Examination of Federal Financial Assistance in

the Renewable Energy Market

Implications and Opportunities for Commercial Deployment of

Small Modular Reactors

October, 2018

EXAMINATION OF FEDERAL FINANCIAL ASSISTANCE IN THE RENEWABLE ENERGY MARKET

P AGE | i

In association with

ACKNOWLEDGMENTS

This Report was prepared pursuant to a contract with CNI Global Solutions, LLC with

funding from U.S. Department of Energy (“DOE”), Office of Nuclear Energy, Prime Contract

DE-NE0008514.

The views and assumptions described in this report are those of the authors. This

Report does not represent the views of DOE, and no official endorsement should be inferred.

The authors of this Report are Seth Kirshenberg, Richard Butterworth and Hilary

Jackler at Kutak Rock LLP and Brian Oakley and Wil Goldenberg at Scully Capital Services,

Inc. The authors gratefully acknowledge the assistance of federal government officials

working to support the small modular reactor program and the development of nuclear

power. DOE provided the resources for this Report and invaluable leadership, guidance,

and input.

In particular, the authors appreciate the leadership, support, guidance, and input

from Tim Beville, Program Manager, Small Modular Reactors Program at DOE and Tom

O’Connor, Director, Office of Advanced Reactor Deployment at DOE. Additionally, the

authors appreciate the input and guidance provided by other individuals at DOE and the

many other entities that reviewed and provided input and technical guidance on the drafts

of this Report.

EXAMINATION OF FEDERAL FINANCIAL ASSISTANCE IN THE RENEWABLE ENERGY MARKET

P AGE | i

In association with

Table of Contents

Executive Summary .................................................................................................................................. ES-1

ES.1 Mandates and Incentives for Renewable Energy ........................................................... ES-1

ES.2 Project Level Effects of Financial Incentives ................................................................ ES-2

ES.3 Costs and Economic Benefits of Support Programs for Renewables ................. ES-3

ES.4 Application to SMRs ........................................................................................................... ES-7

ES.5 Next Steps............................................................................................................................ ES-10

Introduction .............................................................................................................................. 1

Overview of Mandates and Incentives for Renewable Energy ................................ 3

State Renewable Portfolio Standards ...................................................................................... 3

Energy Policy Act of 2005 ........................................................................................................... 5

Recovery Act Boost to Funding Renewable Energy Projects ............................................ 7

Energy Independence and Security Act of 2007 ................................................................. 8

Executive Orders on Renewable Energy Use by Federal Agencies ................................ 9

Department of Defense Implementation of Renewable Energy Goals ....................... 10

Department of Energy, General Services Administration and other Federal Agency

Implementation of Goals ........................................................................................................................ 12

Summary ......................................................................................................................................... 15

Project Level Effects of Financial Incentives ................................................................. 16

Financial Incentives Offered to Renewables Since 2005 .................................................. 16

Effect of Incentives on Individual Projects ............................................................................ 21

Summary ........................................................................................................................................ 25

Costs and Economic Benefits of Support Programs for Renewables .................. 26

Costs of Incentive Programs .................................................................................................... 26

Benefits of Incentive Programs ............................................................................................... 34

Summary ........................................................................................................................................ 43

Application to SMRs ........................................................................................................... 45

Evolution of the U.S. Electricity Market ................................................................................. 45

Existing Challenges Influencing U.S. Electric Supply......................................................... 47

The Market Opportunity for SMRs ......................................................................................... 50

Addressing Challenges through Federal Assistance ........................................................ 52

Summary ........................................................................................................................................ 56

Next Steps for Supporting Commercial Deployment of SMRs ............................. 57

EXAMINATION OF FEDERAL FINANCIAL ASSISTANCE IN THE RENEWABLE ENERGY MARKET

P AGE | ii

In association with

Appendix A: Assumptions for LCOE analyses ................................................................................... A-1

Appendix B: Tax Expenditure Calculations .......................................................................................... B-1

B.1 Wind Power .................................................................................................................................. B-1

B.2 Solar Power ............................................................................................................................... B-12

Appendix C: Analyis of Proposed SMR Assistance ........................................................................... C-1

C.1 SMRs .............................................................................................................................................. C-2

C.2 Solar ............................................................................................................................................... C-3

C.3 Wind .............................................................................................................................................. C-5

C.4 Combined .................................................................................................................................... C-6

EXAMINATION OF FEDERAL FINANCIAL ASSISTANCE IN THE RENEWABLE ENERGY MARKET

P AGE | ES-1

In association with

EXECUTIVE SUMMARY

In numerous sectors of the economy, the Federal government has utilized financial

incentives to mobilize private sector investment and advance policy objectives. The

renewable energy sector provides a highly relevant example of how financial assistance in

the form of demand mandates and financial incentives can spur industry development.

Today, renewable energy generation is transforming the power sector in many states,

challenging traditional utility business models, and in many cases displacing traditional

baseload sources during hours of peak generation.

This report introduces these incentives, discusses how they have been utilized over the past

decade to stimulate investment in the renewable energy sector, provides data on their cost

and on their effectiveness in meeting policy objectives, and offers observations on how Small

Modular Nuclear Reactors (SMRs) could benefit from similar forms of government support.

ES.1 MANDATES AND INCENTIVES FOR RENEWABLE ENERGY

For decades, multiple Presidential Administrations attempted to promote the use of

renewable energy such as solar and wind. Such use had been limited by the higher cost of

renewables due to the lack of demand and technology development and the failure of

commercial markets to accept the technologies. While several Presidents were able to

establish renewable energy goals and policies, it was not until the period following the

passage of the Energy Policy Act of 2005 (EPAct or the Act) that significant renewable

penetration was achieved in the U.S. power sector. This market penetration can be attributed

to several factors:

• State-imposed standards to increase the use of renewable energy (Renewable

Portfolio Standards or RPS);

• Federal policies, mandates, and incentives enacted by EPAct and subsequent

legislation; and

• Executive Orders and Agency actions supporting the purchase of renewable energy.

Collectively, these measures created a multipronged approach that encouraged utilities to

enter into long-term renewable power purchase agreements with project developers, drove

down the cost of renewable energy through Federal tax and credit incentives, and harnessed

the purchasing power of the Federal government.

EXAMINATION OF FEDERAL FINANCIAL ASSISTANCE IN THE RENEWABLE ENERGY MARKET

P AGE | ES-2

In association with

ES.2 PROJECT LEVEL EFFECTS OF FINANCIAL INCENTIVES

The financial incentives introduced by EPAct and subsequent legislation addressed several

financing challenges being faced at the time: first, renewable energy projects had a limited

track record of commercial deployment, particularly with the newer technologies being

introduced at the time; and second, for several years the financial markets were recovering

from the 2008-2009 economic downturn, limiting the availability of low cost, long term debt.

The financing tools introduced by the Federal government made renewable energy projects

financially feasible.

The financial incentives introduced or extended by EPAct and subsequent legislation can be

broadly categorized into two types: tax-based incentives and credit-based incentives.

ES.2.1 Tax-Based Incentives

Tax-based incentives offer the benefit of being relatively easy to introduce and administer.

Once enacted, investors will realize the value of tax incentives by claiming credits or

deductions on their tax filings. The tax incentives utilized in the renewable sector include:

• Investment Tax Credits (ITCs): ITCs give a business a tax credit for a specified

percentage of capital expenditures for qualifying energy projects. ITCs are an

investment-based subsidy as they provide upfront financial support for the

construction of a project which is expected to deliver a specified good or service in

the future (renewable energy in this case).

• 1603 Cash Grants: The Federal government briefly offered cash grants to developers

of renewable energy projects as an alternative to ITCs in response to a decline in tax

equity financing during the 2008-2009 economic downturn which reduced the

number of investors interested in tax credits. Section 1603 of ARRA offered cash

payments to developers equal to, and in lieu of, the existing ITC (30% of qualifying

investment). This allowed developers to receive a benefit equivalent to the ITC

without relying on a tax equity investor.

• Production Tax Credits (PTCs): PTCs give a taxpaying entity a tax credit for power

output, in terms of a fixed dollar amount per unit of output. A PTC can thus be

considered a form of results-based subsidy, in that it is only paid out when the

intended product (renewable energy in this case) is delivered.

