Asat26April2009theGroupoperatedoutof359

storesintheUnitedKingdom(excludingNorthern

Ireland).ThemajorityofstorestradeundertheSports

Direct.comfascia.TheGrouphasacquiredanumber

ofretailbusinessesoverthepastfewyears,andsome

storesstilltradeundertheLillywhites,McGurks,

Exsports,GilesportsandHargreavesfascias.Field&

Trekstorestradeundertheirownfascia.

TheGroup’sUKstores(otherthanField&Trek)

supplyawiderangeofcompetitivelypricedsportsand

leisureequipment,clothing,footwearandaccessories,

underamixofGroupownedbrands,suchasDunlop,

SlazengerandLonsdale,licensedinbrandssuchas

Umbro,andwellknownthirdpartybrandsincluding

adidas,Nike,ReebokandPuma.Asignicant

proportionoftherevenueinthestoresisderivedfrom

thesaleoftheGroupownedandlicensedinbranded

products,whichallowstheretailbusinesstogenerate

highermargins,whilstatthesametimedifferentiating

theGroup’sstoresfromitscompetitors,bothinterms

oftherangeofproductsonsaleandthecompetitive

pricesatwhichtheyareoffered.

Field&Trekoperatesoutof16storesintheUK,

sellingawiderangeofcampingandoutdoor

equipment,waterproofclothingandfootwear,

includingleadingbrandssuchasBerghaus,Merrell

andSalomon.TheacquisitionofField&Trekgave

theGroupanentryintotheoutdoormarket,which

hadbeenidentiedasastrategicopportunityforthe

Group,andthathasbeenstrengthenedfollowingthe

acquisitionofUniversalCyclesbytheintroductionofa

rangeofcycleproductsinbothstoresandonline.

TheGrouphasretailinterestsoutsidetheUKand

hasaexibleapproachtoentryintomarkets.These

interestsincludewhollyownedretailoutlets(in

Belgium,Holland,LuxemburgandSlovenia),joint

ventureswithotherretailers(suchasinNorthern

IrelandandtheRepublicofIreland)storeswithin

anotherretailer’sstore(asinCyprus)andlicence

agreementsasinSouthAfricaandtheMiddleEast.

TheGroup’sportfolioofsportsandleisurebrands

includesDunlop,Slazenger,Kangol,Karrimor,

Lonsdale,EverlastandAntigua.Aspreviously

mentionedtheGroup’sRetaildivisionsellsproducts

undertheseGroupbrandsinitsstores,andtheBrands

divisionexploitsthebrandsthroughitswholesaleand

licensingbusinesses.

TheBrandsdivisionwholesalebusinesssellsthe

brands’coreproducts,suchasDunloptennisrackets

andSlazengertennisballs,towholesalecustomers

throughouttheworld,obtainingfarwiderdistribution

fortheseproductsthanwouldbethecaseiftheir

salewasrestrictedtoGroupstores.Thewholesale

businessalsowholesaleschildrenswearandother

clothing.Thelicensingbusinesslicensesthird

partiestoapplyGroupownedbrandstonon-core

productsmanufacturedanddistributedbythosethird

parties,andthirdpartiesarecurrentlylicensedin

differentproductareasinover100countries.The

Brandsdivisioniscloselyinvolvedinthedevelopment

oflicensedproductsandmonitorslicenseesand

theirmanufacturerstoensureproductqualityand

presentationandconsistencywiththeappropriate

brandstrategy.

TheBrandsdivisioncontinuetosponsoravariety

ofprestigiouseventsandretainabaseofglobally

recognisedtalentedsportsmenandwomen.The

ofcialtennisballsupplieragreementswithThe

WimbledonChampionshipsandRoland-Garrosarethe

foremostoftheseagreements.Dunlop’sprofessional

tennistourteamcontinuestogrowwithJamesBlake

beingtheGroup’shighestrankedplayer.Cricketers

PaulCollingwoodandMattPrioraresponsoredby

SlazengerwhilstLeeWestwoodandDarrenClarke

continuetowearDunlopapparelinmajorgolf

tournamentsacrosstheworld.Othersportssuchas

badmintonandsquashalsoprovideopportunitiesof

interestforCarltonandDunloprespectively.

Sports Direct is the UK’s leading sports retailer by revenue and operating profit, and the

owner of a significant number of internationally recognised sports and leisure brands.

Financial Highlights

• Grouprevenueup8.6%to£1,367m(2008:£1,260m)

• UnderlyingEBITDAdown8.9%to£136.8m(2008:£150.2m)

• Underlyingprotbeforetaxdown20.1%to£68.2m(2008:£85.4m)

Reportedprotbeforetaxdown91%to£10.7m(2008:£118.9m)aftercurrency

exchangeandnon-cashadjustments

• Underlyingearningspersharedown7.5%to7.93p(2008:8.57p)

• Groupgrossmargindecreasedby280basispointsto40.8%(2008:43.6%)

UKretailgrossmarginsdownto42.5%(2008:45.7%)atoncurrencyneutral

basis

• Netdebtatyearend£431.3m

Operatingcomfortablywithinbankingcovenants

Targettoreducedebtbelow£400minthe2009/10nancialyear

• UKRetaillike-for-likegrosscontribution:+2.5%

• TheBoarddecidednottorecommendanaldividend

Operational highlights

• UKRetailclearmarketleader

Salesexceeded£1bn

Consolidatingpositionthroughincreasingproductrangeandavailability,

controllingcosts,improvingsourcing,supplychainefcienciesand

strengtheningthirdpartybrandrelationships

• Successfullyexpandedinternationalretail

Openedsevennewstores

• Brandsdivisiongoodprogress

Growthinbrandslicensing–41newlicencessignedduringtheyear

FurtherconsolidationofBrandsdivisionmanagementinShirebrook

2

3

9

13

14

18

22

27

28

31

73

CONTENTS

CHAIRMAN’S STATEMENT

CHIEF EXECUTIVE’S REPORT AND BUSINESS REVIEW

FINANCIAL REVIEW

BOARD OF DIRECTORS

DIRECTORS’ REPORT

CORPORATE GOVERNANCE REPORT

DIRECTORS’ REMUNERATION REPORT

DIRECTORS’ RESPONSIBILITIES

CORPORATE AND SOCIAL RESPONSIBILITY REPORT

FINANCIAL STATEMENTS

SHAREHOLDER INFORMATION

In a very challenging market environment, the Group’s relentless focus on the

basics of retailing has resulted in the delivery of what are very creditable, solid

results. We grew sales in both Retail and Brands divisions, and while we have

seen a decline in gross margin and a corresponding drop in underlying EBITDA,

that was caused almost entirely by the fall in the value of the pound.

We maintained our position as the UK’s leading sports retailer by continuing

to implement our back to basics strategy – offering the most comprehensive

product range, ensuring stock availability, closely controlling costs and

making efficiencies where possible. During the year the Group developed its

relationships further with our third party brand suppliers, many who have

offices within our head office at Shirebrook.

We improved stock control and sourcing within International Retail. We were

very pleased with the Group’s ability to sign an agreement, produce the goods

and roll out branded areas in 121 stores in China within a four month period

from start to finish.

During the year we opened 27 stores in the UK (excluding Northern Ireland),

nine stores in the Republic of Ireland and Northern Ireland through Heatons,

and seven stores in Europe; including our first stores in Cyprus.

The Group continued to consolidate the Brands division management at

Shirebrook. Licensing remains the key driver of growth within the division, and

we signed 41 new licence deals during the year.

The Board has decided not to recommend the payment of a final dividend this

year as we believe reducing debt should be our priority. We will continue to keep

this under review.

OUR STRATEGY FOR GROWTH

We have established an excellent platform for growth, which we will build on

with our proposed EBITDA related share bonus scheme, of which there are

more details on page 24.

Our priorities going forward are to:

• Continue to strengthen our position in our core UK market

• Continue to develop our international store portfolio

• Maintain our brand market leading positions

• Reduce debt with a target of achieving below £400m in the 2009-10

financial year

Finally I wish to pay tribute to the hard work of all our people, from my

colleagues on the Board to our people in the stores, and thank them for all their

endeavours.

Simon Bentley

Acting Non-Executive Chairman

16 July 2009

Simon Bentley

Acting Non-Executive Chairman

CHAIRMAN’S STATEMENT

2

Chairman’s Statement

Sports Direct International PLC Annual Report 2009 3

Dave Forsey

Chief Executive

OVERVIEW OF FINANCIAL PERFORMANCE

In the 52 weeks ended 26 April 2009 (the Year), Group revenue was up 8.6% at

£1,367m compared with revenue of £1,260m for the 52 weeks ended 27 April

2008. At constant exchange rates the increase was 5.1%. UK Retail sales were

up 5.1% and broke through £1bn again to £1,006m (2008: £958m). Adjusted for

acquisitions and disposals of subsidiaries, UK Retail sales in 2009 increased by

9.2%.

The Group strengthened revenues in other core business segments.

