www.pwc.co.uk/economics

Will robots really

steal our jobs?

An international analysis of

the potential long term

impact of automation

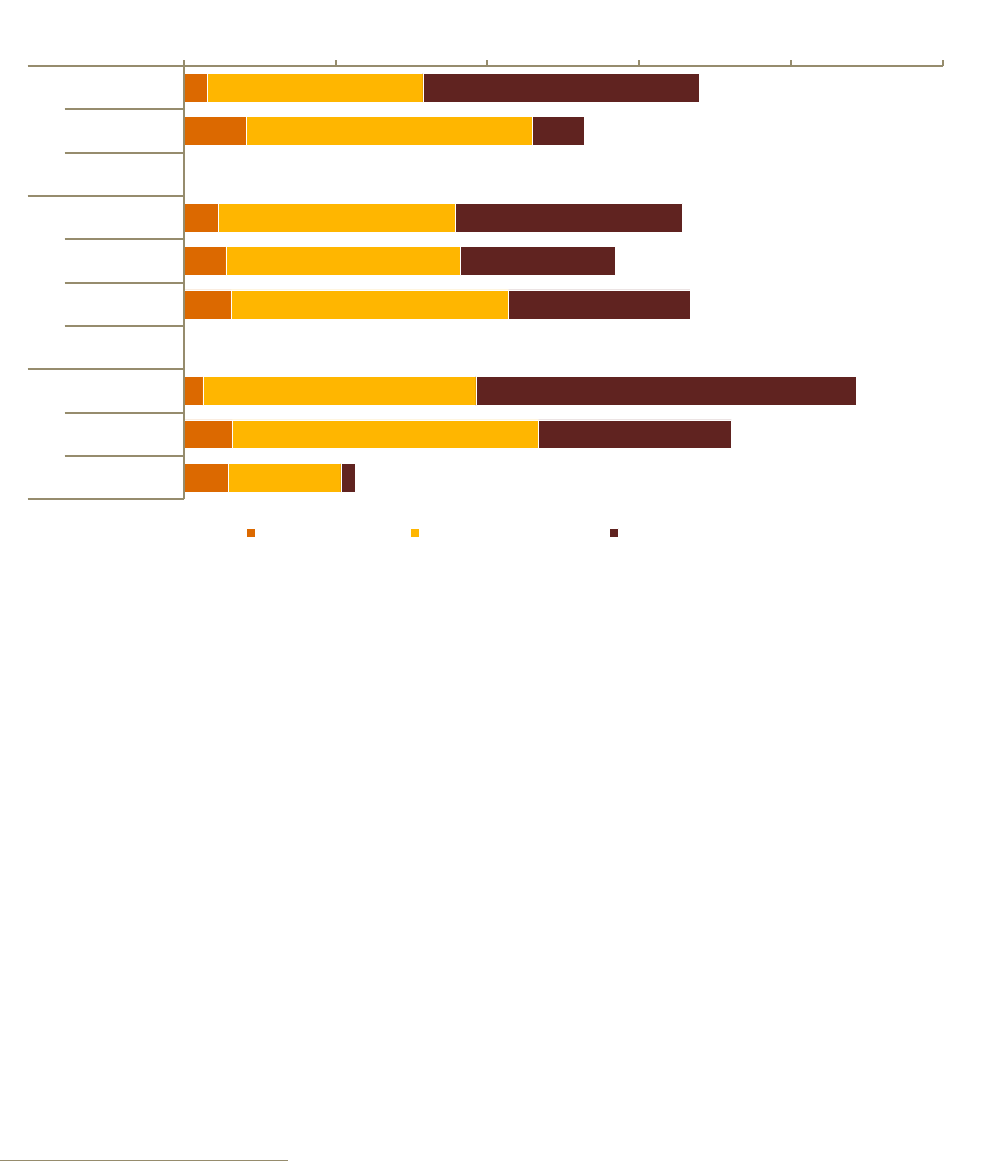

Key findings: impact of automation

Financial services jobs could be relatively

vulnerable to automation in the shorter term,

while transport jobs are more vulnerable to

automation in the longer term

Figure 1 – Potential job automation rates by

industry across waves

Source: PwC estimates based on OECD PIAAC data (median values for 29 countries)

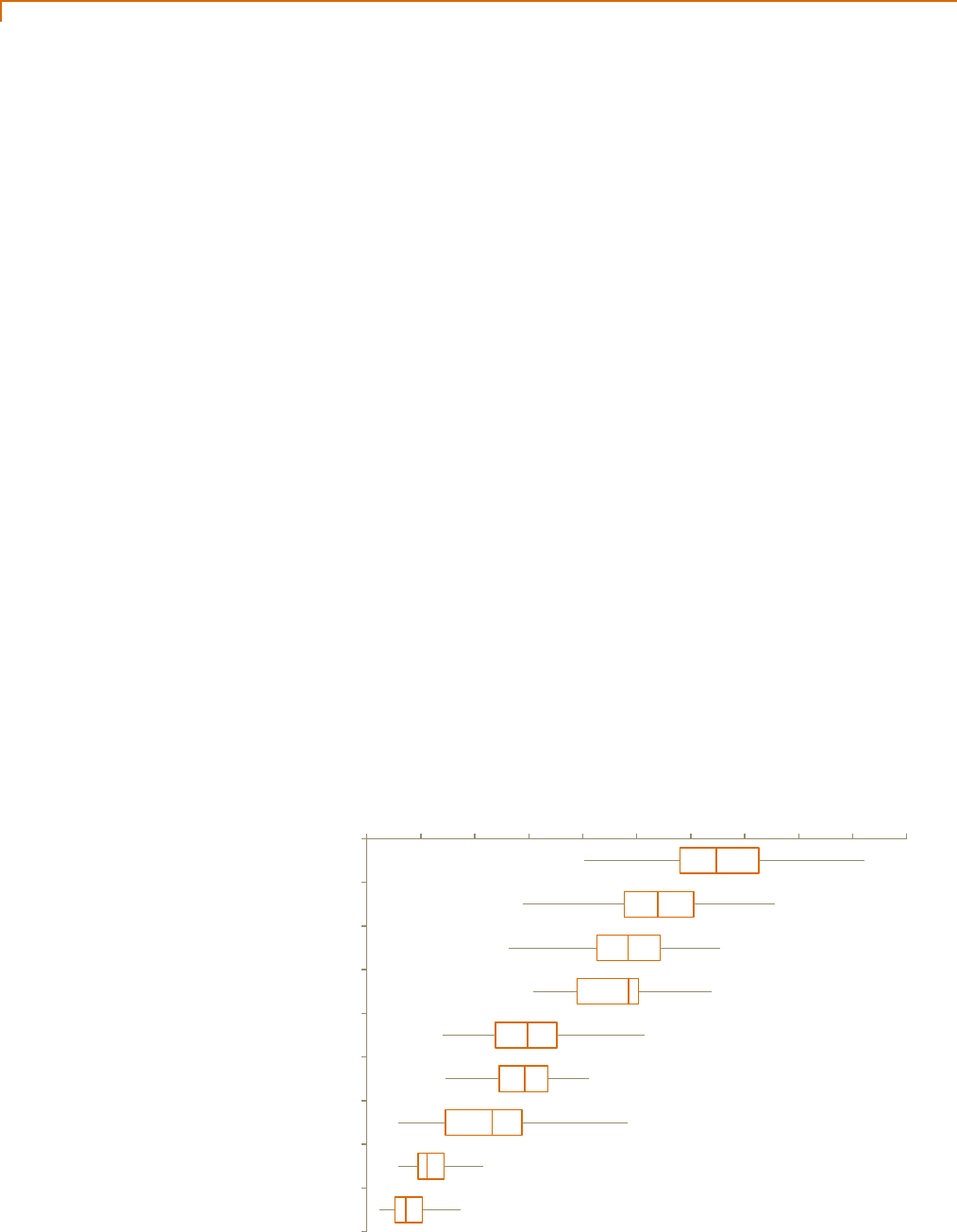

In the long run, less well educated workers

could be particularly exposed to automation,

emphasising the importance of increased

investment in lifelong learning and retraining

Figure 2 – Potential job automation rates by

education level across waves

Source: PwC estimates based on OECD PIAAC data (median values for 29 countries)