1

• Accelerated Depreciation: Accelerated depreciation—formally Modified Accelerated

Cost Recovery System (MACRS)—is a way for businesses to realize higher

1

Results-based subsidies, also commonly referred to as results-based financing (RBF) in international development, have been used to

support investment in renewables and other infrastructure. https://openknowledge.worldbank.org/handle/10986/17481

EXAMINATION OF FEDERAL FINANCIAL ASSISTANCE IN THE RENEWABLE ENERGY MARKET

P AGE | ES-3

In association with

depreciation expenses, and in turn, lower tax liabilities, earlier in the life of an asset

while still incurring the same total depreciation.

ES.2.2 Credit-Based Incentives

Credit-based incentives provide low cost, long-term debt financing at terms that are

unavailable in the private capital markets. Section 1703 of EPAct established the DOE’s loan

program targeted at projects employing innovative technology. Under the program, DOE

provides a direct loan through the Federal Financing Bank (FFB), which serves as the lender.

FFB charges interest slightly above U.S. Treasury rates. DOE then guarantees 100% of the

FFB loan. Alternatively, DOE guarantees loans provided by commercial lenders. DOE’s

guarantee amount is capped at 80% of principal for a given loan, thus requiring the lender

to hold at least 20% of the credit exposure.

Collectively, tax and credit incentives help to reduce the cost of power from different

generation technologies, thus enhancing their competitiveness against other power sources.

Tax credits, accelerated depreciation, and credit support enable significant cost reductions

when applied together, and enable power to be purchased by customers at a lower price.

The combination of tax credits, accelerated depreciation, and credit support is estimated to

reduce the cost of power by 48% for solar power, and 35% for wind.

ES.3 COSTS AND ECONOMIC BENEFITS OF SUPPORT PROGRAMS FOR RENEWABLES

Growth in the solar and wind power industries was supported by a combination of Federal

spending on supply-side incentives (tax incentives, credit support, and R&D), and demand

mandates by the Federal and state governments. To quantify the cost of incentive programs,

this report examines the revenue loss associated with tax incentives, the appropriated credit

subsidy associated with credit incentives, and the direct spending associated with research

and development initiatives. This report does not attempt to quantify the cost of demand

mandates implemented at the Federal and state level.

As illustrated in Exhibit ES-1, based on a review of incentives for solar and wind from 2005

to 2015, it is estimated that the Federal government spent $51.2 billion, with tax incentives

accounting for 90% of the total.

EXAMINATION OF FEDERAL FINANCIAL ASSISTANCE IN THE RENEWABLE ENERGY MARKET

P AGE | ES-4

In association with

Exhibit ES-1 Total Incentives for Wind and Solar

2

,

3

ES.3.1 Tax-Based Incentives

The cost of tax-based incentives is defined as the amount of tax revenue the Federal

government abates through special tax credits and other incentives which reduce tax

obligations. The Federal government spent a total of $45.8 billion on tax incentives for solar

and wind from 2005 to 2015. Of this, production tax credits comprised 46.4%, or $21.3 billion.

Spending on 1603 Cash Grants comprised $20.4 billion, or 44.5% of the total. This was

followed by investment tax credits at $2.4 billion, or $5.13% of the total; it is worth noting

that 1603 Cash Grants were effectively a substitute for ITCs, so investment-based subsidies

were in fact very large if ITCs and 1603 Cash Grants are considered together. Lastly, MACRS

incentives were worth $1.8 billion, or 3.97% of the total. This is summarized in Exhibit ES-2.

2

Based on Scully Capital analysis discussed throughout this section.

3

Chart shows $51.1 billion instead of $51.2 B of total incentives; slight difference due to rounding.

Tax Incentives $45.8 B

(90%)

Credit Incentives $1.3 B (2%)

R&D Grants $4 B

(8%)

Total Incentives:

$51.2 Billion

EXAMINATION OF FEDERAL FINANCIAL ASSISTANCE IN THE RENEWABLE ENERGY MARKET

P AGE | ES-5

In association with

Exhibit ES-2: Summary of Tax-Based Incentives in 2015 Billions of U.S. Dollars

ES.3.2 Credit-Based Incentives

The Federal government offered significant credit support in the form of loans and loan

guarantees for wind and solar through DOE’s lending authority. As depicted in Exhibit ES-

3, DOE provided $11.7 billion in credit assistance to 3,808 MW of solar and wind projects.

Although the loans supported by DOE totaled $11.7 billion, the appropriated subsidy costs

were only $1.3 billion, reflecting the use of credit subsidy in budgeting.

-

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

(2015 $B)

PTC

1603 Cash Grant

MACRS

ITC

EXAMINATION OF FEDERAL FINANCIAL ASSISTANCE IN THE RENEWABLE ENERGY MARKET

P AGE | ES-6

In association with

Exhibit ES-3: LPO Credit Incentive Spending for Wind and Solar

4

Finally, supplementing the financial support through tax and credit incentives was R&D

spending. R&D investment in solar power totaled $3.2 billion from 2005 to 2015 and totaled

$880 million for wind power over same period.

ES.3.3 Benefits of Incentive Programs

While the Federal government’s $51.2 billion investment in solar and wind represents a large

commitment, the impact on the industry and U.S. generation mix has been significant.

Strong government support resulted in meaningful growth in generation capacity and

power production for solar and wind, and stimulated related employment.

The incentive programs sparked growth in the solar and wind power industries. Deployment

of solar and generation capacity, and the resulting electricity, have grown sharply since 2005.

From 2005 to 2015, solar capacity grew by 77,794 MW and wind capacity grew by 446,548

MW. This also facilitated growth of employment in solar and wind jobs, such that those

industries are expected to provide the two fastest growing occupations through 2026. Both

industries make strong contributions to the wider economy, including stimulating growth in

other sectors and making significant tax payments. Power production has become more

efficient, and costs have fallen, for both technologies.

4

Government Accountability Office, “DOE Loan Programs: Current Estimated Net Costs…,” April 2015.

EXAMINATION OF FEDERAL FINANCIAL ASSISTANCE IN THE RENEWABLE ENERGY MARKET

P AGE | ES-7

In association with

ES.4 APPLICATION TO SMRS

Electric utilities in the United States currently operate in a rapidly evolving market

environment which has challenged conventional notions of how electric power is generated

and delivered to customers, presenting uncertainty for electric utilities facing long-term

investment decisions. Nevertheless, capital will continue to be deployed in power production

assets that can reliably provide energy, capacity, and flexibility. As the nation’s traditional

baseload generation assets, largely consisting of large coal and nuclear power plants, are

phased out, utilities will seek opportunities to replace these assets with more resilient energy

systems that recognize the long-term impacts of distributed energy resources (DERs) while

at the same time provide for safe, reliable, and resilient performance over the long term.

Rising use and affordability of renewables, and significant retirements of coal and nuclear

generation assets raise fundamental questions about what kind of generation is needed on

the grid. While the power market may not require the levels of baseload generation

prevalent decades ago, the grid is not ready to be free of baseload entirely. Furthermore,

the North American Electric Reliability Corporation (NERC) indicated in its 2017 Long-Term

Reliability Assessment that fuel assurance is a significant concern in planning for adequate

reserve margins, especially for markets with high renewable penetration and significant

reliance on natural gas.

5

The current trends in the electric power sector present opportunities for SMR development

as a flexible, carbon-free baseload generation resource which can be built on a smaller scale

than traditional nuclear plants. In order to capture the benefits, as a new and complex

technology, SMRs will have to address several challenges to commercial deployment,

including:

• Development of Manufacturing Ecosystem;

• Licensing Risk;

• Development Timeline;

• First of a Kind (FOAK) Costs; and

• Uncertainty in Long-Term Energy Markets.

Federal financial assistance can help address these challenges. Tax and credit incentives

clearly contribute to significant reductions in the cost of electricity while demand mandates

assure off-take at predictable prices. Such incentives could also potentially be applied to

5

North American Electric Reliability Corporation, “2017 Long-Term Reliability Assessment,” March 2018.

EXAMINATION OF FEDERAL FINANCIAL ASSISTANCE IN THE RENEWABLE ENERGY MARKET

P AGE | ES-8

In association with

support the development of SMRs. Exhibit ES-4 illustrates SMR Start’s estimate of the

potential savings to an SMR’s LCOE based on the application of tax and credit incentives.