International retail sales were up 32.3% to £102.3m (2008: £77.3m); on a

currency neutral basis the increase was 12.6%. Brands division revenue rose

19.7% to £230.5m (2008:£192.6m); 4.7% on a currency neutral basis. Within the

division, wholesale revenues were up 18.7% to £203.6m (2008: £171.5m) and

licensing revenues were up 27.5% to £26.9m (2008: £21.1m), both reflecting

the full year impact of acquisitions in the prior year including Everlast, and the

effect of a stronger US dollar.

Group gross margin in the Year fell by 280 basis points from 43.6% to 40.8%. In

the Retail division margin fell by 300 basis points to 41.3% (2008: 44.3%). The

main contributor to the fall in margin was UK Retail where margin fell to 42.5%

(2008: 45.7%) as a result of the adverse movement of the US dollar and the

challenging trading environment in the UK. Had the pound/dollar exchange rate

remained at 2008 levels, gross margin in UK Retail would have been maintained

at 45.7%.

Gross margin fell in the Brands division from 40.2% to 38.3%, due to the

pressure on margins in the wholesale business in an increasingly competitive

global market.

Administration costs include a realised exchange profit of £14.2m compared

to a profit of £3.5m in the preceding year. The fair value adjustment on forward

foreign exchange contracts required under IFRS is included in finance income

(2008:costs) and this unrealised profit amounted to £12.6m as opposed to

a £5.2m loss in 2008. These amounts are excluded from the definition of

Underlying profit before tax and Underlying EBITDA used in the business and as

reported here. The Group’s holding of forward foreign exchange contracts has

greatly reduced during the Year, reducing an element of potential volatility in

reported profit, and we expect the holding to continue at or below the current

low level in 2009/10.

Group Underlying EBITDA for the Year fell 8.9% to £136.8m (2008: £150.2m) and

Group Underlying profit before tax fell 20.2% to £68.2m (2008: £85.4m), in both

cases due to the decreases in margin.

There is a significant difference between Underlying and the lower reported

profits before tax. Underlying profits before tax (and Underlying EBITDA) exclude

exceptional items, which decreased profit by £30.5m, realised exchange profit/

loss and IFRS revaluation of foreign currency contracts, which increased

2009 profits by £14.2m and £12.6m respectively, a £1.8m loss on fair value

adjustments within associated undertakings and a £52.1m non-cash loss in

the recorded value of investments previously provided for through equity and

now charged to the Income Statement as a result of the derecognition of the

investment for accounting purposes.

EBITDA PBT

£m £m

Reported 151.0 10.7

Realised FX Profit (14.2) (14.2)

IAS 39 FX Fair Value adjustment on

forward currency contracts - (12.6)

Profit on disposal of listed investments - (1.0)

Derecognition of investments held

by KSF - 53.1

Exceptional items - 30.5

Fair value adjustment within

associates - 1.7

Underlying 136.8 68.2

Capital expenditure in the Year amounted to £37.8m (2008: £128.8m). This

included acquisitions of retail property, plant and equipment, including £6.4m

(2008: £90.6m) on freehold property.

The Group continues to operate comfortably within it banking covenants. Our

facilities are in place until April 2011 and we will commence discussions with

our banks during the 2009-10 financial year.

Mindful that the financial markets remain difficult, we consider it is prudent that

debt reduction should be priority. We are therefore targeting to reduce levels to

below £400m by April 2010, which will be achieved by:

• Growing EBITDA

• Working capital turning positive by the year end, as we reduce inventory

levels through the year

• Targeting a reduced level of capital expenditure, in the region of £20m, in

the current year

• Further reductions in financing costs as a result of ongoing low interest

rates (and the reduction in debt)

• Saving the cost of the final dividend

Net debt at year end decreased to £431.3m (2008: £465.2m), £20.3m of the

reduction resulted from the accounting treatment of the arrangements with

Kaupthing Singer and Friedlander (see page 11).

CHIEF EXECUTIVE’S REPORT AND BUSINESS REVIEW

None of the home nations qualified for the Euro 2008 football championships.

Undoubtedly sales in 2008-09, particularly in the first half, were significantly

affected by that lack of home nations’ participation in a major international

football competition.

Gross margin in the division during the Year was adversely affected by the

weakness of the pound against the US dollar. Margin in the division fell from

44.3% to 41.3% in the Year, and in the UK from 45.7% to 42.5%, with the

greatest fall in margin coming in the second half of the Year. Almost all the

Group branded goods that we sell in our stores are bought in US dollars, and

we calculate the cost price of these goods in sterling by applying the average

exchange rate for the year. Had the pound/dollar exchange rate remained at

2008 levels gross margin in UK Retail would have been 45.7%. We expect the

percentage margins in 2009-10 to remain at similar levels to the actual level in

2008-09.

UK Retail like-for-like gross contribution increased by 2.5% over the 12 month

period. This is the first time we have reported this KPI.

Underlying costs in UK Retail were closely controlled, rising by only 0.7% in the

Year, in spite of significant increases in the cost of energy, the minimum wage,

an increase in floor space and a rise in sales of just over 5%.

During the Year the Office of Fair Trading (OFT) investigated our acquisition

of stores from JJB Sports, and concluded that in five locations they raised

some concerns. We are currently working with the OFT to agree undertakings

regarding divestment of five stores.

International Retail revenue for the 52 weeks was up 32.3% to £102.3m (2008:

£77.3m). On a currency neutral basis the sales increase was 12.6%. We

opened seven new stores across Europe in the period, in line with our plans for

developing our international store portfolio, and trading has been satisfactory in

those new stores.

International Retail grew gross margin by 170 basis points, largely due to

improved stock control and sourcing.

By July 2008 trial branded areas within stores had been opened in 121 of the

larger ITAT stores in China, stocked with a bespoke product range designed

and manufactured for the Chinese market. We were extremely pleased with

the execution of the roll out and merchandising of the branded areas and

feedback was that the product range was well received by consumers. We

were in discussions with ITAT management concerning the development of the

business, and some issues were proving difficult to resolve, but ITAT has very

recently been acquired by one of its largest suppliers, and those discussions are

now on hold. Accordingly, we consider it prudent to make a provision against the

cost of fixtures, fittings and stock currently held in China.

Our internet retail business continues to grow strongly, albeit from a low base,

and we continue to build systems and fulfilment capability within our Shirebrook

facility.

STORE PORTFOLIO

As of 26 April 2009, we operated 359 stores in the UK (excluding Northern

Ireland), a total retail sales space of circa 3.5m sq ft (2008: circa 3.4m sq ft).

Through the Group’s 42.5% shareholding in the Heatons chain, it has products in

eight stores in Northern Ireland and 22 stores in the Republic of Ireland.

We closed a net 16 stores in the year, with 27 new Sports Direct stores opened

in the UK including three relocations. All new stores are operating under the

sportsdirect.com fascia. We closed or disposed of 40 stores (excluding the three

relocations) which were typically smaller non-core stores.

We have rigorous criteria that must be satisfied before any new store opening or

acquisition is agreed, and we will continue to apply them. We are now targeting

circa between 10 and 15 new core stores in the UK excluding Northern Ireland

this year.

Internationally, as at 26 April 2009 we operated 43 stores in Belgium, 13 in

Slovenia, four in Holland, two in Cyprus and one in Luxembourg. The stores in

Belgium, Holland, Luxembourg and Slovenia are wholly owned by the Group,

and those in Cyprus are within a store under an agreement with a local retailer.

We continue with our strategy to identify partners in new territories whilst

continuing to expand our operations in the countries where we currently trade.