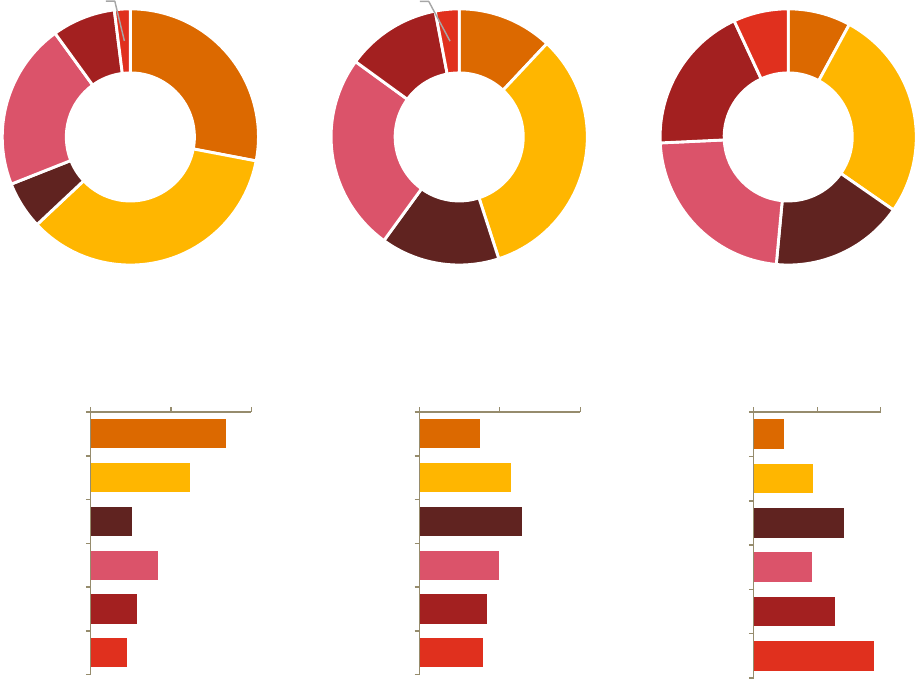

Female workers could be more affected by

automation over the next decade, but male jobs

could be more at risk in the longer term

Figure 3 – Potential job automation rates by

gender across waves

Source: PwC estimates based on OECD PIAAC data (median values for 29 countries)

Waves

Description and impact

Wave 1:

Algorithmic

wave (to early

2020s)

Automation of simple

computational tasks and

analysis of structured data,

affecting data-driven sectors

such as financial services.

Wave 2:

Augmentation

wave (to late

2020s)

Dynamic interaction with

technology for clerical support

and decision making. Also

includes robotic tasks in semi-

controlled environments such as

moving objects in warehouses.

Wave 3:

Autonomous

wave (to mid-

2030s)

Automation of physical labour

and manual dexterity, and

problem solving in dynamic real-

world situations that require

responsive actions, such as in

transport and construction.

0%

10%

20%

30%

40%

50%

Wave 1

(to early 2020s)

Wave 2

(to late 2020s)

Wave 3

(to mid-2030s)

% of existing jobs at potential risk of automation

Transport

Financial services

All sectors

Health

0% 10% 20% 30% 40% 50%

Wave 1

(to early 2020s)

Wave 2

(to late 2020s)

Wave 3

(to mid-2030s)

% of existing jobs at potential risk of automation

Low education

Medium education

High education

0% 5% 10% 15% 20% 25% 30% 35%

Wave 1

(to early 2020s)

Wave 2

(to late 2020s)

Wave 3

(to mid-2030s)

% of existing jobs at potential risk of automation

Men

All

Women

Will robots really steal our jobs?

An international analysis of the potential long term impact of automation PwC Contents

1. Summary 1

2. Introduction 7

3. How do potential automation rates vary by country? 9

3.1. Estimated potential automation rates across countries 9

3.2. The relative impact of industry composition and job automatability 10

3.3. Factors related to estimated automation levels 11

3.4. Impact on countries over time – the three waves of automation 14

3.5. Two important caveats – constraints on automation and new job creation 17

4. Which industry sectors could see the highest rates of

automation? 18

4.1. Total automation rates across industries 18

4.2. Impact on industries over time 20

4.3. Drivers of differences between industries 21

4.4. Which sectors are likely to see the largest jobs gains? 22

5. Which occupations could see the highest rates of automation? 23

5.1. Total automation risk across occupation categories 23

5.2. Impact over time by occupation 24

5.3. Drivers of differences between occupations 25

5.4. Composition of industries by occupational category 26

6. Why does the potential rate of job automation vary by type

of worker? 27

6.1. Total automation risk across workers 27

6.2. Potential automation rates by education level 30

7. What are the public policy implications? 34

7.1. Education and skills 34

7.2. Job creation through increased public and private investment 34

7.3. Enhancing social safety nets 35

8. Implications for business: constraints, opportunities

and responsibilities 36

8.1. What constraints will need to be overcome to realise benefits for business? 36

8.2. AI’s impact on company value chains 37

8.3. AI and healthcare provision 38

8.4. Businesses need to help workers retrain and adapt to new technologies 39

8.5. Conclusion 39

Annex – technical methodology 40

References 41

Authors, contacts and services 43

Contents

Will robots really steal our jobs?

An international analysis of the potential long term impact of automation PwC 1

Artificial intelligence (AI), robotics and other forms of ‘smart automation’ are advancing at a rapid pace and

have the potential to bring great benefits to the economy, by boosting productivity and creating new and better

products and services. In an earlier study

1

, we estimated that these technologies could contribute up to 14% to

global GDP by 2030, equivalent to around $15 trillion at today’s values.

For advanced economies like the US, the EU and Japan, these technologies could hold the key to reversing

the slump in productivity growth seen since the global financial crisis. But they could also produce a lot of

disruption, not least to the jobs market. Indeed a recent global PwC survey

2

found that 37% of workers were

worried about the possibility of losing their jobs due to automation.

To explore this further we have analysed a dataset compiled by the OECD that looks in detail at the tasks

involved in the jobs of over 200,000 workers across 29 countries (27 from the OECD plus Singapore and

Russia). Building on previous research by Frey and Osborne (Oxford University, 2013)

3

and Arntz, Gregory

and Zierahn (OECD, 2016)

4

we estimated the proportion of existing jobs that might be of high risk of

automation by the 2030s for:

Each of these 29 countries;

Different industry sectors;

Occupations within industries; and

Workers of different genders, ages and education levels.

We also identify how this process might unfold over the period to the 2030s in three overlapping waves:

1. Algorithm wave: focused on automation of simple computational tasks and analysis of structured data

in areas like finance, information and communications – this is already well underway.

2. Augmentation wave: focused on automation of repeatable tasks such as filling in forms, communicating

and exchanging information through dynamic technological support, and statistical analysis of

unstructured data in semi-controlled environments such as aerial drones and robots in warehouses – this is

also underway, but is likely to come to full maturity in the 2020s.

3. Autonomy wave: focused on automation of physical labour and manual dexterity, and problem solving in

dynamic real-world situations that require responsive actions, such as in manufacturing and transport (e.g.

driverless vehicles) – these technologies are under development already, but may only come to full maturity

on an economy-wide scale in the 2030s.

Our estimates are based primarily on the technical feasibility of automation, so in practice the actual extent of

automation may be less, due to a variety of economic, legal, regulatory and organisational constraints. Just

because something can be automated in theory does not mean it will be economically or politically viable

in practice.

1

PwC, ‘Sizing the prize’ (2017): https://www.pwc.com/gx/en/issues/data-and-analytics/publications/artificial-intelligence-study.html.

2

PwC, ‘Workforce of the future’ (2017): https://www.pwc.com/gx/en/services/people-organisation/publications/workforce-of-the-

future.html.

3

Frey, C.B. and M.A. Osborne (2013), The Future of Employment: How Susceptible are Jobs to Computerisation?, University of Oxford.

4

Arntz, M. T. Gregory and U. Zierahn (2016), ‘The risk of automation for jobs in OECD countries: a comparative analysis’, OECD Social,

Employment and Migration Working Papers No 189.

1. Summary

Will robots really steal our jobs?