Exhibit ES-4: LCOE of SMR

6

SMR Start estimates that allowing SMRs to receive PTCs would reduce the cost of power

by just under 1¢ per kWh. Credit incentives (loan guarantees) are estimated to reduce the

cost of power by another 0.3¢. State and local tax incentives, such as sales and use tax

exemptions and property tax abatements, could further reduce costs by 0.5¢. Altogether,

these would reduce the cost of power by 22%.

7

To meaningfully impact commercial deployment, these incentives would need to be applied

to several SMRs in combination with demand mandates to assure off-take. Construction of

6 GW of SMR capacity by 2035 would comprise about 5% of total capacity additions through

that year. This would amount to 15 SMR projects with capacity of 400 MW each. The total

cost to the Federal government of supporting 15 such SMR project with PTCs and DOE credit

6

SMR Start, “The Economics of Small Modular Reactors,” September 14, 2017.

7

IBID

SMR LCOE

After

Incentives

Cost of Power (¢/kWh)

SMR

Baseline

LCOE

7.8¢

0.9¢

0.5¢

0.3¢

PTC

State and

Local Tax

Incentives

DOE

Credit

Support

6.1¢

EXAMINATION OF FEDERAL FINANCIAL ASSISTANCE IN THE RENEWABLE ENERGY MARKET

P AGE | ES-9

In association with

support is estimated to cost approximately $10 billion. While this level of support is

significant relative to the capacity deployed, the high capacity factors and long operating

lives of SMRs support an attractive return on the government’s investment. Specifically, the

$10 billion assistance estimate equates to approximately $0.0034/kWh. By comparison, the

investments in wind and solar equaled approximately $0.0108/kWh.

8

This comparison is

presented in Exhibit ES-5.

Exhibit ES-5: Investment to Support SMR Generation

As illustrated above, when viewed in terms of spending per unit of power produced (cents

per kWh), the proposed support for SMRs compares favorably against the historic support

for solar or wind. This is because SMRs are expected to realize capacity factors of 92.1% or

above and have very long operating lives. Nevertheless, important questions remain

regarding the cost of commercially deploying SMRs and whether 6 GW of induced capacity

8

Scully Capital calculations, see Appendix C.

EXAMINATION OF FEDERAL FINANCIAL ASSISTANCE IN THE RENEWABLE ENERGY MARKET

P AGE | ES-10

In association with

would be sufficient to develop the industrial capabilities necessary to support the industry

over the long-term.

ES.5 NEXT STEPS

Given recent retirements of coal and conventional nuclear plants, and significant retirements

expected in coming years, an opportunity exists for SMRs to enter the market and

meaningfully contribute to the country’s need for energy security and energy resilience.

However, SMRs face significant challenges in commercial deployment, including the need

to develop a manufacturing ecosystem for a new technology, significant work remaining to

license and develop a working generation facility, and costs which may be high relative to

other energy sources in the competitive and quickly evolving power markets.

The success of Federal financial incentives for renewables presents a promising model of

financial support for power project development, which could be applied to other innovative

power technologies, including SMRs. Federal expenditure for SMRs could be impactful even

if on a smaller scale than the $51 billion spent on solar and wind from 2005 to 2015.

The Federal government has made progress supporting SMR development with Federal

incentives. DOE currently has an open solicitation for loan guarantees for nuclear projects

including SMRs.

9

Congress also voted to extend nuclear PTCs passed the planned expiration

in 2020, which would enable projects completed after 2020 to benefit from them.

10

While

those actions could be helpful for SMRs, other steps could further help SMRs to

commercialization:

• Examine Potential Market Associated with SMRs: In order to establish a business case

for Federal financial assistance, the potential of SMRs as a source of power generation

and as a commercial enterprise should be analyzed, and if possible, quantified. This

should include consideration of financial, legal, regulatory, and technical issues

related to SMRs’ integration into the power system, including consideration of the

entire value chain, cost competitiveness, and other matters. The objective of this

undertaking would be fourfold:

‒

Confirm the suitability of SMRs to address the baseload power replacements

which will be driven by coal and conventional nuclear retirements;

‒

Identify how the SMR supply chain will need to develop in order to achieve

the n

th

-of-a-kind cost targets;

9

https://www.energy.gov/lpo/advanced-nuclear-energy-projects-solicitation

10

https://www.nei.org/news/2018/congress-passes-nuclear-production-tax-credit

EXAMINATION OF FEDERAL FINANCIAL ASSISTANCE IN THE RENEWABLE ENERGY MARKET

P AGE | ES-11

In association with

‒

Validate or refine the 6 GW estimate of SMR commercial deployments

required to establish SMRs as a viable baseload option; and

‒

Develop an order of magnitude estimate of technology export value based on

the U.S. experience with conventional nuclear power plants.

• Create Project-Level Business Case: Analyses of the impact of financial incentives have

focused on LCOE, which is a useful metric for comparing costs of different

technologies or considering an indicative project. To further DOE’s understanding, a

project-level business case that contemplates the site-specific costs, load profiles, and

financial structure is warranted. This feasibility analysis would seek to identify the cost

of service of a proposed SMR and would measure the impact of incentives and the

uncertainties that could increase costs, identify key risks and mitigants, and integrate

financial, legal, regulatory, and technical considerations.

While the analysis could draw upon conceptual design data, site-specific costs,

infrastructure requirements and customers would be examined with the objective of

refining DOE’s understanding of the financial feasibility of one or two “first movers.”

Additionally, the analysis would consider the host utility’s ownership, the proposed

credit structure of the project and the economic objectives and constraints of the

host utility’s customer base. This effort would result is assessment the opportunities

and challenges to SMR commercial deployment and would inform the design of

incentives around specific market conditions and other constraints.

• Identify Obstacles that Require Legislative Action: Enhancing Federal support for SMRs

will require Congress to pass legislation. To facilitate the eventual enactment of new

incentives, key initiatives should be identified for development into law. This would

be informed by the findings of the project-level business case analysis, and could

focus on matters such as identifying appropriate existing legal authorities for

supporting Federal power purchase agreements, finding ways to modify or extend

existing incentives, creating budget scoring alternatives or developing roadmaps for

implementing new programs or legislation.

EXAMINATION OF FEDERAL FINANCIAL ASSISTANCE IN THE RENEWABLE ENERGY MARKET

P AGE | 1

In association with

INTRODUCTION

In numerous sectors of the economy, the Federal government has utilized financial

incentives to mobilize private sector investment and advance policy objectives. The

renewable energy sector provides a highly relevant example of how financial assistance in

the form of demand mandates and financial incentives can spur industry development.

Today, renewable energy generation is transforming the power sector in many states,

challenging traditional utility business models, and in many cases displacing traditional

baseload sources during hours of peak generation.

Over the next 20 years, the United States is expected to encounter challenges in providing

adequate supply of baseload power as some of the country’s coal-fired power plants and

nuclear generation stations are retired. The estimated electricity output from coal and to a

limited extent nuclear sources is expected to decline significantly due to regulatory drivers,

changes in state and Federal energy policy and competition from low cost sources such as

natural gas.

11

Further, integration of growing power supply from intermittent renewable

power sources requires adequate supply of steady power to balance renewables when their

power production is lower due to variation in intermittent resources.

12

The development and construction of new baseload power plants, like Small Modular

Reactors (SMRs), represents a highly uncertain endeavor. Investment in additional

generation requires consideration of customers’ long-term demand for power, existing and

future regulations, competing alternatives, and changes in market dynamics. Despite the

uncertainties, large-scale baseload power plants will need to be developed, designed, and

constructed to replace an

aging fleet consisting largely of coal and nuclear generation.

These challenges are likely to remain in the near term. However, government financial

incentives could be utilized to encourage investment in targeted sectors and technologies.

Previous analyses sponsored by the Department of Energy (DOE) have examined how the

Federal government can support SMR investment in its capacity as power purchaser.

13,14

Government incentives can take other forms such as direct grants, tax incentives, credit

incentives, and demand mandates. This report introduces these incentives, discusses how

11

U.S. Energy Information, “Annual Energy Outlook 2018: Table: Electricity Generating Capacity,”

https://www.eia.gov/outlooks/aeo/data/browser/#/?id=9-AEO2018&cases=ref2018&sourcekey=0, referenced April 27, 2018. Cited data is

for the Reference Case.

12

Department of Energy, “Staff Report on Electricity Markets and Reliability,” August 2017.