Chief Executive’s Report & Business Review

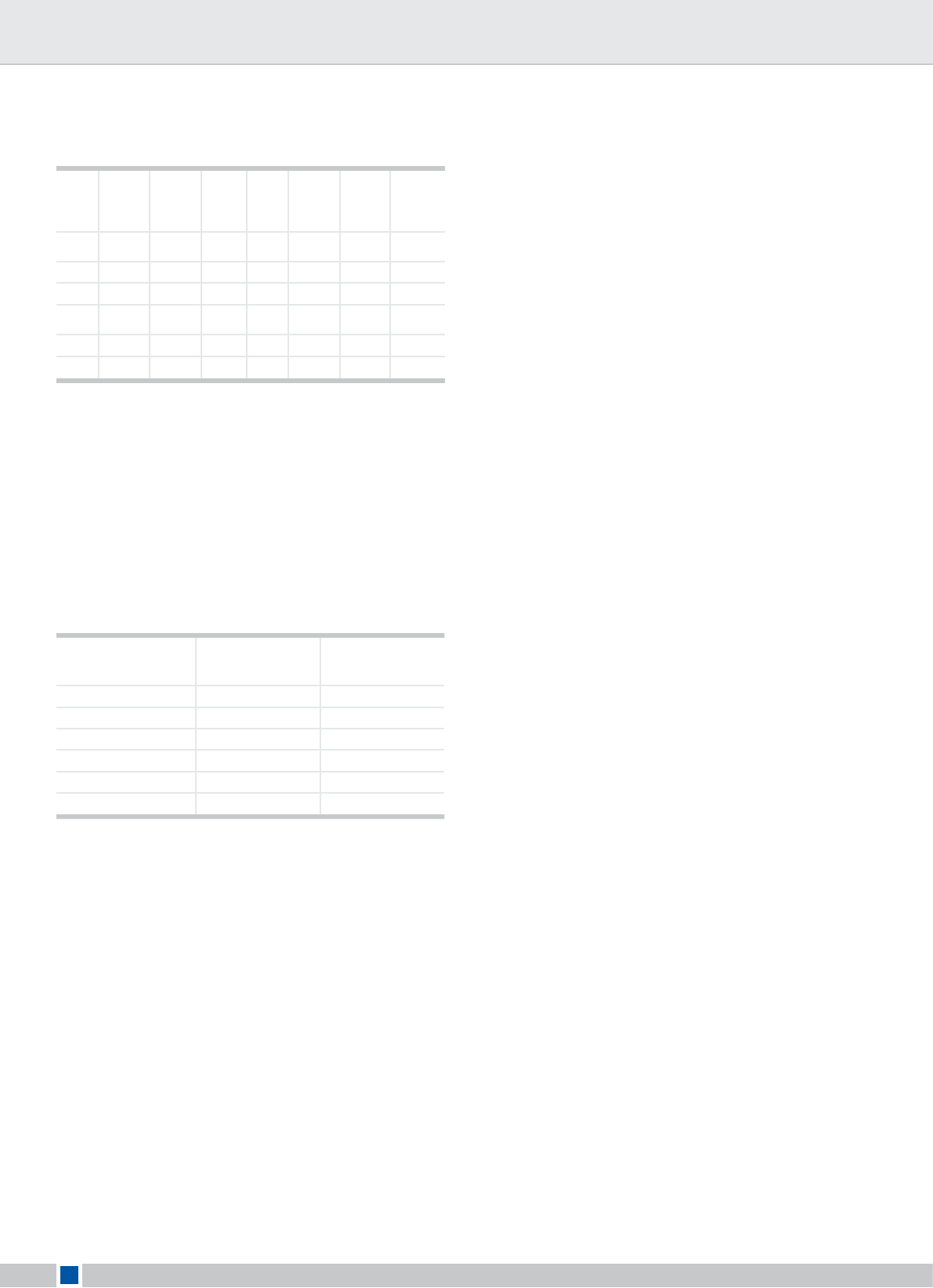

REVIEW BY BUSINESS SEGMENT

52 weeks ended

26 April 2009

52 weeks ended

27 April 2008 Change

(£’m) (£’m) %

Retail Revenue:

UK Retail 1,006.5 957.7

UK wholesale and other 28 31.9

International Retail 102.3 77.3

Total 1,136.8 1,066.9 +6.6

Cost of sales (667.5) (594.7)

Gross margin 469.3 472.2

Gross margin percentage 41.3% 44.3%

Brands Revenue:

Wholesale 203.6 171.5

Licensing 26.9 21.1

Total 230.5 192.6 +19.7

Cost of sales (142.2) (115.1)

Gross margin 88.3 77.5

Gross margin percentage 38.3% 40.2%

BUSINESS REVIEW

Despite tough economic conditions, revenue grew in both the Retail and

Brands divisions, but underlying EBITDA fell notwithstanding good cost control

across the Group, almost entirely due to the strengthening of the US dollar. We

continue to focus our efforts on UK Retail, where our attention to the basics of

retailing leaves us well positioned for growth.

RETAIL DIVISION

The Group’s retail businesses performed strongly in a very difficult economic

environment. Our retail model, offering considerable value to our customers,

proved as resilient as we expected it to be both in the UK and internationally.

We focused on back to basics, offering the customer the most comprehensive

range and the best product availability, and reducing our costs wherever

possible, By way of example, in our Corporate and Social Responsibility Report

we describe some of the steps that we took to reduce our energy consumption

at a time when energy costs were increasing significantly. We continued to

review our store portfolio carefully, looking at the performance of each store

and ways of maximising it, and examined rigorously every proposal to open

or acquire a retail outlet. We continued to develop our store layout, and to

incentivise our store staff in ways that encourage better performance. Our

“state-of-the-art” national distribution centre at Shirebrook continued to deliver

efficiencies.

Sales in the division rose by 6.6% (10.3% excluding the impact of prior year

disposals), and in the UK by 5.1% (9.2% excluding prior year disposals). In the

second half of the Year sales growth accelerated due to both the impact of

new store openings, the attractiveness of our offer compared with that of our

competitors, and product availability.

We continued to work well with our major third party brand suppliers. Nike,

Umbro, adidas, Reebok and Puma all have their own offices in our Shirebrook

head office, and that enables us to work very closely with them on a day to day

basis.

During the Year we strengthened our running category, through our partnership

with Sweatshop and the creation of a “she runs he runs” section within our UK

stores.

CHIEF EXECUTIVE’S REPORT AND BUSINESS REVIEW CONTINUED

4

Sports Direct International PLC Annual Report 2009 5

BRANDS DIVISION

Total Brands revenue was up 19.7% to £230.5m (2008: £192.6m) up 4.7% on a

currency neutral basis.

Within this, wholesale revenue was up 18.7% to £203.6m (2008: £171.5m).

Revenue from licensing was up 27.5% to £26.9m (2008: £21.1m).

Gross margin decreased to 38.3% from 40.2%, due to the need to remain

competitive in a number of markets in order to retain market share in a difficult

trading environment.

The consolidation of the Brands division management into Shirebrook

continued, and costs were tightly controlled as systems and controls were

standardised. Payroll costs in the division reduced significantly.

Growth in the licensing business remains the preferred avenue for development

of the Brands business outside the UK and 41 new licensing agreements were

signed during the Year with a minimum guaranteed contract value of 60m US

dollars over their terms, including licences in the United States for Donnay

rackets and golf, Lonsdale boxing equipment, Dunlop sports apparel and Kangol

clothing.

The business continues to sponsor and receive endorsements from leading

players and tournaments including Slazenger’s 107th year as the official ball

supplier for the Wimbledon championships, sponsorship of Paul Collingwood,

England’s captain at the ICC World Twenty20 cricket competition, and the

England mens and womens national hockey teams.

During the Year we greatly expanded our cycle category following the acquisition

of Universal Cycles, and launched our online cycle business, cyclesdirect.com.

We also acquired the 20% minority shareholding in Lonsdale Sports not

previously owned by the Group.

During the Year we made a number of small brands acquisitions such as

Golddigga.

Operating costs increased in the division due to the full year inclusion of

acquisitions such as Everlast, and the impact of the weak pound on non-sterling

costs when translated into sterling.

STRATEGIC INVESTMENTS

During the Year we reduced our strategic investments in other related

businesses. We still believe that in the right circumstances taking strategic

investments is beneficial for the Group, and the Board will continue to evaluate

opportunities. However strategic investments compete with other priorities,

including debt reduction, for cash, and it is unlikely that further significant

investments will be made in the short term. In addition, as explained in the

Financial Review on page 11, we have for accounting purposes derecognised the

strategic investments held through arrangements with Kaupthing Singer and

Friedlander.

CONTRACTS ESSENTIAL TO THE BUSINESS OF THE GROUP

The Group has long established relationships with Nike and adidas, the major

suppliers of third party branded sporting goods, particularly footwear, and

considers that continued supplies from these companies is critical to the

business of the Group.

MAIN TRENDS AND FACTORS LIKELY TO AFFECT THE FUTURE DEVELOPMENT

AND PERFORMANCE OF THE GROUP’S BUSINESSES

The Group’s retail businesses will undoubtedly be affected by the economic

climate and changes in it. Changes in interest rates and exchange rates affect

the businesses directly, and consumer confidence and spending is affected by a

wide range of factors including employment, tax and interest rates, house prices

and the general ‘feel good factor’, most if not all of which the Group cannot

influence.

The above factors also influence and impact on our many retail competitors,

who may also be affected by other matters relating to the general economic

climate, such as the availability of finance, and also our suppliers may react

differently to the changing economic environment.

All of the above apply equally to our Brands businesses, both wholesale and

retail. Reduction in customer demand is reflected in the wholesaling and

licensing business, as orders and royalties are affected. Moreover, in difficult

economic times suppliers come under increasing pressure to reduce their

prices to their customers, and all suppliers run the risk of their customers

ceasing to trade, reducing demands for their products. Difficult economic

times also sometimes make it difficult for suppliers to obtain credit insurance

in respect of some customers, leaving the supplier with a difficult question of

whether or not to supply and, if they do, with the attendant risk of bad debts.

We have later in this report commented on risks and uncertainties that relate

to the Group’s businesses, and while we manage risks to reduce, where

possible, the likelihood of their occurring and their impact if they do, they are

factors that could influence the Group or part of it.

We anticipate that the football World Cup in 2010 will be a major opportunity

for the UK Retail business, but given the likely launch of new football strips

in March - a month later than in previous years - it’s impact (subject to

qualification of the home nations – and in particular England) will come later

in the calendar year than hitherto, and will be largely reflected in the 2010–11

financial year.