An international analysis of the potential long term impact of automation PwC 2

Furthermore, other analysis we have done

5

suggests that any job losses from automation are likely to be

broadly offset in the long run by new jobs created as a result of the larger and wealthier economy made

possible by these new technologies. We do not believe, contrary to some predictions, that automation will lead

to mass technological unemployment by the 2030s any more than it has done in the decades since the digital

revolution began.

Nonetheless, automation will disrupt labour markets and it is interesting to look at the estimates we have

produced to get an indication of the relative exposure of existing jobs to automation in different countries,

industry sectors, and categories of workers. We summarise the key findings in these three areas in turn below.

Potential impacts by country

As Figure 1.1 shows, the estimated proportion of existing jobs at high risk of automation by the early 2030s

varies significantly by country. These estimates range from only around 20-25% in some East Asian and Nordic

economies with relatively high average education levels, to over 40% in Eastern European economies where

industrial production, which tends to be easier to automate, still accounts for a relatively high share of total

employment. Countries like the UK and the US, with services-dominated economies but also relatively long

‘tails’ of lower skilled workers, could see intermediate levels of automation in the long run.

Figure 1.1 – Potential job automation rates by country across waves

Source: PIAAC data, PwC analysis

5

This modelling was described in our report on the global economic impact of AI here: https://www.pwc.com/gx/en/issues/data-and-

analytics/publications/artificial-intelligence-study.html.

0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50%

svk

svn

ltu

cze

ita

usa

fra

deu

aut

esp

pol

tur

irl

nld

gbr

cyp

bel

dnk

isr

chl

sgp

nor

swe

nzl

jpn

rus

grc

fin

kor

Country

Potential jobs at high risk of automation

Algorithm wave Augmentation wave Autonomy wave

Will robots really steal our jobs?

An international analysis of the potential long term impact of automation PwC 3

Figure 1.1 also shows how potential automation rates might evolve by country over our three waves of

automation. Existing jobs in some countries with relatively low longer term automation rates, such as Japan,

may nonetheless be see relatively high automation rates in the shorter term given that algorithmic technologies

are already more widely used there.

The opposite is true for a country like Turkey, which may have relatively high exposure to later waves of

automation that start to displace manual workers such as drivers and construction workers, but relatively

lower exposure in the short term.

Potential impacts by industry sector

We also see significant variations in potential automation levels between industry sectors, although the pattern

here also varies across different waves as Figure 1.2 illustrates.

Figure 1.2 – Potential rates of job automation by industry across waves

Source: PIAAC data, PwC analysis

Transport stands out as a sector with particularly high potential for automation in the longer run as driverless

vehicles roll out at scale across economies, but this will be most evident in our third wave of autonomous

automation (which may only come to maturity in the 2030s). In the shorter term, sectors such as financial

services could be more exposed as algorithms outperform humans in an ever wider range of tasks involving

pure data analysis.

0% 10% 20% 30% 40% 50% 60%

Transportation and storage

Manufacturing

Construction

Administrative and support service

Wholesale and retail trade

Public administration and defence

Financial and insurance

Information and communication

Professional, scientific and technical

Accommodation and food service

Human health and social work

Education

Potential jobs at high risk of automation

Algorithm wave Augmentation wave Autonomy wave

Will robots really steal our jobs?

An international analysis of the potential long term impact of automation PwC 4

Potential impacts by type of worker

Our analysis also highlights significant differences in the potential impact of automation across types of workers

and these will also vary across our three waves of automation as Figure 1.3 shows.

Figure 1.3 – Potential job automation rates by type of worker across waves

Source: PIAAC data, PwC analysis

The starkest results are those by education level, with much lower potential automation rates on average for

highly educated workers with graduate degrees or above, than for those with low to medium education levels.

This reflects the greater adaptability of more highly educated workers to technological changes and the fact that

they are more likely to be in senior managerial roles that will still be needed to apply human judgement, as well

as to design and supervise AI-based systems. Such workers could see their wages increase due to the

productivity gains that these new technologies should bring.

Differences are less marked by age group, although some older workers could find it relatively harder to adapt

and retrain than younger cohorts. This may apply particularly to less well-educated men as we move into our

third wave of autonomous automation in areas like driverless cars and other manual labour that has a relatively

high proportion of male workers at present. But female workers could be relatively harder hit in early waves of

automation that apply, for example, to clerical roles.

Implications for public policy

The most obvious implication of our analysis is the need for increased investment in education and skills to

help people adapt to technological change throughout their careers. While increased training in digital skills

and STEM subjects

6

is one important element in this, it will also require retraining of, for example, truck

drivers to take jobs in services sectors where demand is high but automation is less easy due to the

importance of social skills and ‘the human touch’. Governments, business, trade unions and other organisations

(e.g. the NHS and social care providers in the UK) all need to play their part here in helping people to adapt to

these new technologies

7

. This will include training and retraining people in softer skills, such as creativity,

problem solving and flexibility. On-the-job training will be important here, for example through degree

6

Design and other creative skills may also be important here.

7

The recent UK government proposal in its November 2017 Budget for a new National Retraining Scheme involving both business and

trade unions is one example here. Further discussion of how people can be helped to adapt to new technologies is contained in our

Workforce of the Future report here: https://www.pwc.com/futureworkforce.

0% 10% 20% 30% 40% 50%

Male

Female

Young (<25)

Core (25-54)

Older (55+)

Low

Medium

High

Sex

Age group

Education level

Potential jobs at high risk of automation

Algorithm wave Augmentation wave Autonomy wave

Will robots really steal our jobs?

An international analysis of the potential long term impact of automation PwC 5

apprenticeships that offer a mix of theoretical study and practical experience, and that are open to a wide range

of people (including mature students) to promote social mobility.

In addition, it is important that aggregate demand levels are kept high so as to facilitate the creation of new

jobs. One obvious way to do this at present is through increased infrastructure investment (including areas such

as housing where this is in short supply as in the UK). Such investment is needed to support longer term

growth, but can also create many new jobs in construction and related sectors

8

. Governments can play a key

role here both in funding some investment directly and in helping to lever in additional private investment.

It is also important to recognise that concerns about the possible loss of existing jobs should not lead countries

to miss out on opportunities to lead the way in developing these new technologies. If governments and

businesses in one country do not invest in them, then they will just be developed elsewhere. Unless a country

blocks itself off from global trade and investment, which history shows would be extremely damaging

economically in the long run, the technologies will still come to all countries over time, so it is better to be at the

forefront of this global race.

However, governments do have a key role in making sure that the great potential benefits from AI, robotics and

related technologies are shared as broadly as possible across society. As well as investing more in education,

training and retraining, and protecting workers rights through appropriate legislation, governments should

consider using the tax proceeds from technology-driven growth to strengthen social safety nets for those who

lose out from automation.

Universal basic income (UBI) is one idea that has been discussed here. The case for this remains to be proven,

but it makes sense for governments to gather evidence from pilot schemes and microsimulation models to

inform future decisions on this and other options for sharing the benefits of technology more widely across

society. Optimal solutions here may involve combining different ideas (e.g. UBI-type schemes with a degree

of conditionality related to working, learning, training, caring or doing some other form of socially valuable

activity to qualify for such benefits).

Implications for business

Our research on AI, robotics and related technologies shows their huge potential to boost productivity and

create new and better products and services. There are large benefits to be reaped here by businesses in all

sectors, but the phasing of these may vary across different waves of automation (see Table 1.1). Of course,

many businesses will need to start investing now for later waves, but they also need to focus on the short-

term gains already available through emerging technology and algorithmic methods to enhance data analysis

and customer service.

Table 1.1: Key impacts in the three waves of automation

Phase

Description

Tasks impacted

Industries impacted

Algorithm

wave

Automation of simple

computational tasks and

analysis of structured data,

affecting data-driven

sectors such as

financial services.

This includes manually conducting

mathematical calculations, or using

basic software packages and internet

searches. Despite increasingly

sophisticated machine learning

algorithms being available and

increasingly commoditised, it is these

more fundamental computational job

tasks that will be most impacted first.

Data driven sectors like

financial and insurance,

information and

communication, and

professional, scientific

and technical services.

8

Of course, as our analysis shows, some construction jobs may also be automated in the long run to boost productivity, but if more

construction work is undertaken this will also boost the demand for human labour, particularly in the short to medium term.

Will robots really steal our jobs?