13

Kutak Rock, LLP, and Scully Capital Services Inc., “Small Modular Reactors: Adding to Resilience at Federal Facilities,” published by U.S.

Department of Energy, December 2017.

14

Kutak Rock, LLP, and Scully Capital Services Inc., “Purchasing Power Produced by Small Modular Reactors: Federal Agency Options,”

published by U.S. Department of Energy, January 2017.

EXAMINATION OF FEDERAL FINANCIAL ASSISTANCE IN THE RENEWABLE ENERGY MARKET

P AGE | 2

In association with

they have been utilized over the past decade to stimulate investment in the renewable

energy sector, provides data on their cost and on their effectiveness in meeting policy

objectives, and offers observations on how SMRs could benefit from similar forms of

government support.

This report is organized as follows:

• Overview of Mandates and Incentives for Renewable Energy: This chapter provides a

comprehensive overview of the multi-pronged strategy employed at the Federal and

state level to drive the renewable energy market.

• Project Level Effects of Financial Incentives: This chapter describes the purpose and

structure of financial incentives. Also, this section explores how incentives reduce the

cost of power, and estimates the effect of Federal tax and credit incentives on

indicative solar and wind power projects in terms of the levelized cost of electricity

(LCOE).

• Costs and Economic Benefits of Support Programs for Renewables: This chapter

describes spending on renewable support and growth in installed renewable power

capacity since 2005, and the resulting benefits in terms of power outputs, jobs, and

other areas.

• Application to SMRs: This chapter provides an overview of current U.S. electric market

conditions and how it has evolved over time, describes how SMRs can address

emerging concerns in the power sector, and proposes models of incentives to

support SMR commercial deployment.

• Next Steps for Supporting Commercial Deployment of SMRs: This chapter provides

recommendations for developing and implementing incentive programs for SMR

commercialization.

EXAMINATION OF FEDERAL FINANCIAL ASSISTANCE IN THE RENEWABLE ENERGY MARKET

P AGE | 3

In association with

OVERVIEW OF MANDATES AND

INCENTIVES FOR RENEWABLE ENERGY

For decades, multiple Presidential Administrations attempted to promote the use of

renewable energy such as solar and wind. Such use had been limited by the high cost of

renewables due to the lack of demand and technology development and the failure of the

commercial market to accept the technologies.

While several Presidents were able to establish renewable energy goals and policies, it was

not until the period following the passage of the Energy Policy Act of 2005 (EPAct or the

Act) that significant renewable penetration was achieved in the U.S. power sector. This

market penetration can be attributed to several factors:

• State-imposed standards to increase the use of renewable energy (Renewable

Portfolio Standards or RPS);

• Federal policies, mandates, and incentives enacted by EPAct and subsequent

legislation; and

• Executive Orders and Agency actions supporting the purchase of renewable energy.

Collectively, these measures created a multipronged approach that encouraged utilities to

enter into long-term renewable power purchase agreements with renewable project

developers, drove down the cost of renewable energy through state and Federal tax and

credit incentives, and harnessed the purchasing power of the Federal government. These

actions increased the demand for renewable energy, while at the same time lowered costs

through financial incentives, increasing the supply of competitive renewable power. The

Federal government has also supported research and development (R&D) for renewable

generation technologies.

This section details the state and Federal incentives that supported the development of

renewable energy projects during the period following the passage of EPAct and highlights

how these policies worked together to significantly expand renewables in the U.S. energy

markets.

STATE RENEWABLE PORTFOLIO STANDARDS

As states have become increasingly concerned about climate change and reducing pollution,

they have enacted Renewable Portfolio Standards (RPS). An RPS is a requirement that retail

electricity suppliers procure a certain minimum quantity of eligible renewable energy or

capacity, measured in either absolute units (kWh or kW), or as a percentage share of retail

EXAMINATION OF FEDERAL FINANCIAL ASSISTANCE IN THE RENEWABLE ENERGY MARKET

P AGE | 4

In association with

sales. RPS policies are generally designed to maintain and/or increase the contribution of

renewable energy to the electricity supply mix. RPS programs often utilize tradable

renewable energy certificates (RECs) to increase the flexibility and reduce the cost of

compliance with the purchase mandate, and to facilitate a purely financial product that can

be traded separately from the underlying electricity generation. These actions have created

a relatively stable market for the purchase and sale of RECs, enhancing their value in a

number of state markets. REC transactions create a supplemental revenue stream for

renewable generators and allow retail suppliers to demonstrate compliance with the RPS by

purchasing RECs in lieu of directly purchasing renewable electricity.

The concept of RPS was developed in California in 1995, although not implemented there

until 2003; other states began enacting RPS in the late 1990s. As of November 2015, 29

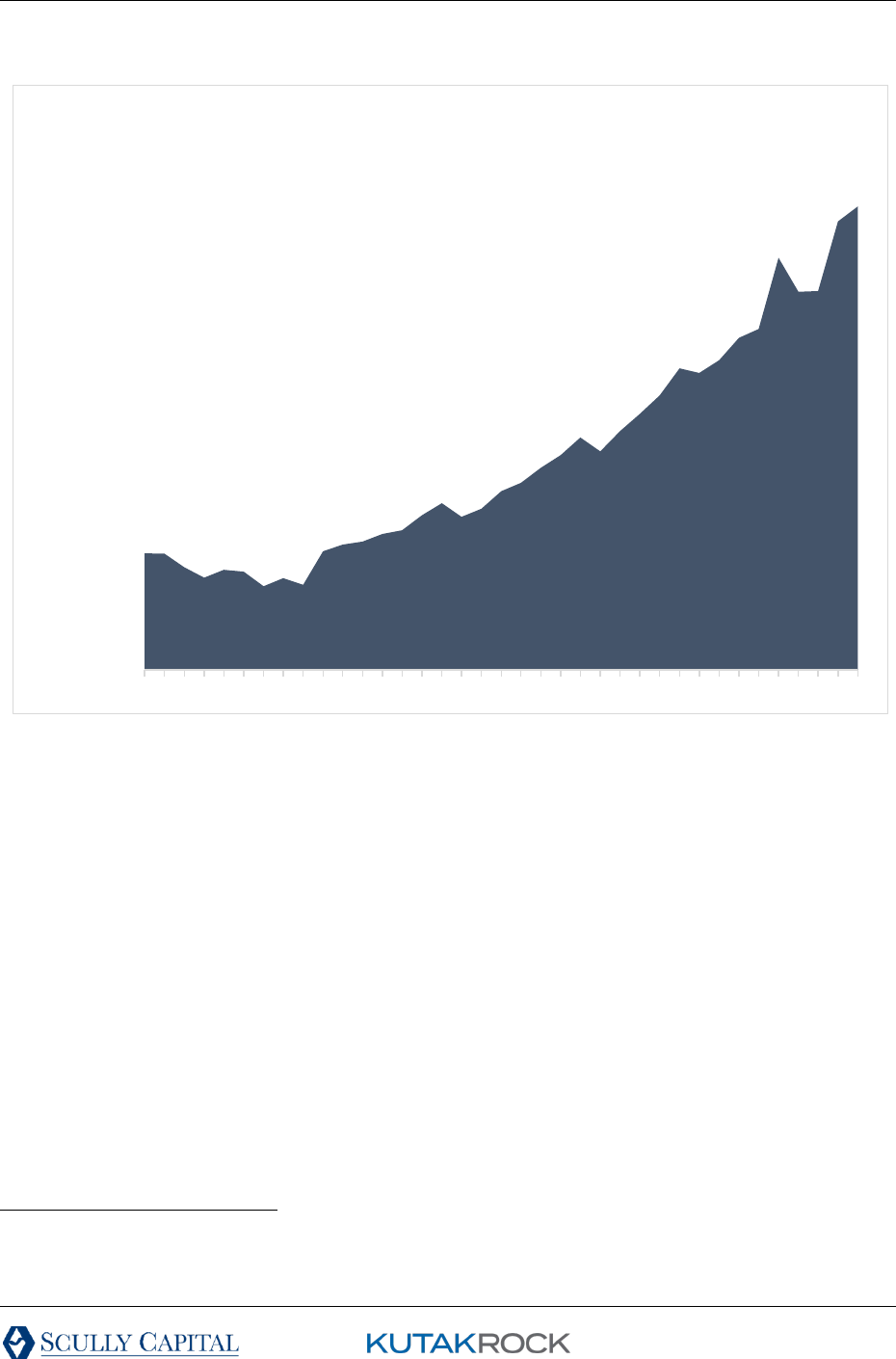

states and the District of Columbia have RPS mandates, as shown in Exhibit 2-1.