As previously commented, the Group’s holding of forward foreign exchange

contracts has greatly reduced during the Year, reducing an element of

potential volatility in reported profit, and we expect the holding to continue at

or below the current low level in 2009–10.

ENVIRONMENTAL MATTERS

A review of the assessment of the Group’s impact on the environment, is

included in the Corporate Social Responsibility Report on page 29.

EMPLOYEES

The hard work and loyalty of our employees are key to our success, and we

intend to motivate them and enable them to share in the Group’s success by

seeking shareholder approval at the AGM for a new bonus scheme.

The bonus scheme is intended to drive underlying EBITDA, and to motivate

and help improve retention of key employees, to encourage those employees

participation in the shares of the Company and to align the interests of those

employees and shareholders.

All permanent UK employees in UK Retail, Brands and Head Office with at

least one year’s service at the beginning of 2009/10 will participate. The

scheme will replace, where relevant, existing annual bonus schemes, but not

workplace based schemes. The bonus targets are stretch targets, and are net

of scheme costs.

The bonus is in two stages. The first bonus is 25% of base pay in shares at

£1.00 per share. The first bonus target is Underlying EBITDA of £155m in

2009-10. The first bonus will vest two years after the EBITDA target of £155m

is reached, and is subject to continuous employment until then.

The second bonus is 75% of base pay in shares at £1.25 per share. The second

stage of the bonus is conditional upon the first bonus target being met in

2009-10, and the second bonus targets are Underlying EBITDA of £195m in

2010-2011, and Underlying EBITDA/Net Debt ratio of 2 or less at the end of

2010-11. The shares vest, subject to continuous employment until then, 2

years after the second bonus targets are met.

SHIREBROOK CAMPUS

The Group continues to invest in infrastructure, and the process of

consolidating the Brands business, including acquired businesses, at

Shirebrook continues.

RISKS AND UNCERTAINTIES RELATING TO THE GROUP’S BUSINESS

Risks are an inherent part of the business world. The Group has identified

the following factors as potential risks to, and uncertainties concerning, the

successful operation of its business.

SUPPLY CHAIN

Any disruption or other adverse event affecting the Group’s relationship with

any of its major manufacturers or suppliers, or a failure to replace any of its

major manufacturers or suppliers on commercially reasonable terms, could

have an adverse effect on the Group’s business, operating profit or overall

financial condition.

FOREIGN EXCHANGE RISK

The Group operates internationally and is exposed to foreign exchange risk

arising from various currency exposures, primarily with respect to the US

dollar and Euro.

Foreign exchange risk arises when future commercial transactions or

recognised assets or liabilities are denominated in a currency that is not the

entity’s functional currency, as exchange rates move. As explained above,

in the Group’s case, the majority of contracts relating to the sourcing of

Group branded goods are denominated in US dollars, and a strengthening

of the dollar or a weakening of the pound sterling makes those goods more

expensive.

Chief Executive’s Report & Business Review

CHIEF EXECUTIVE’S REPORT AND BUSINESS REVIEW CONTINUED

6

Sports Direct International PLC Annual Report 2009 7

The Group historically hedged the risk of currency movements using forward

purchases of foreign currency, but has determined to reduce that hedging

significantly.

The Group also holds assets overseas in local currency, and these assets are

revalued in accordance with currency movements. This currency risk is not

hedged.

INTEREST RATE RISK

The Group has net borrowings, which are principally at floating interest rates

linked to bank base rates or LIBOR. The Group does not use interest rate

financial instruments to hedge its exposure to interest rate movements.

CREDIT RISK

The Group could have a credit risk if credit evaluations were not performed

on all customers requiring credit over a certain amount. The Group does not

require collateral in respect of financial assets.

FUNDING AND LIQUIDITY RISK

Funding and liquidity for the Group’s operations are provided through bank

loans, overdrafts and shareholders funds. The object is to maintain sufficient

funding and liquidity for the Group’s requirements, but the availability of

adequate cash resources from bank facilities and achieving continuity of

funding in the current financial climate could be a risk to the Group in future

years.

INVESTMENT RISK

The Group also holds shares in publicly listed companies and fluctuations in

their share prices will have a financial impact on the business results.

RELIANCE ON NON UK MANUFACTURERS

The Group is reliant on manufacturers in developing countries as the

majority of the Group’s products are sourced from outside the UK. The Group

is therefore subject to the risks associated with international trade and

transport as well as those relating to exposure to different legal and other

standards.

PENSIONS

Some subsidiaries in the Group make contributions to certain occupational

defined benefits pension schemes. An increase in the Schemes funding needs

or changes to obligations in respect of the schemes could have an adverse

impact on the Group’s business.

MARKET FORCES

The sports retail industry is highly competitive and the Group currently

competes at national and local levels with a wide variety of retailers of varying

sizes who may have competitive advantages, and new competitors may enter

the market. Such competition continues to place pressure on the Group’s

pricing strategy, margins and profitability.

OPERATIONAL

Any significant disruption to the operations of the Group, divisional head

offices and the national distribution centre at Shirebrook, or interruption to

the smooth running of the Group’s fleet of vehicles, might significantly impact

its ability to manage its operations, distribute products to its stores and

maintain its supply chain.

Any long term interruption of the Group’s IT systems would have a significant

impact on the Group’s operation, particularly in the Retail division.

BUSINESS CONTINUITY AND ACTS OF TERRORISM

The majority of the Group’s revenue is derived from the UK and accordingly

any terrorist attacks, armed conflicts or government actions within the UK

could result in a significant reduction in consumer confidence, which would in

turn have an adverse affect on sales in stores.

LEGAL

The Group’s trade marks, patents, designs and other intellectual property

rights are central to the value of the Group brands. Third parties may try to

challenge the ownership or counterfeit the Group’s intellectual property. The

Group may need to resort to litigation in the future to enforce its intellectual

property rights and any litigation could result in substantial costs and a

diversion of resources. The Group believes that its licensees, suppliers,

agents and distributors are in material compliance with employment,

environmental and other laws. The violation, or allegations of a violation, of

such laws or regulations, by any of the Group’s licensees, suppliers, agents

or distributors, could lead to adverse publicity and a decline in public demand

for the Group’s products, or require the Group to incur expenditure or make

changes to its supply chain and other business arrangements to ensure

compliance.

SALES

The Group’s retail businesses are subject to seasonal peaks. The incidence

and participation in major sporting events will have a particular impact on the

UK Retail business. Prolonged unseasonal weather conditions or temporary

severe weather during peak trading seasons could also have a material

adverse effect on the Group’s businesses.

CONSUMERS

The Group’s success and sales are dependent, in part, on the strength and

reputation of the brands it sells, and are subject to consumers’ perceptions of

the Group and of its products, which can fall out of favour. Adverse publicity

concerning any of the Group brands or manufacturers or suppliers could lead

to substantial erosion in the reputation of, or value associated with, the Group.

RESEARCH AND DEVELOPMENT

The Group’s success depends on the strength of the Group brands and, to

a lesser extent, the licensed-in brands. The Group’s efforts to continually

develop or obtain brands in a timely manner or at all may be unsuccessful.

MANAGEMENT AND MITIGATION OF RISK

The identification and management of risk is a continuous process, and

the Group’s system of internal controls and the Group’s business continuity

programmes are key elements of that. The Group maintains a system of

controls to manage the business and to protect its assets. We continue to

invest in people, systems and in IT to manage the Group’s operations and its

finances effectively and efficiently.

The Group has a credit policy in place and the exposure to risk is monitored

on an ongoing basis. Credit evaluations are performed on all customers

requiring credit over a certain amount, and concentration of credit risk is

managed. Investment of cash surplus, borrowings and derivative investments

are made through banks and companies which have credit ratings and

investment criteria approved by the Board.

The Group’s follows policies of forging long term relationships with suppliers

and of utilising two leading supply chain companies to procure much of

the Group’s own branded goods is described on page 29 in the Corporate

and Social Responsibility Report. Many risks relating to the supply chain,

reliance on non-UK suppliers, and to the reputation of the Group’s brands are

managed and mitigated by the implementation of those policies.

Close monitoring of the market, competitors, the economy, consumer

confidence, participation in major sporting events, the weather, companies

in which the Group holds strategic stakes, the behaviour of licensees, and

of possible infringement of intellectual property, and the development of

contingency plans and rapid response to changing circumstances manages

and does much to mitigate the risks caused by these factors.

The Group maintains close contact with its bank and will address the renewal

of its facilities in 2009/10.

The business continuity programme addresses the risk of disruption to

the Shirebrook campus. Accordingly the Board is confident that as far as is

practical the risks and uncertainties that face the Group are being monitored

and managed and that where required appropriate action is being taken.