An international analysis of the potential long term impact of automation PwC 6

Phase

Description

Tasks impacted

Industries impacted

Augmentation

wave

Dynamic interaction

with technology for

clerical support and

decision making. Also

includes robotic tasks

in semi-controlled

environments such

as moving objects

in warehouses.

For example, routine tasks such as

filling in forms or exchanging

information, which includes the

physical transfer of information. It is

also likely to see a decreased need for

many programming languages as

repeatable programmable tasks are

increasingly automated, and through

machines themselves building and

redesigning learning algorithms.

The financial and insurance

sector will continue to be

highly impacted, along with

other sectors with a higher

proportion of clerical support,

including public and

administration,

manufacturing, and

transport and storage.

Autonomy

wave

Automation of physical

labour and manual

dexterity, and problem

solving in dynamic real-

world situations that

require responsive actions,

such as in transport

and manufacturing.

AI and robotics will further automate

routine tasks but also those tasks that

involve physical labour or manual

dexterity. This will include the

simulation of adaptive behaviour by

autonomous agents.

Sectors like construction,

water, sewage and waste

management, and

transportation and storage

with the advent of fully

autonomous vehicles

and robots.

Source: PwC analysis

Businesses also need to consider now how successive waves of AI-related technologies might further break

down barriers to entry in their sector and challenge existing business models. In addition to enhancing existing

propositions, it also allows business to offer the same proposition in a more cost effective way, which may be

particularly beneficial for small to medium sized businesses and start-ups. This will also create new

opportunities for successful businesses to leverage their distinctive competencies in adjacent sectors. Given the

fast pace of change, businesses need to be constantly experimenting with new technologies and creating options

that they can scale up quickly where successful.

Individuals also need to be more entrepreneurial, taking responsibility for their lifelong learning and seeking to

generate their own intellectual property and start new businesses. Much of the automation of the future may be

driven by these new businesses replacing or challenging established companies that find it harder to change.

At the same time, as we have argued in previous reports

9

, businesses and other employers need to adopt a

responsible approach to AI, both as regards their customers (e.g. as regards data privacy) and their workers

(e.g. helping them to develop the skills they need to prosper in an age of increasing automation and rapid

technological change).

By acting in this way

10

, businesses and governments can help to maximise the benefits of AI and robotics while

minimising as far as possible the negative impacts of these disruptive technologies.

9

See our website for more details on Responsible AI: https://www.pwc.co.uk/services/audit-assurance/risk-assurance/services/

technology-risk/technology-risk-insights/accelerating-innovation-through-responsible-ai/responsible-ai-framework.html.

10

For more on this, see the following G20 Policy Insights paper by various PwC authors: http://www.g20-

insights.org/policy_briefs/accelerating-labour-market-transformation/.

Will robots really steal our jobs?

An international analysis of the potential long term impact of automation PwC 7

The potential for disruption to labour markets due to advances in technology is not a new phenomenon. Most

famously, the Luddite protest movement of the early 19

th

century was a backlash by skilled handloom weavers

against the mechanisation of the British textile industry that emerged as part of the Industrial Revolution

(including the Jacquard loom, which with its punch card system was in some respects a forerunner of the

modern computer). But, in the long run, not only were there still many (if, on average, less skilled) jobs in the

new textile factories but, more important, the productivity gains from mechanisation created huge new wealth.

This in turn generated many more jobs across the UK economy in the long run than were initially lost in the

traditional handloom weaving industry.

The standard economic view for most of the last two centuries has therefore been that the Luddites were wrong

about the long-term benefits of the new technologies, even if they were right about the short-term impact on

their personal livelihoods. Anyone putting such arguments against new technologies has generally been

dismissed as believing in the ‘Luddite fallacy’.

However, over the past few years, fears of technology-driven job losses have re-emerged with advances in

‘smart automation’ – the combination of AI, robotics and other digital technologies that is already producing

innovations like driverless cars and trucks, intelligent virtual assistants like Siri, Alexa and Cortana, and

Japanese healthcare robots.

While traditional machines, including fixed location industrial robots, replaced our muscles (and those of other

animals like horses and oxen), these new smart machines have the potential to replace our minds and to move

around freely in the world driven by a combination of advanced sensors, GPS tracking systems and deep

learning - if not now, then probably within the next decade or two. Will this just have the same effects as past

technological leaps – short term disruption more than offset by long term economic gains? Or is this something

more fundamental in terms of taking humans out of the loop not just in manufacturing and routine service

sector jobs, but more broadly across the economy? What exactly will humans have to offer employers if smart

machines can perform all or most of their essential tasks better in the future

11

? In short, has the ‘Luddite fallacy’

finally come true?

This debate was given added urgency in 2013 when researchers at Oxford University (Frey and Osborne, 2013)

estimated that around 47% of total US employment had a ‘high risk of computerisation’ over the next couple of

decades – i.e. by the early 2030s.

However, there are also dissenting voices. Notably, Arntz, Gregory and Zierahn (OECD, 2016) re-examined the

research by Frey and Osborne and, using an extensive new OECD data set, came up with a much lower estimate

that only around 10% of jobs were under a ‘high risk

12

of computerisation’. This is based on the reasoning that

any predictions of job automation should consider the specific tasks that are involved in each job rather than

the occupation as a whole

13

.

In an earlier article in March 2017

14

we produced our own analysis of the potential effect of automation on jobs

with a focus on the UK. Using a more refined version of the OECD methodology, we concluded that up to 30%

of UK jobs could be impacted by automation by the 2030s. We also produced high level comparisons suggesting

somewhat lower potential automation rates in Japan and somewhat higher rates in Germany and the US.

11

Martin Ford, The Rise of the Robots (Oneworld Publications, 2015) is one particularly influential example of an author setting out this

argument in detail. Calum Chace (The Economic Singularity, 2016) also discusses these issues in depth.

12

In both studies, this is defined as an estimated probability of 70% or more. For comparability, we adopt the same definition of ‘high

risk’ in this report.

13

The importance of looking at tasks is also emphasised by Autor (2015).

14

‘Will robots steal our jobs?’ PwC UK Economic Outlook, March 2017, available here: https://www.pwc.co.uk/economic-

services/ukeo/pwcukeo-section-4-automation-march-2017-v2.pdf.

2. Introduction

Will robots really steal our jobs?

An international analysis of the potential long term impact of automation PwC 8

At the same time, we also emphasised that various economic, legal and regulatory and organisational factors

mean that these potential risks may not lead to actual job displacement. In some cases, it would alter the nature

of jobs significantly, but not displace humans entirely.

Furthermore, we emphasised that there were likely to be broadly offsetting job gains from the new technologies,

provided that the income and wealth gains from these advances were recycled into the economy. This

qualitative judgement was backed up by later detailed quantitative modelling

15

that concluded that the net long

term job impact of automation would be likely to be neutral or even slightly positive

16

. This will, however,

require both business and governments to provide support to workers affected by these technological advances

to retrain and start new careers.

In this paper, we extend our March 2017 analysis of jobs at potential risk of automation to a much wider set of

countries, using the OECD’s PIAAC database for 29 countries (27 from the OECD, plus Singapore and Russia).

In total, this covers the jobs of over 200,000 workers and so provides a much larger dataset to explore potential

impacts of automation by country, sector and type of worker. The additional data also allows us to provide a

more robust analysis of the factors causing automation risk to vary across countries and sectors.

We also identify how this process might unfold over the period to the 2030s in three overlapping waves:

1. Algorithm wave: focused on automation of simple computational tasks and analysis of structured data

in areas like finance, information and communications – this is already well underway.

2. Augmentation wave: focused on automation of repeatable tasks such as filling in forms, communicating

and exchanging information through dynamic technological support, and statistical analysis of

unstructured data in semi-controlled environments such as aerial drones and robots in warehouses –

this is also underway, but is likely to come to full maturity in the 2020s.

3. Autonomy wave: focused on automation of physical labour and manual dexterity, and problem solving in

dynamic real-world situations that require responsive actions, such as in manufacturing and transport (e.g.

driverless vehicles) – these technologies are under development already, but may only come to full maturity

on an economy-wide scale in the 2030s.

Report structure

The discussion in the rest of this report is structured as follows:

Section 3 – How do potential automation rates vary by country?

Section 4 – Which industry sectors could see the highest rates of automation?

Section 5 – Which occupations could see the highest rates of automation?