Exhibit 2-1: States with RPS

RPS mandates created strong demand for renewable power. It is estimated that 58% of all

renewable capacity in the U.S. installed from 1998 to 2014 is being used to meet RPS targets

(excluding hydropower).

15

RPS mandates require that at least 8% of the U.S. power supply

15

Wiser et al, “A Retrospective Analysis of the Benefits and Impacts of U.S. Renewable Portfolio Standards,” published by National

Renewable Energy Laboratory, January 2016.

EXAMINATION OF FEDERAL FINANCIAL ASSISTANCE IN THE RENEWABLE ENERGY MARKET

P AGE | 5

In association with

will be met by renewables in 2025, equivalent to 106 GW of capacity.

16

From 2010-2013,

wholesale power buyers (generally utilities) tended to pay a premium (under long-term

power purchase agreements) over prevailing “brown power” rates, as high as 4.8¢ per kWh

for some utilities, to purchase renewables for RPS purposes over other generation options.

The incremental cost of complying with RPS, net of the avoided cost of alternative

generation, ranged from 2% to 4% of retail rates in eight states, and was below 2% in 17

states.

17

ENERGY POLICY ACT OF 2005

The Federal government’s effort to increase the use of energy from renewable sources

began in earnest with the requirements included in EPAct.

18

Given high oil and natural gas

prices that prevailed around 2001, the Bush Administration supported policies which

targeted the development of a long-term, comprehensive strategy to lessen the impact of

energy price volatility and supply uncertainty. This led to several years of policy discussion

around “energy security” as a national priority. In 2005, the U.S. Congress enacted the EPAct,

which reflected the Administration’s goals by creating programs and policies aimed at

increasing and diversifying domestic energy production. EPAct included key provisions to

help diversify domestic energy production through the development of new sources of fuel

and electricity supply. This included incentives for nuclear power plants, coal, and

renewables.

For renewable energy, EPAct included financial incentives, which were later enhanced in

subsequent legislation and demand mandates related to the energy consumption by Federal

facilities. Tax incentives, which are examined in the following section, included production

tax credits, investment tax credits, and accelerated depreciation treatment for qualifying

renewable energy projects. Also, EPAct set specific renewable energy purchase targets for

all Federal agencies:

• 3% of all electricity by 2007;

• 5% by 2010; and

16

Wiser et al, “A Retrospective Analysis of the Benefits and Impacts of U.S. Renewable Portfolio Standards,” published by National

Renewable Energy Laboratory, January 2016.

17

Heeter at al, “A Survey of State-Level Cost and Benefit Estimates of Renewable Portfolio Standards,” published by National Renewable

Energy Laboratory, May 2014.

18

Energy Policy Act of 2005

, Pub.L. 109-58, Aug. 8, 2005, 42 U.S.C. §§ 13201, et. seq.

EXAMINATION OF FEDERAL FINANCIAL ASSISTANCE IN THE RENEWABLE ENERGY MARKET

P AGE | 6

In association with

• 7.5% by 2013.

19

The Administrator of General Services (GSA) was required to establish a photovoltaic

purchasing program for the acquisition and installation of solar electric systems for new and

existing buildings.

20

DOE was authorized to establish a renewable energy rebate for the

installation of renewable energy systems in residential and small business properties.

21

And

the Secretary of Interior (DOI) was directed to approve non-hydropower renewable energy

projects located on public lands with a generation capacity of at least 10,000 megawatts of

electricity by 2015.

22

The goals included in EPAct were intensified by Congress as applied to the Department of

Defense (DoD) in the 2007 National Defense Authorization Act (NDAA), which required DoD

to “produce or procure not less than 25 percent of the total quantity of electric energy it

consumes within its facilities and in its activities during fiscal year 2025 and each fiscal year

thereafter from renewable energy sources” and “to produce or procure electric energy from

renewable energy sources whenever the use of such renewable energy sources is consistent

with the energy performance goals and energy performance plan for the Department.”

23

Section 1703 of Title XVII of EPAct of 2005 created the DOE’s Loan Guarantee Program.

Under Section 1703, DOE is authorized to issue loan guarantees for projects with high

technology risks that "avoid, reduce or sequester air pollutants or anthropogenic emissions

of greenhouse gases; and employ new or significantly improved technologies as compared

to commercial technologies in service in the United States at the time the guarantee is

issued." Loan guarantees are intended to encourage early commercial use of new or

significantly improved technologies in energy projects. The loan guarantee program

generally does not support research and development projects. During the Obama

Administration, DOE issued new supplemental guidance for Renewable Energy and Efficient

Energy (REEE) projects that added $500 million of loan guarantee authority, making the total

available approximately $4.5 billion.

The loan guarantee program was reauthorized and revised by the American Recovery and

Reinvestment Act (ARRA) of 2009 by adding Section 1705 to EPAct. The 1705 Program was

retired in September 2011, and loan guarantees are no longer available under that authority.

19

Section 203 of EPAct, 42 U.S.C. § 15852.

20

Section 204 of EPAct, 40 U.S.C. § 3177.

21

Section 206(c) of EPAct, 42 U.S.C. § 15853.

22

Section 211 of EPAct.

23

National Defense Authorization Act of 2007

, October 17, 2006, Pub.L. 109-364, § 2852.

EXAMINATION OF FEDERAL FINANCIAL ASSISTANCE IN THE RENEWABLE ENERGY MARKET

P AGE | 7

In association with

DOE, however, still has authority to issue loan guarantees under the old Section 1703

Program.

RECOVERY ACT BOOST TO FUNDING RENEWABLE ENERGY PROJECTS

Nearly 10% of the ARRA

24

, which included over $787 billion in economic stimulus measures,

focused on funding and tax credits for green-energy related projects including renewables,

energy efficiency, transmission, and weatherization. No funding was provided for nuclear

related programs.

In 2009, ARRA significantly increased Federal investment and spending on renewable

energy. ARRA included $16.8 billion for the DOE’s Office of Energy Efficiency and Renewable

Energy (EERE). The funding was a nearly tenfold increase for EERE, which received $1.7 billion

in fiscal year 2008. The bulk of the new EERE funding supported direct grants and rebates

while $2.5 billion supported EERE's applied research, development, and deployment

activities, mainly for renewable technologies.

25

ARRA also provided $3.2 billion in block grants to assist local governments in implementing

energy efficiency and conservation programs authorized under subtitle E of title V of the

Energy Independence and Security Act of 2007

26

. These funds could be used for a number

of activities, including establishing financial incentive programs for energy efficiency

improvements (e.g., loan programs, rebate programs, waive permit fees); developing,

implementing, or installing on or in any government building onsite renewable energy

technology that generates electricity from renewable resources (solar and wind energy, fuel

cells, and biomass); implementing energy distribution technologies; and

purchasing/implementing technologies to reduce and capture methane and other

greenhouse gases generated by landfills or similar sources.

ARRA included a $3.1 billion appropriation to DOE’s State Energy Program (SEP) authorized

under part D of title III of the Energy Policy and Conservation Act (42 U.S.C. 6321). SEP dollars

are used to provide grants and funding to state energy offices for energy efficiency and

renewable energy programs. The Act also appropriated $6 billion for the cost of guaranteed

loans authorized by section 1705 of the Energy Policy Act of 2005, as noted above. The Act

authorized the DOE Loan Guarantee Program for projects that involved renewable energy,

electric transmission, or leading-edge biofuel technologies. The $6 billion in appropriated

funds was expected to support more than $60 billion in loans for these projects.

24

Pub. L. 111-5, February 17, 2009; 123 Stat. 115.

25

Included in the $2.5 billion were $800 million for projects related to biomass and $400 million for geothermal activities and projects.

26

42 U.S.C. 17151, et seq.

EXAMINATION OF FEDERAL FINANCIAL ASSISTANCE IN THE RENEWABLE ENERGY MARKET

P AGE | 8

In association with

Through ARRA, Congress provided $280 million for the military departments, of which $100

million was for energy conservation and alternative energy projects. $120 million was

allocated for the Energy Conservation Investment Program (ECIP). ECIP improves the energy

and water efficiency of existing Military Services' facilities, promoting energy conservation

and investment in renewable energy resources including wind, solar, geothermal, waste-to-

energy, and biomass at U.S. military installations.