CHIEF EXECUTIVE’S REPORT AND BUSINESS REVIEW CONTINUED

Chief Executive’s Report & Business Review

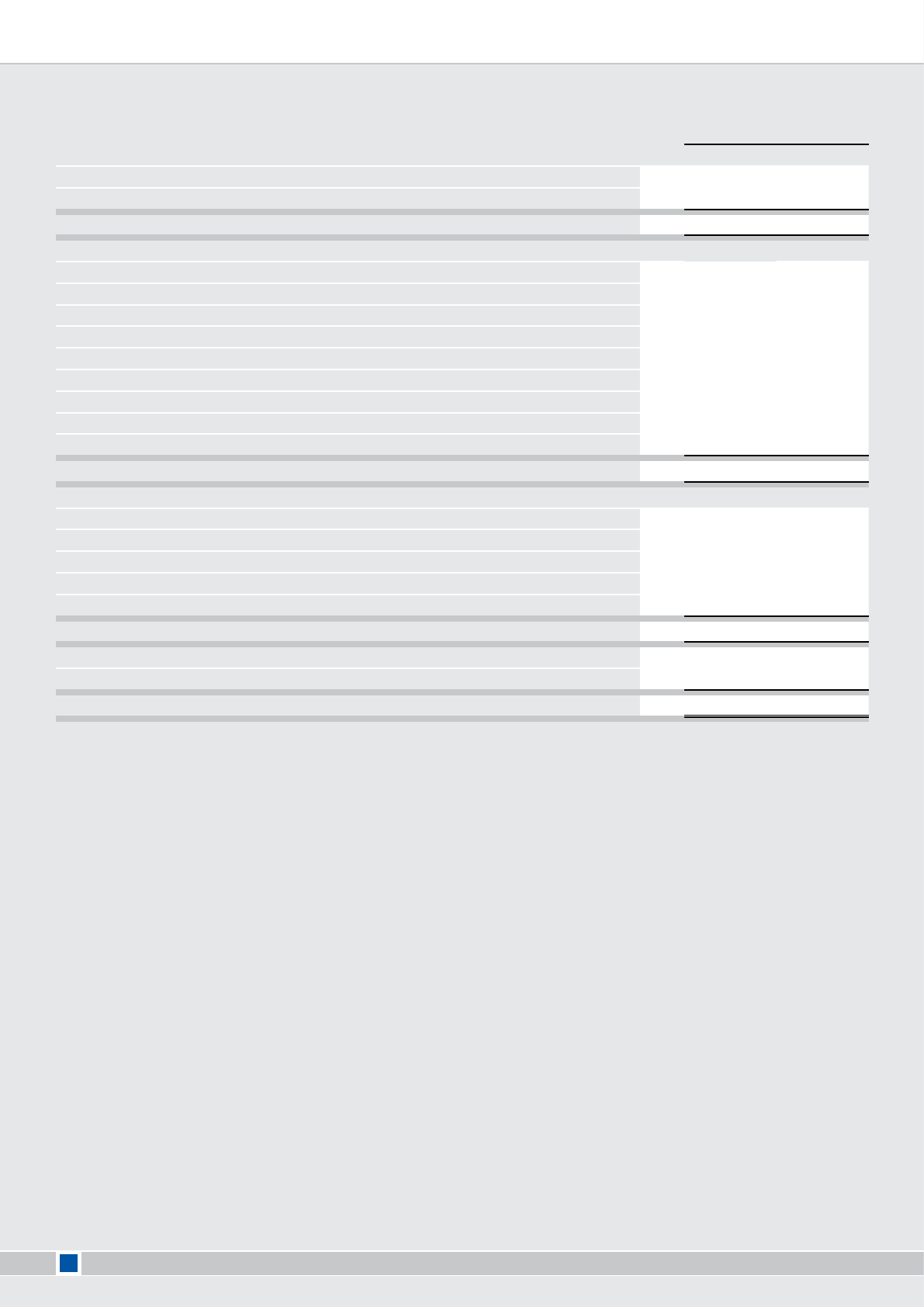

KEY PERFORMANCE INDICATORS

The Board monitors the performance of the Group by reference to a number

of key performance indicators (KPIs), which are discussed fully in this Chief

Executive’s Report and Business Review, and also in the Financial Review,

and in the Corporate and Social Responsibility Report on pages 9 to 12 and 28

to 30 respectively. The most important of these KPIs are:

52 weeks ended

26 April 2009

52 weeks ended

27 April 2008

Financial KPIs

Group revenue £1,367m £1,260m

Underlying EBITDA

(1)

£136.8m £150.2m

UK Retail gross margin 42.5% 45.7%

UK Retail like-for-like stores

gross contribution

(2)

+2.5% -

Underlying earnings per share

(3)

7.93p 8.57p

Non Financial KPIs

No. of core stores

(4)

292 272

Customer complaints %

change

(5)

-7.49% -

Employee turnover

(6)

29.0% 38.4%

Cardboard recycling 6,007 tonnes 5,558 tonnes

(1) The way in which Underlying EBITDA is calculated is set out in the Financial Review on page 9.

(2) Like-for-like gross contribution for UK Retail is percentage change in successive 12 month periods.

Like-for-like gross contribution is adjusted to eliminate the impact of foreign currency movements. A like-

for-like store is one that has been trading for the full 12 months in both periods, and has not been affected by

a significant change such as a refit. Store gross contribution is the excess of sales revenue (net of VAT) over

the cost of goods sold. The gross contribution would only be adjusted if a significant promotion affected the

comparison. This is the first year that this KPI has been reported.

(3) The way in which Underlying earnings per share is calculated is set out in the Financial Review on

page 10.

(4) A core store is a store acquired and fitted out by the Group or otherwise so designated.

(5) The monitoring of customer complaints is described in the Corporate and Social Responsibility Report

on page 28. Records containing complaints received prior to the beginning of 2007-08 were not retained, and

accordingly annual percentage change in customer complaints in 2008 is not available.

(6) Employee turnover was affected in both the Year and in 2007-08 by the relocation of head office, retail and

brand support functions, and warehousing and distribution activities to Shirebrook throughout these periods.

OUR STRATEGY FOR GROWTH

We will focus on growing the core UK Retail business by continuing to

drive efficiencies and deliver outstanding value to our customers. We have

established an excellent platform for growth, which we will build on with our

proposed EBITDA related share bonus scheme.

In order to develop our store portfolio, both in the UK and internationally, we

will continue to evaluate opportunities and will take them when we believe

there is quantifiable and significant benefit in doing so.

We have learned valuable lessons in China that we will be able to apply both

there and in other parts of the world.

Outside the UK our brands business will focus on licensing opportunities and

continue to restructuring of the wholesale businesses. We will continue to

invest in our Brands through advertising and promise to spend and develop

grass roots initiatives.

We believe that making acquisitions and taking strategic investments in

other related businesses is beneficial for the Group, and we will continue to

evaluate opportunities while, for the time being, being mindful of the priority

to reduce debt.

OUTLOOK FOR THE CURRENT YEAR

The Board is confident that our initiatives and hard work across all areas of

the Group leaves us well positioned for the next phase of growth. Accordingly,

at current exchange rates, we are expecting Underlying EBITDA to be at least

£140m this financial year.

Dave Forsey

Chief Executive

16 July 2009

8

Sports Direct International PLC Annual Report 2009 9

REVENUE AND MARGIN

52 weeks ended

26 April 2009

52 weeks ended

27 April 2008 Change

(£’m) (£’m) %

Retail revenue:

UK Retail 1,006.5 957.7 +5.1

UK wholesale and property 28.0 31.9 -12.2

International Retail 102.3 77.3 +32.3

Total 1,136.8 1,066.9 +6.6

Brands Revenue:

Wholesale 203.6 171.5 +18.7

Licensing 26.9 21.1 +27.5

Total 230.5 192.6 +19.7

Total revenue 1,367.3 1,259.5 +8.6

Total Group revenue increased by 8.6%.

Retail revenue increased by 6.6%. The UK accounted for 91.0% of total retail

revenues with the balance in continental European stores.

UK wholesale and other includes income on property transactions which is

not regarded as being exceptional or non recurring totalling £Nil at no margin

(2008: £10.5m at no margin).

Retail margins in the UK decreased from 45.7% to 42.5%.

Our representation in both parts of Ireland is covered by Heatons, in which we

have a 42.5% interest, the results of which are reported as an associate.

Brands revenue increased by 19.7%, including the full year effect of prior year

acquisitions such as Everlast. Licensing income increased by 27.5%, with an

increase in wholesale revenue of 18.7%. The contribution made by Everlast in

the year for revenue and profit after taxation amounted to £35.9m and £4.4m

respectively.

Brands margins decreased from 40.2% to 38.3%.

SELLING, DISTRIBUTION AND ADMINISTRATION COSTS

Selling, distribution and administration costs for the Group decreased as a

percentage of revenue. This was as a result of the cost and efficiency savings

offsetting inflation.

FOREIGN EXCHANGE

The Group manages the impact of currency movements through the use of

forward fixed rate currency purchase and sales contracts. The Group’s policy

has been to hold or hedge up to four years (with generally a minimum of one

year) on anticipated purchases in foreign currency. During the Year the holding

of forward purchase contracts has been significantly reduced.