Section 6 – Why does the potential rate of job automation vary by type of worker?

Section 7 – What are the public policy implications?

Section 8 – Implications for business – constraints, opportunities and responsibilities.

Further details of the methodology behind our analysis are contained in a technical annex at the end of this

report, together with references to the studies cited.

15

This modelling was described in our report on the global impact of AI here: https://www.pwc.com/gx/en/issues/data-and-

analytics/publications/artificial-intelligence-study.html.

16

Other reports such as ZEW (2016) and Acemoglu and Restrepo (2016) also highlights the job creating potential of these new

technologies. However, an empirical study for the US manufacturing sector by Acemoglu and Restrepo (2017) found a net negative

impact on employment from industrial robots, so this remains an active area of debate.

Will robots really steal our jobs?

An international analysis of the potential long term impact of automation PwC 9

Key findings

The estimated share of existing jobs that could potentially be automated by the 2030s varies widely across

countries from only around 22% in Finland and South Korea to up to 44% in Slovakia.

Countries with similar labour market performances and economic structures have broadly similar levels of

potential automation. Four broad country groups emerge: a) Industrial economies with relatively inflexible

labour markets, which could see the highest automation rates; b) Services-dominated economies such as the

US and the UK with long tail of lower skilled workers and intermediate levels of potential automation; c)

Nordic countries with high employment rates and skill levels and relatively low levels of potential

automation; and d) East Asian nations with high levels of technological advancement and education, which

could see high short term automation rates in some sectors but lower longer term impacts.

Industry structure is important as Eastern European countries, for example, tend to have relatively high

shares of employment in sectors such as manufacturing and transport that are projected to be relatively

easy to automate looking ahead to the 2030s.

Automation rates also differ across countries because ways of working differ. In particular, workers in

countries such as Singapore and South Korea with more stringent educational requirements have greater

protection against automation in the long run. This is also true (particularly in Europe) for countries with

higher levels of education spending as a percentage of GDP.

Country automation levels will evolve over time – jobs in more technologically advanced nations like Japan

and South Korea may be at immediate risk as computational tasks are automated in the first algorithmic

wave. But workers in these nations could eventually face lower risks in the later waves of automation that

displace manual jobs and could have a greater impact on workers in other countries with lower average skill

levels and/or large manufacturing bases.

3.1. Estimated potential automation rates across countries

The methodology for estimating potential future automation rates that we previously developed

17

was refined

and applied across the set of 29 countries for which OECD PIAAC data are publicly available (27 from the OECD

plus Singapore and Russia). This revealed a range of estimates across countries for the share of existing jobs

with potential high rates of automation by the 2030s, as shown in Figure 3.1. Notably some Eastern European

countries such as Slovakia (44%) and Slovenia (42%) face relatively high potential automation rates, whilst

Nordic countries such as Finland (22%) and Asian countries such as South Korea (22%) have relatively lower

shares of existing jobs that are potentially automatable.

17

PwC (2017), UK Economic Outlook: Will robots steal our jobs? Available here: https://www.pwc.co.uk/economic-

services/ukeo/pwcukeo-section-4-automation-march-2017-v2.pdf.

3. How do potential automation rates

vary by country?

Will robots really steal our jobs?

An international analysis of the potential long term impact of automation PwC 10

Figure 3.1 – Potential rates of job automation by country

Source: PIAAC data, PwC analysis

3.2. The relative impact of industry composition and

job automatability

The overall automation rate estimates in Figure 3.1 reflect two key factors:

1. The share of employment in each country across industry sectors; and

2. The relative automatability of jobs in each country on a sector by sector basis.

As a result of differences in labour market structures, education and skills levels, and government polices across

the countries, the relative impact of these two components varies between countries (see Figure 3.2), which

gives rise to differences in estimated automation levels. Looking at Figure 3.2, we can distinguish four broad

country groups:

Industrial economies – for example, Germany, Slovakia and Italy, which could see relatively higher

automation rates in the long run. These countries are typically characterised by jobs that are relatively more

automatable and (relative to the OECD average) more concentrated in industry sectors with higher potential

automation rates (as discussed further in Section 4 below).

Services-dominated economies – for example, the US, UK, France and the Netherlands, which have jobs

that are on average relatively more automatable based on their characteristics, but also a greater concentration

on services sectors that tend to be less automatable on average than industrial sectors.

0% 10% 20% 30% 40% 50%

svk

svn

ltu

cze

ita

usa

fra

deu

aut

esp

pol

tur

irl

nld

gbr

cyp

bel

dnk

isr

chl

sgp

nor

swe

nzl

jpn

rus

grc

fin

kor

Country

Potential jobs at high risk of automation

Will robots really steal our jobs?

An international analysis of the potential long term impact of automation PwC 11

Asian countries – for example, Japan, South Korea, Singapore and Russia, which have jobs that are relatively

less automatable overall but with relatively high concentrations of employment in industrial sectors with

relatively high potential automation rates.

Nordic countries – for example Finland, Sweden and Norway (in addition to New Zealand and Greece

outside this region). These countries have jobs that are on average relatively less automatable and in industry

sectors with relatively lower potential automation rates.

Figure 3.2 – Potential impact across countries by employment shares and automatability of jobs

Source: PIAAC data, PwC analysis

There are also some relationships here between estimated automation risks in different countries and their

performances on PwC’s labour market indices – the Young Workers Index (YWI)

18

, the Women in Work Index

(WWI)

19

and the Golden Age Index (GAI) for older workers

20

. European countries such as Slovakia, Slovenia,

Czech Republic and Italy have repeatedly appeared towards the bottom or lower middle of the rankings on all of

these labour market indices. This indicates relatively higher NEET (not in education, employment or training)

rates for younger people and lower engagement of women and older people in the workforce. Similarly, New

Zealand and Israel, along with the Nordic countries, have been high performers on all of our indices due to

relatively high employment rates and education and skill levels across all major demographic groups.

3.3. Factors related to estimated automation levels

Countries that have an increased concentration of labour in more industrial sectors, rather than in the service

sectors, tend to have higher potential automation rates (other things being equal). For example, countries with

a higher share of employment in the manufacturing sector such as Czech Republic (29%) and Slovenia (28%)

are estimated to have an increased potential job automation rate, see Figure 3.3. These jobs are characterised by

a greater proportion of manual or routine work that is typically more susceptible to automation (as discussed

further in Section 4 below).

18

PwC (2017), Young Workers Index: The $1.2 trillion prize from empowering young workers in an age of automation. Available here:

https://www.pwc.co.uk/services/economics-policy/insights/young-workers-index.html.

19

PwC (2017), Women in Work Index: Closing the gender pay gap. Available here: https://www.pwc.co.uk/services/economics-

policy/insights/women-in-work-index.html.

20

PwC (2017), Golden Age Index: The potential $2 trillion prize from longer working lives. Available here:

https://www.pwc.co.uk/services/economics-policy/insights/golden-age-index.html.

svk

svn

ltu

cze

ita

usa

fra

deu

aut

esp

pol

tur

irl

nld

gbr

cyp

bel

dnk

isr

chl

sgp

nor

swe

nzl

jpn

rus

grc

fin

kor

0

1

2

3

4

5

6

7

8

9

10

0 1 2 3 4 5 6 7 8 9 10

Relative impact from the automatability

of jobs (0

-10 index)

Relative impact from employment shares across industries (0-10 index)

Will robots really steal our jobs?

An international analysis of the potential long term impact of automation PwC 12

Figure 3.3 – Relative impact from employment shares across industries e.g. manufacturing

Source: PIAAC data, PwC analysis

The relative impact from the automatability of jobs is instead dependent on a wider range of determinants,

such as the level of training, education, and skills required for those jobs. For example, countries with a

higher proportion of labour employed in jobs with a high level of educational requirements, such as

Singapore (60%) and Russia (57%), are estimated to have lower potential automation rates (see Figure 3.4).

Notably, this is a stronger effect than the proportion of labour with high education levels alone (e.g. degree-

level, correlation (r) = -0.35 vs. r = -0.55 for high educational job requirements).