In addition to these direct appropriations, ARRA also provided tax incentives supportive of

renewable energy uses. For example, the creation of a 30% tax credit for certain investments

with respect to qualifying advanced energy products, including manufacturing facilities for

the production of renewable energy products, electric grids to support the transmission of

intermittent sources of renewable energy, and property designed to refine or blend

renewable fuels or to produce energy conservation technologies. ARRA also extended and

expanded credits available to qualified facilities producing energy from renewable resources,

credits worth approximately $13 billion. Income tax credits for the production of electricity

from qualified energy resources were also included. The qualified energy resources were

comprised of wind, closed loop biomass, open loop biomass, geothermal energy, solar

energy, small irrigation power, municipal solid waste, qualified hydropower production, and

marine and hydrokinetic renewable energy.

ARRA also provided incentives to residential energy users by extending a credit of 30% for

residential solar electric, solar water heating, small wind energy and geothermal heat pump

property expenditures, and removing previous caps on residential solar electric, solar water

heating, small wind energy, and geothermal heat pump property expenditures.

ENERGY INDEPENDENCE AND SECURITY ACT OF 2007

The Energy Independence and Security Act of 2007 (EISA) built on many of the policy

objectives and goals included in EPAct.

27

For example, Section 431 established new energy

reduction goals for Federal facilities, increasing each year up to 30% reduction by 2015.

Section 432 established energy management scorecards for Federal agencies and required

metering and other evaluative tools in order to identify and implement energy and water

efficiency projects, and to establish benchmarks for all metered buildings in the Federal

inventory. Section 433 required all new Federal buildings, or buildings undergoing major

modernizations (those requiring GSA to submit a prospectus to Congress or over $2.5

million) to reduce fossil fuel use compared to a similar building use in FY 2003. The

percentage reduction in fossil fuel use was set at 55% for 2010 and increased to 100% by

27

Energy Independence and Security Act of 2007. Pub. L. No. 110-140. 121 Stat. 1492 (2007).

EXAMINATION OF FEDERAL FINANCIAL ASSISTANCE IN THE RENEWABLE ENERGY MARKET

P AGE | 9

In association with

2030. Within 3 years of enactment of EISA, as provided in Section 435, Federal agencies

were prohibited from executing any lease with the private sector for space that had not

earned an EnergyStar label. Title V of EISA included a number of provisions to encourage

the use of ESPCs, which had been authorized in EPAct, by addressing policy or procedural

obstacles that had been encountered by Federal agencies in implementing the authority.

EXECUTIVE ORDERS ON RENEWABLE ENERGY USE BY FEDERAL AGENCIES

President Bush, by Executive Order (E.O.) in 2007, required Federal agencies to reduce their

energy usage by 30% by 2015, and ensure that at least half of their renewable goals under

EPAct were achieved using new renewable sources, located on Federal agency property to

the extent feasible.

28

Later that same year, Congress passed the Energy Independence and

Security Act (EISA), which required all new Federal buildings and all Federal buildings

undergoing major renovation to reduce fossil fuel-generated energy consumption, as

compared to 2003 usage by similar buildings, by 55% by 2010, 65% by 2015, 80% by 2020,

90% by 2025, and 100% by 2030.

29

Federal agencies were also required, where lifecycle

cost-effective, as compared to other reasonably available technologies, to ensure that not

less than 30% of the hot water demand for each new Federal building or Federal building

undergoing a major renovation be met through the installation and use of solar hot water

heaters.

30

President Bush also signed E.O. 13514, Federal Leadership in Environmental, Energy and

Economic Performance, which encouraged Federal agencies to increase the use of

renewable energy and to implement renewable energy generation projects on agency

property.

31

Following up on that executive order, President Obama issued a Presidential

Memorandum in 2011, requiring Federal agencies to implement all energy conservation

measures in Federal buildings with a payback time of less than 10 years.

32

President Obama

also established a 2 year goal for all Federal agencies to enter into a minimum of $2 billion

in performance-based contracts, primarily through the ESPC and UESC contracts that had

been authorized in EPAct.

28

E.O. 13423, January 26, 2007.

29

Energy Information and Security Act

, Pub.L. 110-140, December 19, 2007, Section 433, 42 U.S.C. § 6834(a)(3).

30

Section 523 of EISA, 42 U.S.C. 6834(a)(3)(A)(iii).

31

E.O. 13514, October 8, 2009, Section 2(a)(ii) and (f).

32

Presidential Memorandum,

Implementation of Energy Savings Projects and Performance-Based Contracting for Energy Savings

,

December 2, 2011.

EXAMINATION OF FEDERAL FINANCIAL ASSISTANCE IN THE RENEWABLE ENERGY MARKET

P AGE | 10

In association with

President Obama, on December 5, 2013, signed a Presidential Memorandum directing the

Federal government to consume 20% of its electricity from renewable sources by 2020, more

than double the then current level of about 7% renewable energy use.

33

The Presidential

Memorandum implemented the goal the President outlined in his June 2013 Climate Action

Plan that challenged Federal agencies to more than double their renewable electricity

consumption by 2020.

34

As part of this effort, agencies were encouraged to identify formerly

contaminated lands, landfills, and mine sites to target for renewable energy projects,

providing valuable opportunities to return those lands to productive use. To improve

agencies' ability to manage energy consumption and reduce costs, the Memorandum directs

them to use Green Button, a tool developed by industry in response to a White House call-

to-action that provides utility customers easy and secure access to their energy usage

information in a consumer-friendly format.

President Obama then doubled the original $2 billion goal for performance-based

contracting by the Federal agencies to $4 billion total.

35

In 2015, President Obama launched the Clean Energy Investment Initiative through DOE.

36

The initiative set a goal of catalyzing $2 billion in private sector investment in solutions to

climate change, particularly through the development of low-carbon energy technologies.

By June of that same year, the President announced that the objective had already reached

more than $4 billion in commitments, over double the initial goal.

37

Before leaving office,

President Obama announced that the goal had been exceeded as a result of Federal agency

initiatives.

38

DEPARTMENT OF DEFENSE IMPLEMENTATION OF RENEWABLE ENERGY GOALS

In addition to goals established by statute and executive order, additional renewable energy

goals have been established by Federal agency policies. For example, in 2012, President

Obama directed DoD to install 3 GWs of renewable energy capacity on or around its bases

by 2025. This directive was built on a commitment President Obama made during the State

33

Presidential Memorandum,

Federal Leadership on Energy Management

, December 5, 2013.

34

https://obamawhitehouse.archives.gov/sites/default/files/image/president27sclimateactionplan.pdf

35

See, https://obamawhitehouse.archives.gov/the-press-office/2014/05/09/fact-sheet-president-obama-announces-commitments-and-

executive-actions-a; https://obamawhitehouse.archives.gov/blog/2014/05/09/leading-example-reduce-carbon-pollution-and-waste-

less-energy

36

Presidential Memoranda,

37

Fact Sheet: Obama Administration Announces More Than $4 billion in Private Sector Commitments and Executive Actions to Scale up

Investment in Clean Energy Innovation

, June 16, 2015.

38

https://obamawhitehouse.archives.gov/blog/2016/12/28/Federal-government-exceeds-goal-renewable-energy-and-energy-efficiency-

investments

EXAMINATION OF FEDERAL FINANCIAL ASSISTANCE IN THE RENEWABLE ENERGY MARKET

P AGE | 11

In association with

of the Union that year to develop 1 GW of renewable energy on Navy installations by 2020.

As a result, the Air Force established a goal of obtaining 1 GW by 2016 and the Army set a

goal of obtaining 1 GW of capacity by 2025.

39

In order to implement these renewable energy goals, DoD’s Office of the Assistant Secretary

of Operational Energy Plans and Programs was established to coordinate energy issues in

2010. In 2011, DoD published its Operational Energy Strategy to set the overall direction for

operational energy security for the agency.

40

DoD and DOE published a Memorandum of

Understanding (MOU) in July 2010, to facilitate cooperation to accelerate the research,

development, and deployment of energy efficiency and renewable energy technologies.