The exchange gain of £14.2m (2008: £3.5m gain) included in administration

costs have arisen from:

a) accepting dollars and Euros at the contracted rate; and

b) the translation of dollars and Euro denominated assets and

liabilities at the period end rate or date of realisation

The exchange gain of £12.6m (2008: £5.2m loss) included in finance income

substantially represents the reduction in the mark-to-market provision made

(under IFRS) for the forward contracts at 26 April 2009 in anticipation of the loss

which may be realised in the accounts to 25 April 2010.

The sterling exchange rate with the US dollar at 27 April 2008 was $1.986 and

$1.471 at 26 April 2009.

FINANCIAL REVIEW

BASIS OF REPORTING

The financial statements for the Group for the 52 weeks ended 26 April 2009

are presented in accordance with International Financial Reporting Standards

(IFRS) as adopted by the EU.

52 weeks ended

26 April 2009

52 weeks ended

27 April 2008 Change

(£’m) (£’m) %

Revenue: 1,367.3 1,259.5 +8.6

Underlying EBITDA 136.8 150.2 -8.9

Underlying profit before tax 68.2 85.4 -20.2

Reported profit before

taxation 10.7 118.9 -91.0

Pence per share Pence per share

Basic EPS (2.79) 12.23 -122.8

Underlying EPS 7.93 8.57 -7.5

The directors believe that Underlying EBITDA, Underlying profit before tax

and Underlying earnings per share provide more useful information for

shareholders on the underlying performance of the business than the reported

numbers and are consistent with how business performance is measured

internally. They are not recognised profit measures under IFRS and may not be

directly comparable with “adjusted” profit measures used by other companies.

EBITDA is earnings before investment income, finance income and finance

costs, tax, depreciation and amortisation and therefore includes the Group’s

share of profit of associated undertakings and joint ventures. Underlying

EBITDA is calculated as EBITDA before the impact of foreign exchange, and any

exceptional and other non-trading items.

Bob Mellors

Group Finance Director

Financial Review

FINANCIAL REVIEW CONTINUED

EARNINGS

52 weeks ended

26 April 2009

52 weeks ended

27 April 2008 Change

pence per share pence per share %

Basic EPS (2.79) 12.23 -122.8

Underlying EPS 7.93 8.57 -7.5

Weighted average number

of shares (actual) 568,452,000 639,010,000 -11.0

Basic earnings per share (EPS) is calculated by dividing the earnings

attributable to ordinary shareholders by the weighted average number of

ordinary shares outstanding during the actual financial period.

The Underlying EPS reflects the underlying performance of the business

compared with the prior year and is calculated using the weighted average

number of shares. It is not a recognised profit measure under IFRS and may

not be directly comparable with “adjusted” profit measures used by other

companies.

The items adjusted for arriving at the Underlying profit are as follows:

52 weeks ended

26 April 2009

52 weeks ended

27 April 2008

(£’m) (£’m)

(Loss)/profit after tax: (15.8) 78.1

Post tax effect of Exceptional items:

(Loss)/profit on disposal of listed

investments net of interest (1.0) (24.6)

Derecognition of listed investments 53.2 -

Fair value adjustment to forward

foreign exchange contracts (8.5) 3.6

Realised profit on forward foreign

exchange contracts (9.6) (2.4)

Impairment of freehold property 15.6 -

Impairment of intangible assets 10.0 -

Fair value adjustment within

associated undertakings 1.2

Underlying profit after tax 45.1 54.7

DIVIDENDS

A final dividend of 2.44p per share (totalling £13.87m), in respect of the year

ended 27 April 2008, was paid on 31 October 2008 to shareholders on the

register at 3 October 2008.

An interim dividend of 1.22p per share (totalling £6.94m), in respect of the year

ended 26 April 2009, was paid on 30 April 2009 to shareholders on the register

at 3 April 2009.

CAPITAL EXPENDITURE

Capital expenditure amounted to £37.8m (2008: £128.8m). This included £6.4m

(2008: £90.6m) on freehold property. The prior year includes a freehold office

in London was acquired for £31.9m and the purchase of freehold stores. The

remaining balance includes intangibles such as licenses.

ACQUISITIONS

The Group spent £6.6m on acquisitions during the Year. The principal acquisition

was the remaining 20% of share capital in Lonsdale Sports which was not

previously owned by the Group. This has been accounted for as a movement

between minority interests and goodwill.

EXCEPTIONAL OPERATING COSTS AND REVENUES

52 weeks ended

26 April 2009

52 weeks ended

27 April 2008

(£’m) (£’m)

Impairment of intangible assets 14.8 -

Impairment of freehold property 15.7 -

30.5

The impairment of freehold property was recognised to reflect the fall in market

values of commercial property in the last year.

The impairment of intangible assets was recognised to reflect an increase in

discount rate to reflect specific risk factors and a softening in sales growth as a

result of the economic climate.

FINANCE INCOME

52 weeks ended

26 April 2009

52 weeks ended

27 April 2008

(£’m) (£’m)

Bank interest receivable 1.2 3.1

Expected return on pension plan

assets 2.1 2.3

Fair value adjustment to forward

foreign exchange contracts 12.6 -

15.9 5.4

The profit on the fair valuing of forward foreign exchange contracts arises under

IFRS as a result of marking to market at the period end those contracts held to

hedge the Group’s currency risk.

FINANCE COSTS

52 weeks ended

26 April 2009

52 weeks ended

27 April 2008

(£’m) (£’m)

Interest on bank loans and overdrafts (20.0) (33.0)

Interest on other loans (1.1) (4.5)

Interest on retirement benefit

obligations (2.5) (2.3)

Fair value adjustment to forward

foreign exchange contracts - (5.2)

(23.6) (45.0)

The fall in interest payable is a result of the reduction in interest rates during

the year and a lower average level of debt compared with the prior year.

TAXATION

The effective tax rate on profit before tax for 2009 was 245.6% (2008: 34.6%).

This rate reflects tax relief being unavailable on the derecognition of listed

investments and the impairment of freehold property, as well as depreciation

on non-qualifying assets and the non-relievable losses in certain overseas

subsidiaries. Excluding the impact of the derecognition of listed investments

and the impairment of freehold property, the effective rate would be 32.9%.

10

Sports Direct International PLC Annual Report 2009 11

STRATEGIC INVESTMENTS

During the Year the Group held investments in Amer Sports, Blacks Leisure,

JD Sports and JJB Sports. Changes in the value of these shares are recognised

directly in equity, while for Contracts for Difference they are recognised in the

Income Statement, in accordance with IFRS.

26 April 2009

(£’m)

Total available for sale investments at 27 April 2008 65.7

Additions in the period 4.9

Disposal proceeds in the period (12.8)

Profit taken to the income statement 2.4

Fair value adjustments taken through equity (28.6)

Derecognition of shares held by KSF (26.1)

Total available for sale investments at 26 April 2009 5.5

We have previously reported that our strategic stakes were held by Kaupthing

Singer & Friedlander (KSF) and partly financed by them. On 8 October 2008

KSF went into administration and we are in dispute with the administrators

concerning the ownership of the shares they hold. We have now concluded

that, while we continue to maintain that the shares are ours and should be

delivered to us, we may not “control” the shares for accounting purposes. We

have therefore treated them in the accounts as having been derecognised. Doing

so has no impact on net assets as the value of the shares (£26.1m) has been

replaced by a reduction in creditors (£20.3m owed to KSF) and the creation of a

£5.9m debtor. It has however, had a significant impact on reported profit as the

loss in value of the Black’s shareholding which was previously charged to the

statement of recognised income and expense has now been taken to the Income

Statement.

The respective shareholdings at 26 April 2009 and 27 April 2008 (not reflecting

the derecognition for accounting purposes) were as follows:

At 26 April 2009 At 27 April 2008

Shares

‘m Holding

Shares

‘m Holding

Blacks

Leisure Group 12.728 29.85% 12.728 29.85%

Amer Sports Corporation 1.066 1.48% 1.066 1.48%

JD Sports Fashion 6.475 13.31% 5.955 12.34

adidas AG - - 0.398 0.02%

JJB Sports 11.944 4.76% - -

Other - - - -

CASH FLOW AND NET DEBT

In addition to the amounts invested in capital expenditure and acquisitions,

the Group received a net £8.9m cash inflow from the purchase and disposal of

strategic investments. Net debt decreased to £431.3m at 26 April 2009 from

£465.2m at 27 April 2008. £20.3m of the reduction in Net Debt resulted from the

derecognition of the loan used to finance strategic investments held by KSF.