Figure 3.4 – Relative impact from the automatability of jobs e.g. educational job requirements

Source: UNDP HDI data, PwC analysis

0%

10%

20%

30%

40%

50%

0% 5% 10% 15% 20% 25% 30%

Potential jobs at high risk of automation

Manufacturing employment share

ρ = 0.536

0%

10%

20%

30%

40%

50%

0% 10% 20% 30% 40% 50% 60% 70%

Potential jobs at high risk of automation

High educational job requirements

ρ = (0.554)

Will robots really steal our jobs?

An international analysis of the potential long term impact of automation PwC 13

Furthermore, for European countries there are strong negative correlations between the potential share of

existing jobs at high risk of automation and country education metrics, such as government expenditure on

education as a percentage of GDP (r=-0.77) and pupil-t0-teacher ratios in primary school (r=0.53)

21

. This

relationship is not so strong for Asian countries that have proportionally lower education spend and higher

pupil-to-teacher ratios than in Europe. However, these Asian countries nonetheless achieve high educational

outcomes, notably for STEM subjects, so the underlying negative relationship between high education and low

automatability also holds here even if different metrics need to be used to show this relationship in Asia.

In addition to the share of employment and automatability of jobs, one other factor that may impact Asian

countries more is the current technological level and the extent to which job automation has already taken

place, which is also an important factor in future automation rates. Figure 3.5 shows a negative correlation

between the potential jobs at high risk of automation, adjusted to account for industry composition, against the

density of industrial robots in the country

22

. This suggests that workforces in more technologically advanced

countries such as Japan, South Korea and Singapore that are increasingly working alongside robots have

already adjusted to automation to some degree and so may be at lower future risk. Instead they may be well

placed to reap the benefits of automation in terms of higher productivity and real wages.

Figure 3.5 – Relationship between density of industrial robots and industry-adjusted job automation rates

Source: International Federation of Robots, PwC analysis

21

Data sourced from the United Nations Development Programme. Government expenditure on education (% of GDP 2010-2014);

Pupil-to-teacher ratio (2010-2014).

22

International Federation of Robotics – https://ifr.org/ifr-press-releases/news/world-robotics-report-2016.

svk

svn

cze

ita

usa

fra

deu

aut

esp

nld

gbr

bel

dnk

sgp

swe

jpn

fin

kor

0%

10%

20%

30%

40%

50%

1.7 1.9 2.1 2.3 2.5 2.7 2.9

Industry

-adjusted job automation risk

log (industrial robots per 10,000 employees in the manufacturing industry)

ρ = (0.596)

Will robots really steal our jobs?

An international analysis of the potential long term impact of automation PwC 14

3.4. Impact on countries over time – the three waves of automation

The impact of the automation process is expected to vary over-time as automation encroaches on increasingly

human-like capabilities, as illustrated in Figure 3.6 for the four country groups we discussed earlier in this

section. On average across the 29 countries covered, the share of jobs at potential high risk of automation is

estimated to be around 3% by the early 2020s, but this rises to around 20% by the late 2020s, and around 30%

by the mid-2030s. The precise timings shown in Figure 3.6 (and subsequent charts of this kind in the report)

are subject to many uncertainties, but give some indication of how automation might have its effect on different

groups of countries over time.

Figure 3.6 – Potential impact of job automation over-time across the four country groups

Source: PIAAC data, PwC analysis

As mentioned in the introduction, this automation process can be characterised as involving three overlapping

waves, which we refer to as: 1) an Algorithm wave, 2) an Augmentation wave, and 3) and Autonomy wave.

Algorithm wave – The first wave of automation, which is already well underway, is primarily an automation

of simple computational tasks and analysis of structured data (see Figure 3.7). This includes manually

conducting mathematical calculations, or using basic software packages and internet searches. Increasingly

sophisticated applications for processing big data and running machine learning algorithms are available to the

market and being commoditised. However, it is these more fundamental computational job tasks that will be

most impacted first.

Augmentation wave – The second wave of automation is expected to involve a more dynamic change to how

many job tasks are conducted, in particular those that are routine and repeatable. For example, routine tasks

such as filling in forms or exchanging information, which includes the physical transfer of information, will

increasingly be augmented by technology. It is also likely to see a decreased need for many programming

languages as repeatable programmable tasks are increasingly automated, and through machines themselves

building and redesigning learning algorithms. This will also involve further advances in robotics, although

generally these will not be fully autonomous during this period but will operate with the assistance of human

workers and augment their capabilities. The impacts of this second wave are expected to emerge on an

economy-wide scale during the course of the 2020s.

Autonomy wave – The third wave of automation is one of autonomous AI and robotics that will further

automate routine tasks but also those tasks that involve physical labour or manual dexterity. Problem solving

will increasingly extend from analytical modelling of structured data to problem solving in dynamic real-world

situations that also requires responsive actions to be taken. This will include the simulation of adaptive

behaviour by autonomous agents, such as in factories or in transport. The full impacts of this third wave are

only expected to emerge on an economy-wide scale in the 2030s, even though some of these technologies are

already being piloted now.

0%

10%

20%

30%

40%

50%

2019 2021 2023 2025 2027 2029 2031 2033 2035 2037

Potential jobs at

high risk of automation

Industrial Service Nordic Asian

Will robots really steal our jobs?

An international analysis of the potential long term impact of automation PwC 15

Figure 3.7 – Task automation across the three waves

Source: PIAAC data, PwC analysis

As these three waves play out, different regions of the world are expected to see relatively greater impacts at

different points in time, as illustrated in Figure 3.8. For example, a greater impact is expected in Asian

countries at first as the Algorithm wave predominates. However, both industrial and services-dominated

economies are then expected to face greater impacts in the longer term as the Augmentation and Autonomy

waves ripple through economies.

Figure 3.8 – The rank order of potential impact over-time across the four country groups

Source: PIAAC data, PwC analysis

0% 5% 10% 15% 20% 25% 30% 35% 40% 45%

Manual tasks

Routine tasks

Computation

Management

Social skills

Literacy skills

Proportion of tasks from high risk jobs

Algorithm wave Augmentation wave Automony wave

1

2

3

4

2019 2021 2023 2025 2027 2029 2031 2033 2035 2037

Rank order of potential

impact of job automation

Industrial Service Nordic Asian

Will robots really steal our jobs?

An international analysis of the potential long term impact of automation PwC 16

In Table 3.1 below we set out estimates of how the proportion of jobs at risk of automation in different

countries might evolve over the three waves.

Table 3.1 – Estimated share of jobs at potential high risk of automation across countries for each of the

three waves: Algorithm wave, Augmentation wave and Autonomy wave

Country

Algorithm wave (%)

Augmentation wave (%)

Autonomy wave (%)

Slovakia

4

25

44

Slovenia

3

24

42

Lithuania

4

26

42

Czech Republic

3

25

40

Italy

4

23

39

USA

5

26

38

France

4

22

37

Germany

3

23

37

Austria

3

22

34

Spain

3

21

34

Poland

2

18

33

Turkey

1

14

33

Ireland

2

19

31

Netherlands

4

21

31

UK

2

20

30

Cyprus

2

19

30

Belgium

4

18

30

Denmark

3

19

30

Israel

3

19

29

Chile

1

13

27

Singapore

4

18

26

Norway

3

18

25

Sweden

3

17

25

New Zealand

2

16

24

Japan

4

16

24

Russia

2

12

23

Greece

2

13

23

Finland

2

16

22

South Korea

2

12

22

Note: figures shown are cumulative so those in the final column include the estimated impacts from all three waves of automation.

Source: PIAAC data, PwC analysis

Will robots really steal our jobs?

An international analysis of the potential long term impact of automation PwC 17

3.5. Two important caveats – constraints on automation and new

job creation

When considering these and other results in this report, however, it is important to bear in mind, first, that

there could be a variety of economic, legal and regulatory and organisational constraints that mean that

automation does not proceed as fast as projected here. We discuss these constraints further in Section 8 below.

Second, we also believe that new technologies like AI and robotics will create many new jobs. Some of these

new jobs will relate directly to these new technologies, but most will just result from the general boost to

productivity, incomes and wealth that these technologies will bring. As these additional incomes are spent, this

will generate additional demand for labour and so new jobs, as such technologies have done throughout history.

Our other research

23

suggests that the net long term effect on employment in advanced economies like the US

and the EU may be broadly neutral, although it is harder to quantify new job creation than it is to estimate the

proportion of existing jobs at risk of automation (precisely because those jobs exist now and we therefore know

a lot about their characteristics). We can, however, gain some more insight into potential areas of job losses and

gains by considering how automatability varies by industry sector, which is the subject of the next section of

this report.