41

Each of the services also established new energy offices in order to carry out the renewable

energy objectives. In 2009, the Army issued the Army Energy Security Implementation

Strategy, which requires at least five installations meet “net-zero” energy goals by 2020 and

deploy 1 GW of renewable energy on their installations by 2025.

42

In 2011, the Secretary of

the Army established the Energy Initiatives Office Task Force (EITF) as a part of the Office of

the Assistant Secretary of the Army for Installations, Energy and Environment (ASA IE&E).

The EITF served as the central managing office for the development of large-scale Army

renewable energy projects intended to help the Army achieve the previously established

goals. In 2014 the EITF became an enduring organization, the Office of Energy Initiatives

(OEI), which now serves as the central management office for implementing large-scale

renewable and alternative energy projects.

The Deputy Assistant Secretary of the Navy (Energy) office was established in March 2010,

in order to develop and oversee Department of the Navy policy on matters pertaining to

operational and shore energy initiatives for the Secretary of the Navy. In 2012, the Navy

issued its Strategy for Renewable Energy to guide the Department of the Navy in

accomplishing two of the energy goals established in 2009: to obtain half of the

Department’s energy from alternative sources; and to produce at least half the shore-based

energy requirements from renewable sources, such as solar, wind, and geothermal by

2020.

43

39

See https://obamawhitehouse.archives.gov/the-press-office/2012/04/11/fact-sheet-obama-administration-announces-additional-

steps-increase-ener

40

The 2011 Report, and annual reports thereafter, can be found at https://www.acq.osd.mil/eie/OE/OE_library.html

41

See https://www.acq.osd.mil/dpap/cpic/cp/docs/Memorandum_of_Agreement_with_DoE.pdf

42

http://www.asaie.army.mil/Public/Partnerships/doc/AESIS_13JAN09_Approved%204-03-09.pdf

43

http://www.secnav.navy.mil/eie/Documents/DoNStrategyforRenewableEnergy.pdf

EXAMINATION OF FEDERAL FINANCIAL ASSISTANCE IN THE RENEWABLE ENERGY MARKET

P AGE | 12

In association with

In May 2010, the Air Force published its Air Force Energy Plan with the vision: To “make

energy a consideration in all we do.”

44

Renewable energy initiatives, as well as other energy

programs, were managed by the Air Force Facility Energy Center. In 2016, the Air Force

established the Air Force Office of Energy Assurance (OEA), which develops an integrated

facility energy portfolio and manages the progression of all energy initiatives for the service.

Also in 2016, the Air Force and the Army signed an interagency agreement to partner and

share resources in pursuing the fruition of their energy initiatives and renewable energy

goals.

45

In addition to the goal of producing 1 GW of renewable energy to support on-site

capacity by 2016, the Air Force is also pushing toward ensuring all new buildings are

designed to achieve zero-net-energy by 2030, beginning in 2020.

DEPARTMENT OF ENERGY, GENERAL SERVICES ADMINISTRATION AND OTHER FEDERAL

AGENCY IMPLEMENTATION OF GOALS

2.7.1. Department of Energy Initiatives

Even before the creation of the Office of Energy Efficiency & Renewable Energy (EERE) in

1993, DOE had been focused on the development and use of renewable energy and had

launched initiatives in support of renewable energy. After the passage of EPAct in 2005,

DOE created the Solar America Initiative (SAI) in 2006 as part of President Bush’s Advanced

Energy Initiative. The SAI’s goal was to make solar energy cost competitive by 2015.

46

EERE

and the State of Hawaii signed a Memorandum of Understanding in 2008, establishing the

Hawaii Clean Energy Initiative, a long-term partnership designed to transform Hawaii's

energy system to one that uses renewable energy and energy efficient technologies for a

significant portion (60-70%) of its energy needs.

47

In response to the ARRA, DOE created

the Energy Efficiency and Conservation Block Grant Program to provide $3.2 billion in block

grants to cities, communities, states, U.S. territories, and Indian tribes to develop, promote,

implement, and manage energy efficiency and conservation projects.

DOE’s Solar Energy Technology Office (SETO) launched the SunShot Initiative in 2011 with

the objective of making solar electricity costs competitive with other generation sources by

2020, without subsidies.

48

In September 2017, SETO announced the utility-scale solar goal

44

http://www.acc.af.mil/Portals/92/Docs/AFD-100930-035.pdf

45

https://www.army.mil/e2/c/downloads/429902.pdf

46

https://www.nrel.gov/docs/fy07osti/40936.pdf

47

http://www.hawaiicleanenergyinitiative.org/wp-content/uploads/2015/02/HCEI_FactSheet_Feb2017.pdf

48

https://www.energy.gov/eere/solar/articles/doe-pursues-sunshot-initiative-achieve-cost-competitive-solar-energy-2020

EXAMINATION OF FEDERAL FINANCIAL ASSISTANCE IN THE RENEWABLE ENERGY MARKET

P AGE | 13

In association with

had been met three years ahead of schedule.

49

SETO has stated that they will continue to

work to lower the cost of solar energy and has established a goal to halve the cost of solar

energy by 2030, committing up to $82 million in supportive funding to that end.

50

In addition to the SunShot Initiative, DOE also released the National Offshore Wind Strategy

in 2011, a strategic plan for accelerating the responsible deployment of offshore wind energy

in the United States. This publication serves as a blueprint to achieve 54 GW of deployed

offshore wind generating capacity by 2030.

51

The program expected to build from the more

than $90 million provided in ARRA and FY 2009 and FY 2010 appropriations provided to

DOE for wind initiatives. EERE launched the Clean Energy Manufacturing Initiative (CEMI) in

2013, a new DOE initiative focused on growing American manufacturing of clean energy

products and boosting U.S. competitiveness through major improvements in manufacturing

energy productivity.

52

Since initiating the program, DOE has issued $150 million in Advanced

Energy Manufacturing tax credits and supported state energy and economic development

offices to create state strategies for clean energy manufacturing and economic

development. Then in 2016, DOE’s Wind and Water Power Technologies Office released

Hydropower Vision, a roadmap by which U.S. hydropower could grow from 101 GW of

capacity in 2015 to nearly 150 GW by 2050.

53

DOE continues to provide significant support for renewable energy sources and technology.

In fact, DOE Secretary Perry just announced it is providing $105.5 million in funding for

several solar initiatives in partnership with the private sector, funding approximately 70

projects.

54

An additional $20 million is being provided to assist innovative solar technologies

intended to drive down the cost of solar production.

55

DOE also supports other agencies in increasing their acquisition of energy from renewable

sources. For example, the Federal Energy Management Program (FEMP) established the

Renewable Energy Procurement (REP) Program to provide training for Federal employees,

as well as acquisition assistance to Federal contracting offices in the procurement of

renewable energy.

56

49

https://www.energy.gov/articles/energy-department-announces-achievement-sunshot-goal-new-focus-solar-energy-office

50

Ibid.

51

https://www1.eere.energy.gov/wind/pdfs/national_offshore_wind_strategy.pdf

52

https://www.energy.gov/clean-energy-manufacturing-initiative

53

https://www.energy.gov/eere/water/articles/hydropower-vision-new-chapter-america-s-1st-renewable-electricity-source

54

https://www.energy.gov/articles/us-secretary-energy-rick-perry-announces-105-million-new-funding-advance-solar-technologies

55

https://www.energy.gov/articles/department-energy-announces-20-million-new-projects-lower-cost-power-electronics-solar

56

https://www.energy.gov/eere/femp/renewable-energy-procurement-Federal-agencies

EXAMINATION OF FEDERAL FINANCIAL ASSISTANCE IN THE RENEWABLE ENERGY MARKET

P AGE | 14

In association with

2.7.2. General Services Administration Initiatives

ARRA provided $5.55 billion to the General Services Administration (GSA) Federal Buildings

Fund of which no less than $4.5 billion was to be used to convert GSA facilities to High-

Performance Green buildings as defined in P.L. 110-140. An additional $4 million was

provided for the Office of Federal High-Performance Green Buildings, authorized in the

Energy Independence and Security Act of 2007. While this funding was largely targeted at

energy efficiency, this initiative also led to GSA’s commitment to increase its renewable

energy production and procurement by 30% by FY20.

For example, in 2014, GSA awarded a competitive power supply contract to a commercial

wind developer for the purchase of 140 megawatts (MW) of wind energy.