The analysis of debt at 26 April 2009 was as follows:

At 26 April 2009 At 27 April 2008

(£’m) (£’m)

Cash and cash equivalents 32.4 25.4

Borrowings (463.7) (490.6)

Net debt (431.3) (465.2)

Financial Review

CASH FLOW

Total movement is as follows:

At 26 April 2009 At 27 April 2008

(£’m) (£’m)

Underlying EBITDA 136.8 150.2

Realised profit on forward foreign

exchange contracts 14.2 3.5

Taxes paid (25.3) (37.7)

Free cash flow 125.7 116.0

Invested in:-

Working capital and other (31.5) (90.5)

Acquisitions (including debt) (6.6) (120.1)

Net proceeds from investments 8.9 45.5

Reduction in KSF debt 20.3 -

Net capital expenditure (34.8) (132.4)

Share buy back programme - (201.5)

Equity dividend paid (25.6) (7.4)

Finance costs and other financing

activities (22.5) (36.7)

Decrease/(increase) in net debt 33.9 (427.1)

RECONCILIATION OF MOVEMENT IN EQUITY

Total equity movement is as follows:

(£’m)

Total equity at 27 April 2008 128.4

Loss after tax for the 52 weeks ended 26 April 2009 (15.8)

Items taken directly to equity:

Exchange differences on translation of foreign

operations (44.6)

Actuarial loss on pension (0.4)

Fair value adjustment in respect of available-for-

sale financial assets (28.6)

Transfer of historic losses on available-for-sale

financial assets 53.2

Tax on items taken directly to equity (6.9)

Movement in equity issues:

Movement in Minority interests -

Dividends paid/declared (20.8)

Total equity at 26 April 2009 153.7

PENSIONS

The Group operates a number of closed defined benefit schemes in the Dunlop

Slazenger companies. The net deficit in these schemes increased from £11.7m

at 27 April 2008 to £12.4m at 26 April 2009.

Bob Mellors

Finance Director

16 July 2009

12

Sports Direct International PLC Annual Report 2009 13

BOARD OF DIRECTORS

Simon Bentley

Acting Non-Executive

Chairman

Mike Ashley

Executive Deputy Chairman

Dave Forsey

Chief Executive

Bob Mellors

Group Finance Director

Malcolm Dalgleish

Non-Executive Director

David Singleton

Senior Independent

Non-Executive Director

Simon Bentley (aged 54) was appointed to the board on 2 March 2007 and Acting Chairman on

31 May 2007. He is also Chairman of the Audit Committee and a member of the Remuneration

Committee. As Acting Chairman he chairs the Nominations Committee. Simon qualified as

a chartered accountant in 1980 and in 1987 joined Blacks Leisure Group plc where he was

Chairman and Chief Executive for 12 years until 2002. Simon chairs and is on the board of a

range of companies and organisations. Among these, he is Deputy Chairman of the solicitors

Mishcon de Reya and a Senior Trustee of The Leadership Trust. He is the Chairman of hair

product brand Umberto Giannini and the hotelier Maypole Group Plc. He has lengthy experience

of the sporting goods industry and is a Director of the UK’s leading five-a-side football centre

operator, Powerleague.

Dave Singleton (aged 58) joined the Board on 25 October 2007. Dave spent 25 years with Reebok

International Limited. He stepped down in April 2007 having helped to successfully integrate

Reebok following its acquisition by adidas Group in January 2006. For eight years he was

Vice President Northern Europe Region & UK and since 2003 he was Senior Vice President

Europe, Middle East & Africa. Dave has an extensive senior management record and brings

valuable experience of international sports brand operations. He is Chairman of the Board’s

Remuneration Committee and a member of the Board’s Audit and Nomination Committees. He

is also a director of Bolton Lads & Girls Club.

Bob Mellors (aged 59) has been the Group’s Finance Director since 2004. A graduate in

economics, he qualified with PriceWaterhouseCoopers in London before joining Eacott Worrall,

where Sports Direct became a client in 1982. He was managing partner and head of corporate

finance at Eacott Worrall before joining the business.

Dave Forsey (aged 43) has been with the business for over 24 years, during which he has acquired

significant knowledge and experience. He is Chief Executive and has overall responsibility for

the business.

Malcolm Dalgleish (57) joined the Board on 25 October 2007. Malcolm is currently head of

retail in the Europe, Middle East and Africa area at CB Richard Ellis. In 2005 CBRE acquired

Dalgleish - the leading retail real estate services specialist in the UK, which Malcolm founded in

1979 and of which he was the principal shareholder. Malcolm is a member of the Board’s Audit,

Nomination and Remuneration Committee.

Mike Ashley (aged 44) established the business of the Group on leaving school in 1982 and was

the sole owner of the business until the Company’s listing in March 2007. Mike is the Executive

Deputy Chairman and is responsible for formulating the vision and strategy of the Company.

Mike is a member of the Board’s Nomination Committee.

DIRECTORS’ REPORT

The Group’s forecast and projections, taking account of reasonably possible

changes in trading performance, show that the Group should be able to operate

within the level of the current facility. The Group will open renewal negotiations

with the bank during 2009/10 and has at this stage not sought any written

commitments that the facility will be renewed. However, the Group regularly

holds discussions with its bankers about its present and future borrowing needs

and no matters have been drawn to its attention to suggest that renewal may

not be forthcoming on acceptable terms.

After making enquiries, the directors have a reasonable expectation that the

Company and the Group have adequate resources to continue in operational

existence for the foreseeable future. Accordingly, they continue to adopt the

going concern basic in preparing the Annual Report and Accounts.

APPROPRIATIONS

An interim dividend of 1.22p per share was paid to shareholders on the register

at 30 April 2009.

GROUP STRUCTURE AND OPERATIONS

During the Year the Group acquired the 20% of Lonsdale Sports Limited not

already owned by the Group and disposed of Streetwise Sports Limited.

SHARE CAPITAL

The authorised share capital of the Company is £100,000,000 divided into

999,500,010 ordinary shares of 10p each and 499,990 redeemable preference

shares of 10p each.

The ordinary shares have all the rights that usually attach to such ordinary

shares, including the right to receive dividends (if paid or declared), to receive

notice and attend and vote at meetings of shareholders and (subject to what is

said below concerning redeemable preference shares) to receive a share of the

assets of the Company on any winding up.

The redeemable preference shares do not carry any right to receive a dividend

or to participate in any distribution of the profits or assets of the Company, or

to vote at meetings of shareholders, but holders of redeemable preference

shares have the right to receive notice and attend meetings of shareholders

and on any winding up of the Company the redeemable preference shares are

redeemed at par in priority to any distribution to the holders of ordinary shares.

No redeemable preference shares are in issue.

640,452,369 ordinary shares of 10p are in issue and fully paid of which

64,000,000 are currently held in Treasury. On 16 September 2008, 8,000,000

shares were sold from Treasury to the Sports Direct International plc Employee

Benefit Trust (the EBT).

Grants in respect of 4,397,128 shares have been made under the Performance

Share Plan, which is described in the Directors Remuneration Report on pages

23 to 24. The Trustee of the EBT has agreed to use shares held by them to

satisfy awards that vest under that plan.

TRANSFER OF SHARES

A member may transfer all or any of his certificated shares by an instrument of

transfer in any usual form or in any other form which the Board may approve.

An instrument of transfer shall be signed by or on behalf of the transferor and,

unless the share is fully paid, by or on behalf of the transferee. An instrument of

transfer need not be under seal.

The Board may, in its absolute discretion, refuse to register the transfer of a

certificated share which is not a fully paid share, provided that the refusal does

not prevent dealings in shares in the Company from taking place on an open and

proper basis.

The Board may also refuse to register the transfer of a certificated share unless

the instrument of transfer:

• is lodged, duly stamped (if stampable), at the registered office of the

Company, or at another place appointed by the Board, accompanied by the

certificate for the share to which it relates and such other evidence as the

Board may reasonably require to show the right of the transferor to make

the transfer;

• is in respect of one class of share only, and

• is in favour of not more than four persons.

The directors of Sports Direct International plc present their annual report to

shareholders, together with the audited consolidated financial statements for

the Company and its subsidiaries for the 52 weeks ended 26 April 2009 (the

Year).

This document contains a number of forward-looking statements relating to

the Company and its subsidiaries (the Group) with respect to, amongst others,

the following: financial conditions; results of operations; economic conditions

in which the Group operates; the business of the Group and future benefits

of the current management plans and objectives. The Group considers any

statements that are not historical facts as “forward-looking statements”. They

relate to events and trends that are subject to risks and uncertainties that could

cause the actual results and financial position of the Group to differ materially

from the information presented in the relevant forward-looking statement.

When used in this document the words “estimate”, “project”, “intend”, “aim”,

“believe”, “expect”, “should”, and similar expressions, as they relate to the

Group and the management of it, are intended to identify such forward-looking

statements. Readers are cautioned not to place undue reliance on the forward-

looking statements which speak only as at the date of this document. Neither

the directors nor any member of the Group undertake any obligation publicly to

update or revise any of the forward-looking statements, whether as a result of

new information, future events or otherwise, save in respect of any requirement

under applicable laws, the Listing Rules, and other regulations.

PRINCIPAL ACTIVITIES

The principal activities of the Group during the Year were:

• Retailing of sports and leisure clothing, footwear and equipment;

• Wholesale distribution and sale of sports and leisure clothing, footwear

and equipment under Group owned or licensed brands; and

• Licensing of Group brands.

Further information on the Group’s principal activities is set out in About Sports

Direct International plc at the front of this document and in the Chief Executive’s

Report and Business Review on pages 3 to 8.