23

PwC (2018), The macroeconomic impact of artificial intelligence

Will robots really steal our jobs?

An international analysis of the potential long term impact of automation PwC 18

Key findings

Potential automation risk varies widely across industry sectors. Transportation and storage and

manufacturing are estimated to have the highest share of existing jobs that could potentially be automated

by the 2030s at around 52% and 45% respectively. Human health and education are the major sectors with

the lowest estimated future automation rates, and corresponding potential for net job gains in the long run.

Industries are likely to follow different paths of automation over time – data-driven industries such as

financial services and information management will be most affected in the short term as algorithmic

technologies are developed. In the longer run, the advent of driverless vehicles and other types of

autonomous machines will impact sectors such as transport and construction.

An industry’s task composition and educational requirements are the primary drivers behind its

automatability. Industries where large number of workers are engaged in relatively routine tasks are likely

to see more automation. Less automatable sectors have a greater proportion of time spent on social and

literacy-based tasks, and also have higher average educational requirements.

4.1. Total automation rates across industries

The estimated share of existing jobs with potential high rates of automation varies widely across industry

sectors, from a median across countries of 52% for transportation and storage to just 8% for the education

sector (see Figure 4.1 – error bars in this and other similar charts in this report show the variation across

countries in our estimates of potential automation rates by industry).

However, in terms of absolute numbers of jobs that could be automated, the greatest impact might be felt in the

manufacturing sector (with an estimated automatability of 45%) as this has a median employment share across

countries of 14%, as compared to only 5% in transport and storage. The wholesale and retail trade sector has a

moderately high automatability estimate at 34% (with a median employment share of 14%), whilst health and

social work has relatively lower potential automatability at 21% (with a median employment share of 11%).

Figure 4.1 –Share of jobs with potential high automation rates by industry

Source: PIAAC data, PwC analysis

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Transportation and storage

Manufacturing

Construction

Administrative and support service

Wholesale and retail trade

Public administration and defence

Financial and insurance

Information and communication

Professional, scientific and technical

Accommodation and food service

Human health and social work

Education

Potential jobs at high risk of automation

4. Which industry sectors could see

the highest rates of automation?

Will robots really steal our jobs?

An international analysis of the potential long term impact of automation PwC 19

The fact that automatability in a given industry sector varies across countries is illustrated by the more detailed

figures in Table 4.1 for five of the largest sectors by employment.

Table 4.1. Share of jobs with potential high automation rates for the top 5 industries by employment share,

across countries.

Country

Manufacturing

(%)

Wholesale and

retail trade

(%)

Human health

and social work

(%)

Education

(%)

Construction

(%)

Slovakia

58

43

34

14

42

Slovenia

57

35

31

13

53

Lithuania

55

39

27

26

58

Czech Republic

55

33

38

10

36

Italy

55

35

29

17

44

USA

53

51

28

12

34

France

53

41

29

17

41

Germany

49

43

24

9

39

Austria

48

37

26

9

51

Spain

45

35

26

8

42

Poland

50

31

21

9

48

Turkey

45

26

36

8

40

Ireland

50

39

17

7

33

Netherlands

46

35

24

8

36

UK

45

42

18

8

23

Cyprus

38

35

14

6

42

Belgium

45

28

19

10

43

Denmark

46

33

17

9

44

Israel

42

34

14

8

42

Chile

32

27

23

13

29

Singapore

33

38

19

9

26

Norway

33

34

16

6

35

Sweden

45

26

22

4

28

New Zealand

36

32

16

6

23

Japan

32

27

10

6

29

Russia

33

21

8

5

45

Greece

35

23

20

3

25

Finland

41

22

9

4

35

South Korea

31

24

12

6

31

Employment

share (median)

14.4

13.7

10.7

8.7

7.6

Source: PIAAC data, PwC analysis

As the colour coding in the table shows, there are some clear common patterns across countries between those

with high automatability (red colour) and low automatability (green colour), but also some differences between

countries within sectors.

Will robots really steal our jobs?

An international analysis of the potential long term impact of automation PwC 20

4.2. Impact on industries over time

The automation process is also expected to affect industries differently over time, as shown in Figure 4.2.

For example, the financial and insurance sector has the highest share of existing jobs at potential high risk of

automation in the Algorithm wave at 8%, but then peaks at just over 30% in the early 2030s as we move into

the Autonomy wave. In contrast, the transport and storage and manufacturing sectors have lower potential

automation rates in the Algorithm wave, but this picks up to higher levels by the time of the Autonomy wave in

the 2030s (by which time use of driverless vehicles is likely to become more widespread across the economy).

Figure 4.2 – Potential impact of job automation over time across industry sectors

Source: PIAAC data, PwC analysis

0%

10%

20%

30%

40%

50%

60%

2019 2021 2023 2025 2027 2029 2031 2033 2035 2037

Potential jobs at

high risk of automation

Transportation and storage Manufacturing

Wholesale and retail trade Financial and insurance

Human health and social work Education

Will robots really steal our jobs?

An international analysis of the potential long term impact of automation PwC 21

4.3. Drivers of differences between industries

One of the main drivers of a sector being potentially more automatable is the composition of tasks involved

in jobs in that sector. Workers in sectors such as manufacturing and transport and storage spend a larger

proportion of their time engaged in manual tasks and in conducting simple administrative and routine tasks,

as shown in the left hand pane of Figure 4.3 for manufacturing. In the long term these tasks are most likely to

be automated by machines that are increasingly able to replace human labour, and carry out tasks at much

higher speed and levels of accuracy and efficiency.

Figure 4.3 – Task composition for manufacturing, financial and insurance, and education sectors.

Manufacturing

Financial and insurance

Education

Compared to average

Compared to average

Compared to average

Source: PIAAC data, PwC analysis

However, as noted above, industries follow different paths of automation over time, and data-driven industries

such as the financial and insurance sector (and others such as the ‘information and communication’ and the

‘professional, scientific and technical’ sectors) may be most automatable in the short term. Workers in these

sectors typically spend a disproportionately larger amount of their time engaged in simple computational

tasks (see middle panel of Figure 4.3 for finance/insurance).

In contrast, relatively low automatability sectors such as human health and social work, and education (see

right hand panel in Figure 4.3) have more focus on social skills, empathy and creativity, which are more difficult

to directly replace by a machine even allowing for potential technological advances over the next 10-20 years.

20%

31%

12%

22%

12%

2%

6%

28%

20%

26%

16%

4%

10%

26%

12%

23%

21%

7%

124%

108%

101%

88%

86%

63%

0% 100% 200%

Manual tasks

Routine tasks

Computation

Management

Social skills

Literacy skills

34%

98%

163%

103%

114%

119%

0% 100% 200%

Manual tasks

Routine tasks

Computation

Management

Social skills

Literacy skills

64%

90%

102%

92%

148%

0% 100% 200%

Manual tasks

Routine tasks

Computation

Management

Social skills

Literacy skills

202%

Will robots really steal our jobs?

An international analysis of the potential long term impact of automation PwC 22

4.4. Which sectors are likely to see the largest jobs gains?

We mentioned above that our previous research suggests that, at the macroeconomic level, the job losses from

automation are likely to be broadly offset by job gains arising from new technologies like AI and robotics. This

will include some totally new jobs in areas relating specifically to these technologies, which will be relatively

highly skilled and highly paid, but probably relatively small in number based on past experience

24

.

However, the largest job gains will be in sectors where these new technologies boost demand, either directly or

indirectly, through increasing income and wealth. As these additional incomes are spent on goods and services,

so this will generate increased demand for labour. It is difficult to put precise numbers on what kind of jobs

these will be, but we would anticipate them being concentrated in non-tradable service sectors such as health

and education that a richer, and older, society is likely to demand more of, and which are less readily

automatable according to our analysis. In the case of education, the increased demand with an ageing

population and rapid technological change may not be from the young but rather from older people wanting

to retrain for new careers later in life, or just to study for personal fulfilment in retirement. While some of this

could be delivered digitally, there is still likely to be strong demand for human teachers, coaches and mentors to

help guide people through this process (whether in person or online). As average incomes grow, there will also

be increased demand for a range of other jobs providing personal services (e.g. cleaning, household chores and

repairs, personal trainers and shoppers, and the digital platforms providing these services).

