RCWs with a cycle time of less than 45 minutes (collectively, “short cycle

product classes”). The petitioners argued that the final rule revoking the short cycle

product classes violated EPCA and was arbitrary and capricious. On January 8, 2024, the

United States Court of Appeals for the Fifth Circuit granted the petition for review and

remanded the matter to DOE for further proceedings consistent with the Fifth Circuit’s

opinion. See Louisiana v. United States Department of Energy, 90 F.4th 461 (5th Cir.

2024)

Following the Fifth Circuit’s decision, the signatories to the Joint Agreement

submitted a second letter to DOE, which stated that Joint Recommendation did not

“address” “short-cycle product classes.”

29

That is because, as the letter explained, such

product classes “did not exist” at the time of the Joint Agreement.

In a recently issued Request for Information,

30

DOE is commencing a rulemaking

process on remand from the Fifth Circuit (the Remand Proceeding) by soliciting further

information, relevant to the issues identified by the Fifth Circuit, regarding any short

cycle product classes. In that Remand Proceeding, DOE will conduct the analysis

29

This document is available in the docket at: www.regulations.gov/comment/EERE-2014-BT-STD-0058-

0058.

30

See https://www1.eere.energy.gov/buildings/appliance_standards/standards.aspx?productid=50.

38

required by 42 U.S.C. 6295(q)(1)(B) to determine whether any short-cycle products have

a “capacity or other performance-related feature [that] . . . justifies a higher or lower

standard from that which applies (or will apply) to other products. ..... ”

The current standards applicable to any products within the scope of that

proceeding remain unchanged by this rule. See 10 CFR 430.32(g). Consistent with the

Joint Parties’ letter, short-cycle products are not subject to the amended standards

adopted by this direct final rule. If the short-cycle products that DOE will consider in the

Remand Proceeding were subject to these standards, that would have the practical effect

of limiting the options available in the Remand Proceeding. That is because EPCA’s anti-

backsliding provision precludes DOE from prescribing any amended standard “which

increases the maximum allowable energy use” of a covered product. 42

U.S.C. 6295(o)(1). Accordingly, were the products at issue in the Remand Proceeding

also subject to the amended standards adopted here, the Department could only reaffirm

the standards adopted in this direct final rule or adopt more stringent standards.

The Joint Agreement specifies the product classes for consumer clothes dryers:

electric, standard; electric, compact; vented electric, compact; vented gas, standard;

vented gas, compact; ventless electric, compact; and ventless electric, combination

washer-dryer. Although these product classes were not further divided by cycle time,

DOE understands them to exclude vented electric standard-size clothes dryers and vented

gas standard-size clothes dryers with a cycle time of less than 30 minutes, when tested

according to appendix D2. As previously noted, any such “short-cycle” consumer clothes

39

dryers will be considered in the Remand Proceeding; the current standards applicable to

such “short-cycle” consumer clothes dryers are unchanged by this rule.

Under the direct final rule authority at 42 U.S.C. 6295(p)(4), DOE evaluates

whether recommended standards are in accordance with criteria contained in 42 U.S.C.

6295(o). DOE does not have the authority to revise recommended standards submitted

under the direct final rule provision in EPCA. Therefore, DOE did not analyze any

additional product classes beyond those product classes included in the Joint Agreement.

That is, DOE has not separately considered or established amended standards applicable

to any short-cycle product classes. In the event that DOE establishes short-cycle product

classes, pursuant to the rulemaking on remand from the Fifth Circuit, DOE will

necessarily consider what amended standards ought to apply to any such product classes

and will do so in conformance with EPCA.

DOE notes that the data and analysis used to support this direct final rule includes

information for vented electric standard-size clothes dryers and vented gas standard-size

clothes dryers that is not distinguished by cycle time and is representative of all consumer

clothes dryers currently on the market today. To the extent that any short cycle product