57

The energy will

come from the Walnut Ridge Wind Farm, which is currently in development in northwest

Illinois, and will add more than 500,000 megawatt-hours (MWhs) of electricity to the power

grid annually. The ten-year contract was awarded to MG2 Tribal Energy – a joint venture

between the Mesa Grande Band of Mission Indians, a Federally-recognized Native American

tribe, and Geronimo Energy, a commercial wind developer – and is the largest wind energy

purchase from a single source in Federal contracting history.

GSA has also initiated programs to implement other Administration objections, such as a

Net Zero program to achieve the goal of 100% use of renewable energy by 2030 established

in EISA.

58

2.7.3. Department of Veterans Affairs

In response to the renewable purchase goal of 7.5% of consumed energy by 2013 set for

Federal agencies in EPAct, the Department of Veterans Affairs (VA) actually doubled that

goal for itself to 15%. In order to reach this goal, the VA initiated a number of renewable

energy projects, including a $78 million solar project in Phoenix, AZ, a 455 Kw solar project

in Philadelphia, PA

59

, and both a wind turbine and a ground source heat pump generation

project in St. Cloud, MN.

60

In 2010 alone, the VA awarded $78 million in solar projects

nationwide.

61

In 2011, the VA awarded another $56 million in contracts for solar energy.

62

By

2016, the VA reported that 30% of their facilities’ electrical use came from renewable

sources.

63

57

See, https://www.gsa.gov/node/78816

58

See, https://www.gsa.gov/cdnstatic/RMI_white_paper_-_GSA_NZE-_2015-10-21.pdf

59

http://vabenefitblog.com/the-va-tackles-renewable-energy/

60

https://www.stcloud.va.gov/features/Wind_Turbine.asp

61

https://obamawhitehouse.archives.gov/blog/2010/10/22/leading-example-va-funds-solar-energy-projects-hospitals-clinics-cemeteries

62

https://www.pv-tech.org/news/us_department_of_veterans_affairs_grants_us56.7m_for_solar_installations_on

63

https://www.sustainability.gov/pdfs/va_scorecard_fy2016.pdf

EXAMINATION OF FEDERAL FINANCIAL ASSISTANCE IN THE RENEWABLE ENERGY MARKET

P AGE | 15

In association with

2.7.4. Department of Labor

The Department of Labor (DOL) received $750 million from ARRA for a program of

competitive grants for worker training and placement in high growth and emerging industry

sectors. Within the amount provided, $500 million was designated for projects that prepare

workers for careers in energy efficiency and renewable energy as described in the Green

Jobs Act of 2007. ARRA also appropriated $250 million for the DOL Job Corps Centers, of

which up to $37.5 million was made available for the operational needs of the Job Corps

program, including activities to provide additional training for careers in energy efficiency,

renewable energy, and environmental protection industries.

SUMMARY

Although there had been earlier attempts to promote the use of renewable energy, progress

was slow until the galvanizing impacts of Federal support through mandating the acquisition

and generation of renewable energy by Federal agencies, and Federal tax and credit

incentives to increase the affordability of renewable energy. These initiatives were matched,

and in some cases exceeded, by State programs which also mandated renewable energy

production and use by public utilities, and provided consumers with tax incentives for

renewable purchasing. As discussed in the sections that follow, this multipronged strategy

was effective and the combination of incentives meaningfully impacted the solar and wind

sectors in the United States.

EXAMINATION OF FEDERAL FINANCIAL ASSISTANCE IN THE RENEWABLE ENERGY MARKET

P AGE | 16

In association with

PROJECT LEVEL EFFECTS OF

FINANCIAL INCENTIVES

The financial incentives introduced by EPAct and subsequent legislation addressed several

financing challenges being faced at the time: first, renewable energy projects had a limited

track record of commercial deployment, particularly with the newer technologies being

introduced at the time; and second, for several years the financial markets were recovering

from the 2008-2009 economic downturn, limiting the availability of low cost, long term debt.

The financing tools introduced by the Federal government made renewable energy projects

financially feasible.

This section of the report describes these financial incentives and quantifies the impact of

incentives at the project level. Importantly, many of the financial incentives can be used in

combination, providing a cumulative benefit as reflected in the LCOE. This section is

organized as follows:

• Introduction and Description of Financial Incentives; and

• Project Level Financial Analysis.

For the analysis of financial incentives, solar and wind generation are examined as these

sources of renewable energy posted the largest gains over the period 2005 through 2015.

FINANCIAL INCENTIVES OFFERED TO RENEWABLES SINCE 2005

The financial incentives introduced or extended by EPAct and subsequent legislation can be

broadly categorized into two types: tax-based incentives and credit-based incentives. Tax-

based incentives encourage investment by providing a means of lowering an investor’s

taxable income while credit-based incentives increase the availability of debt capital and/or

lower borrowing cost. Each of these categories is described below.

3.1.1. Tax-Based Incentives

Tax-based incentives offer the benefit of being relatively easy to introduce and administer.

Once enacted, investors will realize the value of tax incentives by claiming credits or

deductions on their tax filings. To convert the benefit of tax incentives to facilitate project

development, project developers often collaborate with specialized financing entities who

have larger income, and thus a larger appetite for tax reductions. These specialized entities

are willing to trade cash “tax equity” for a stream of tax benefits. Tax equity represents a

source of capital for projects qualifying for tax incentives and reduces the amount of funding

required from conventional debt and equity sources. Third-party tax equity investors tend

EXAMINATION OF FEDERAL FINANCIAL ASSISTANCE IN THE RENEWABLE ENERGY MARKET

P AGE | 17

In association with

to be large, sophisticated institutional investors, and in 2016 funded approximately $13 billion

in tax equity investments, largely in the renewable energy sector.

64

The tax incentives utilized in the renewable sector are described below.

Investment Tax Credits (ITCs)

ITCs give a business a tax credit for a specified percentage of capital expenditures for

qualifying energy projects. ITCs are an investment-based subsidy as they provide upfront

financial support for the construction of a project which is expected to deliver a specified

good or service in the future (renewable energy in this case). The ITCs for renewable energy

property were established by EPAct 2005 and then modified by several subsequent laws:

The Energy Improvement and Extension Act of 2008, ARRA, and most recently the

Consolidated Appropriations Act of December 2015. The Tax Cut and Jobs Act of 2017 did

not change the status quo ITC offerings. Projects qualify for ITCs in the year they begin

construction, and receive ITCs when they are placed in service; projects can spread ITC

benefits over multiple years by “carrying forward” the unused amount. From 2005 to 2015,

ITCs were offered in an amount equal to 30% of qualifying investment costs. Since the value

of ITCs for individual projects often exceeds tax obligations, tax equity investors are

commonly used to fully realizing the benefit of ITCs.

Production Tax Credits (PTCs)

PTCs give a taxpaying entity a tax credit for power output, in terms of a fixed dollar amount

per unit of output. A PTC can thus be considered a form of results-based subsidy, in that it

is only paid out when the intended product (renewable energy in this case) is delivered.

65

PTCs have been offered for a specified number of years of production generally less than

the full operational life of power projects; since 2005, PTCs have been offered for eight years

of production for nuclear projects and 10 years for other technologies. PTCs for renewable

energy were first authorized by the Energy Policy Act of 1992, and then have been modified

or extended several times since then, including most recently EPAct 2005, ARRA in 2009, the

American Taxpayer Relief Act of 2012, the Tax Increase Prevention Act of 2014, and the

Consolidated Appropriations Act of 2016.

66

The Tax Cut and Jobs Act of 2017 did not change

the status quo PTC offerings. PTC payments were scaled up to adjust for inflation each year.

64

Tax Equity Update 2017. Bloomberg New Energy Finance. March 7, 2017.

65

Results-based subsidies, also commonly referred to as results-based financing (RBF) in international development, have been used to

support investment in renewables and other infrastructure. https://openknowledge.worldbank.org/handle/10986/17481

66

https://www.awea.org/production-tax-credit

EXAMINATION OF FEDERAL FINANCIAL ASSISTANCE IN THE RENEWABLE ENERGY MARKET

P AGE | 18

In association with

As with the ITCs described previously, power projects often use tax equity financing to realize

the full benefit of PTCs.

Accelerated Depreciation

Accelerated depreciation—formally Modified Accelerated Cost Recovery System (MACRS)—

is a long-standing business tax incentive which is offered to renewable power projects and