In addition, the government should benefit from increased tax revenues from the higher incomes and profits

that these new technologies will generate. These additional tax revenues could fund higher public spending on

health and education to support additional jobs in these areas, but could also be directed into increased

investment in infrastructure, which would both support the supply side of the economy and create new jobs in

construction and related sectors. While construction may well be more automatable than health or education by

the 2030s, we would still expect there to do be considerable human employment in this sector on supervisory

jobs and those that require multi-tasking and flexibility rather following set routines.

The public policy implications are discussed further in Section 7 below. Before that, however, we look in the

next section at how different occupations may be affected by automation.

24

As discussed, for example, in Frey and Hawksworth (PwC, 2015)

Will robots really steal our jobs?

An international analysis of the potential long term impact of automation PwC 23

Key findings

Potential automation rates vary widely by occupation – machine operators and assemblers could face a risk

of over 60% by the 2030s, while professionals, senior officials and senior managers may face only around a

10% risk of automation. These variations stem from the different kinds of tasks performed in different

occupations and their varied educational requirements.

Workers in different occupations are likely to be impacted differently over time – technicians and clerical

workers could be most heavily affected in the algorithmic and augmentation waves where machines

overtake humans in firstly simple computational tasks and eventually routine, information processing tasks.

However, in the longer run, machine operators and assemblers may be the most exposed to automation.

Occupations typically vary more in their automatability than industries, which reflects the fact that they are

typically more concentrated in their task composition than industries. However, a given occupation could

see different automation rates in different industries and countries depending on factors such as the

average education level of workers, and the practices of labour division and specialisation from country to

country.

5.1. Total automation risk across occupation categories

In addition to the overall impact on industries, potential rates of automation also vary across occupational

categories. For example, our estimates suggest a median long run automation rate of up to around 64% for

machine operators and assemblers, as compared to a median rate of just 6% for senior officials and senior

managers (see Figure 5.1). Machine operators and assemblers are most over-represented in the transportation

and storage sector, accounting for on average 43% of the employment in that sector, followed by 20% for the

manufacturing sector.

Figure 5.1 – Share of jobs with potential high rates of automation by industry

Source: PIAAC data, PwC analysis

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

8. Machine operators and assemblers

4. Clerical workers

9. Elementary occupations

7. Craft and related trades workers

3. Technicians and associate professionals

5. Service and sales workers

6. Skilled agricultural and fishery workers

2. Professionals

1. Senior officials and managers

Potential jobs at high risk of automation

5. Which occupations could see the

highest rates of automation?

Will robots really steal our jobs?

An international analysis of the potential long term impact of automation PwC 24

5.2. Impact over time by occupation

The impact of the automation process shows notable differences between occupations over time (see Figure

5.2). In particular, clerical workers are estimated to face the highest potential impacts in the short to medium

term. This includes: general and keyboard clerks, customer services clerks, numerical and material recording

clerks, and other clerical support workers. The proportion of these clerical jobs at potential high risk of

automation is estimated at 10% in the Algorithm wave, rising sharply to 49% in the Augmentation wave of the

2020s (but with only a slight further rise to 54% in the Autonomy wave of the 2030s, which would hit other

occupations such as machine operators and assemblers more).

Figure 5.2 – Potential impact of job automation over time across occupational categories

Source: PIAAC data, PwC analysis

0%

10%

20%

30%

40%

50%

60%

70%

2019 2021 2023 2025 2027 2029 2031 2033 2035 2037

Potential jobs at

high risk of automation

Managers and professionals Technicians and associate professionals

Clerical workers Service and sales workers

Craft and related trades workers Machine operators and assemblers

Will robots really steal our jobs?

An international analysis of the potential long term impact of automation PwC 25

5.3. Drivers of differences between occupations

The estimated differences in potential automation rates across occupational categories is much greater than

across industries. For example, machine operators and assemblers have a long run estimated automation rate

that is over 10 percentage points greater than the most automatable industry during the Autonomy wave (which

is the transportation and storage sector). For these workers, the tasks conducted are primarily manual and

routine tasks, which account for approximately two-thirds of their working activity (see left hand panel in

Figure 5.3). This concentration of labour into this particular set of tasks makes their work more automatable.

Figure 5.3 – Task composition for machine operators and assemblers, clerical workers and professionals

Machine operators and assemblers

Clerical workers

Professionals

Compared to average

Compared to average

Compared to average

Source: PIAAC data, PwC analysis

Clerical workers, likewise, could face much higher automation rates in the Algorithm and Augmentation waves

than the most automatable industry in that period (the financial and insurance sector). These clerical workers

inherently undertake work that is most characteristic of the Augmentation wave – routine processes, simpler

computational tasks and exchanging information.

Professionals, as well as senior officials and senior managers, are estimated to be at the lowest risk of

automation throughout the three waves. They are more likely to be engaged in social skills, literacy skills and

more complex computational tasks that are less automatable (see right hand panel in Figure 5.3). They also

tend to be relatively highly educated and this will help them to adapt to new waves of technology so as to remain

complementary to machines, rather than being replaced by them. The nature of their work may change

significantly over time (as it did previously with the advent of personal computers and later the internet),

but they are less likely to find themselves displaced entirely by autonomous machines than a driver, factory

worker or clerk.

28%

35%

6%

21%

8%

2%

12%

33%

15%

25%

12%

3%

8%

27%

17%

23%

19%

7%

168%

124%

51%

84%

58%

45%

0% 100% 200%

Manual tasks

Routine tasks

Computation

Management

Social skills

Literacy skills

75%

114%

128%

99%

84%

79%

0% 100% 200%

Manual tasks

Routine tasks

Computation

Management

Social skills

Literacy skills

48%

93%

142%

92%

128%

189%

0% 100% 200%

Manual tasks

Routine tasks

Computation

Management

Social skills

Literacy skills

Will robots really steal our jobs?

An international analysis of the potential long term impact of automation PwC 26

5.4. Composition of industries by occupational category

The share of employment across occupations varies between industry sectors, which accounts for some of the variation in

the overall estimated rate of automation by sector. For example, machine operators and assemblers typically account for

around 20% of occupations in the manufacturing sector, but are negligible in both the financial and insurance and

education sectors (see Figure 5.4). Instead, the financial and insurance sector is over-represented in clerical workers (25%)

and associate professionals (26%), whereas education sector staff are primarily teaching professionals (70%).

Figure 5.4 – Employment share across occupations

Source: PIAAC data, PwC analysis

However, not all occupations are the same across different industry sectors. For example, professionals and associate

professionals are not only over-represented in the health and social work sector (31% and 24%) compared to the wholesale

and retail trade sector (5% and 10%), but also have a significantly lower estimated risk of automation (Figure 5.5). In

contrast, service and sales workers are over-represented in the wholesale and retail trade sector relative to the health sector

(46% vs. 27%), but face a roughly equivalent risk of automation in the two sectors.

Figure 5.5 – Potential impact of job automation by occupation: Human health and social work vs.

wholesale and retail trade

Source: PIAAC data, PwC analysis

These sectoral and occupational variations are driven by differences in ways of working such as the educational

requirements of jobs and the characteristics of the workers employed. In the next section, we look in more detail at how

different types of workers may be affected by automation.

0% 10% 20% 30% 40% 50% 60% 70% 80%

9. Elementary occupations

8. Machine operators and assemblers

7. Craft and related trades workers

6. Skilled agricultural and fishery workers

5. Service and sales workers

4. Clerical workers

3. Technicians and associate professionals

2. Professionals

1. Senior officials and managers

Employment share

Manufacturing Financial and insurance Education

1. Senior officials and

managers

2. Professionals

3. Technicians and

associate

professionals

4. Clerical workers

5. Service and sales

workers

8. Machine operators

and assemblers

9. Elementary

occupations

(30)%

(20)%

(10)%

0%

10%

20%

30%

(30)% (20)% (10)% 0% 10% 20% 30%

Increased automation risk in

human health and social work

Increased employment share in human health and social work

Will robots really steal our jobs?

An international analysis of the potential long term impact of automation PwC 27

Key findings

Potential automation risk varies significantly across different types of workers. Males may face a