RESULTS FOR THE YEAR

The trading results for the Year and the Group’s financial position as at the

end of the Year are shown in the attached Financial Statements, and discussed

further in the Chief Executive’s Report and Business Review and in the Financial

Review on pages 3 to 8 and 9 to 12 respectively.

BUSINESS REVIEW AND FUTURE DEVELOPMENTS

The statutory Business Review required by the Companies Act 2006 (the 2006

Act) is included in the Chief Executive’s Report and Business Review, and in

the Corporate and Social Responsibility Report on pages 3 to 8 and 28 to 30

respectively. A review of Group activities during the Year, together with the

factors likely to affect its future development, performance and conditions, is

included in the Chief Executive’s Report and Business Review on pages

4 to 8. The financial position of the Group, its cash flow, liquidity position and

borrowing facilities are described in the Financial Review on pages 9 to 12. The

Chief Executive’s Report and Business Review also describes on page 6 and

7 the principal risks and uncertainties that face the Group, and note 3 to the

Financial Statements includes the Group’s objectives, policies and processes for

managing its capital, its principal financial risk management objectives, details

of its financial instruments and hedging activities and its exposure to credit

risk and liquidity risk. Details of the Group’s Key Performance Indicators by

reference to which the development, performance and position of the business

can be measured effectively are stated in the Chief Executive’s Report and

Business Review on page 8.

The Corporate and Social Responsibility Report on pages 28 to 30 reports on

environmental matters, including the impact of the Group’s businesses on the

environment, the Group’s employees, and on social and community issues.

GOING CONCERN

As highlighted in note 25 to the Financial Statements, the Group finances its day

to day working capital requirements and has made investments and conducted

a share buy-back programme in the past, using a facility with the Bank of

Scotland that is due for renewal in April 2011. The current economic conditions

however, create some uncertainty in the economy and particularly in respect

of the exchange rate between sterling and the US dollar which impacts on the

cost of the Group’s products manufactured in the Far East, and the availability of

bank finance in the foreseeable future.

Directors’ Report

14

Sports Direct International PLC Annual Report 2009 15

THE COMPANY’S POWER TO PURCHASE SHARES

At the Company’s Annual General Meeting on 10 September 2008 the Company

was generally and unconditionally authorised to make market purchases (within

the meaning of section 163(3) of the 1985 Act) of ordinary shares of 10p each in

the Company subject to the following conditions:

• the maximum aggregate number of ordinary shares authorised to be

purchased is 57,645,236, representing 10% of the Company’s issued

ordinary share capital;

• the minimum price (exclusive of expenses) which may be paid for an

ordinary share is 10p (being the nominal value of an ordinary share);

• the maximum price (exclusive of expenses) which may be paid for each

ordinary share is the higher of: (i) an amount equal to 105% of the average

of the middle market quotations for the Ordinary Shares as derived

from the London Stock Exchange Daily Official List of the five business

days immediately preceding the day on which the share is contracted

to be purchased; and (ii) an amount equal to the higher of the price of

the last independent trade of an ordinary share and the highest current

independent bid for an ordinary share as derived from the London Stock

Exchange Trading System.

The above authority expires at the close of the next Annual General Meeting

of the Company, but at that meeting a similar authority will be sought from

shareholders.

SHAREHOLDERS

No shareholder enjoys any special control rights, and, except as set out above

and below, there are no restrictions in the transfer of shares or of voting rights.

Mike Ashley and the Company have entered into a Relationship Agreement,

pursuant to which Mike Ashley undertook to the Company that, for so long as he

is entitled to exercise, or to control the exercise of, 15% or more of the rights to

vote at general meetings of the Company, he will;

• conduct all transactions and relationships with any member of the Group

on arm’s length terms and on a normal commercial basis and with the

approval of the non-executive directors;

• exercise his voting rights or other rights in support of the Company

being managed in accordance with the Listing Rules and the principles

of good governance set out in the Combined Code and not exercise any of

his voting or other rights and powers to procure any amendment to the

Articles of Association of the Company;

• other than through his interest in the Company, not have any interest in

any business which sell sports apparel and equipment subject to certain

rights, after notification to the Company, to acquire any such interest

of less than 20% of the business concerned, and certain other limited

exceptions, without receiving the prior approval of the non-executive

directors;

• and not solicit for employment or employ any senior employee of the

Company.

As at 16 July 2009, the following party had a significant direct or indirect share

holding in the shares of the company:

Number of

shares held

Percentage of issued

ordinary share capital

with voting rights held

Nature

of holding

MASH Holdings Limited 410,400,000 71.2% Direct

MASH Holdings Limited is wholly owned by Mike Ashley.

SUPPLIERS

It is the policy of the Group to agree appropriate terms and conditions for its

transactions with suppliers (ranging from standard written terms to individually

negotiated contracts) and for payment to be made in accordance with these

terms, provided the supplier has complied with its obligations.

The number of days purchases outstanding for the Group’s UK operations as 26

April 2009 was 36 days (2008: 27 days).

The Board may refuse to register a transfer of shares in the Company by a

person if those shares represent at least a 0.25% interest in the Company’s

shares or any class thereof and if, in respect of those shares, such person has

been served with a restriction notice after failure (whether by such person or

by another) to provide the Company with information concerning interests in

those shares required to be provided under the Companies Act 2006 (the 2006

Act), unless (i) the transfer is an approved transfer (as defined in the Articles of

Association of the Company), (ii) the member is not himself in default as regards

supplying the information required and certifies that no person in default as

regards supplying such information is interested in any of the shares the subject

of the transfer, or (iii) the transfer of the shares is required to be registered by

the Uncertificated Securities Regulations 2001.

If the Board refuses to register a transfer of a share in certificated form, it will

send the transferee notice of its refusal within two months after the date on

which the instrument of transfer was lodged with the Company. No fee may be

charged for the registration of any instrument of transfer or other document

relating to or affecting the title to a share.

POWERS TO ISSUE SHARES

At the Company’s Annual General Meeting on 10 September 2008:

• the directors of the Company were generally and unconditionally

authorised pursuant to section 80 of the Companies Act 1985 (the 1985

Act), in substitution for all prior authorities conferred upon them, but

without prejudice to any allotments made pursuant to the terms of such

authorities, to exercise all the powers of the Company to allot relevant

securities (within the meaning of that section) up to an aggregate nominal

amount of £19,215,078 for the period expiring (unless previously revoked,

varied or renewed) at the conclusion of the next Annual General Meeting

of the Company save that the Company may, before such expiry make an

offer or agreement which would or might require relevant securities to be

allotted after such expiry and the directors may allot relevant securities

in pursuance of such an offer or agreement as if the authority had not

expired;

• the directors were empowered to allot equity securities (within the

meaning of section 94 of the 1985 Act) for cash, pursuant to the general

authorities described above in substitution for all prior powers conferred

upon the Board but without prejudice to any allotments made pursuant to

the terms of such powers, as if section 89(1) of the 1985 Act did not apply

to any such allotment, such power being limited to:

i) the allotment of equity securities in connection with an issue in

favour of holders of ordinary shares in the capital of the Company

in proportion (as nearly as may be) to their existing holdings of

ordinary shares but subject to such exclusions or other

arrangements as the directors deem necessary or expedient in

relation to fractional entitlements or any legal or practical problems

under the laws of any territory, or the requirements of any

regulatory body or stock exchange; and

ii) the allotment of equity securities for cash (otherwise than as

described in (i) above) up to an aggregate amount equal to 5% of

the then issued and unconditionally allotted share capital of the

Company provided always that such power expires (unless

previously revoked, varied or renewed) at the conclusion of the next

Annual General Meeting of the Company, save that the Company

may, before the end of such period, make an offer or agreement

which would or might require equity securities to be allotted after

expiry of this authority and the directors may allot equity securities

in pursuance of such an offer or agreement as if this power had not

expired.

The authorities expire at the close of the next Annual General Meeting of the

Company, but a contract to allot shares under these authorities may be made

prior to the expiry of the authority and concluded in whole or part after the

Annual General Meeting, and at that meeting similar authorities will be sought

from shareholders.

DIRECTORS’ REPORT CONTINUED

CONTRACTS ESSENTIAL TO THE BUSINESS OF THE COMPANY

The Chief Executive’s Report and Business Review sets out on page 5

information about persons with whom the Company has contractual or other

arrangements which are essential or material to the business of the Group.

TAKEOVERS

The directors do not believe there are any significant contracts that may change

in the event of a successful takeover of the Company. Details of the impact of

any successful takeover of the Company on directors’ bonus and share schemes

are set out in the Directors’ Remuneration Report on pages 23 and 24. Executive

Directors’ service contracts and non-executive directors’ appointment letters

contain no specific provisions relating to any takeover of the Company.

EMPLOYEE SHARE SCHEMES

Details of the Performance Share Plan and share awards made thereunder are

set out in the Directors’ Remuneration Report on pages 23 and 24, and on page

26. No performance period has yet been completed under that plan. At the next

Annual General Meeting of the Company the Company intends to seek approval