2022

WORLD TRADE

REPORT

Climate change and

international trade

What is the World

Trade Report?

The World Trade Report is an

annual publication that aims to

deepen understanding about

trends in trade, trade policy issues

and the multilateral trading

system.

What is the 2022

Report about?

The 2022 World Trade Report

explores the complex interlinkages

between climate change and

international trade, revealing how

international trade and trade rules

can contribute to addressing

climate change.

Find out more

Website: www.wto.org

General enquiries:

enquiries@wto.org

Tel: +41 (0)22 739 51 11

Cover image:

Kamarjani, Bangladesh

Technicians travel with their equipment by rickshaw to install a solar power system at a rural house

built on Kharzanir Chor, an island on the Jamuna River. These islands come and go over a period

of around 10 to 20 years and thus connecting them to the national grid is impractical. However,

a programme of rural electrication is being rolled out using solar panels and batteries installed

at individual homes.

© Laurent Weyl / Argos / Panos Pictures.

Contents

Acknowledgements and disclaimer 2

Abbreviations 4

Foreword by the WTO Director-General 6

Key messages 8

Executive summary 9

A. Introduction 16

1. The next great transformation 18

2. Harnessing the transformative power of trade 20

3. Overview of the report 23

B. The role of trade in adapting to climate change 26

1. Introduction 28

2. Why does climate change adaptation matter? 28

3. International trade and trade policy can support climate change adaptation strategies 34

4. International cooperation is essential to assist countries in adapting to climate change 39

5. Conclusion 47

C. The trade implications of a low-carbon economy 50

1. Introduction 52

2. Achieving a low-carbon economy is an imperative but faces challenges 52

3. A low-carbon economy would change trade patterns and provide new trading opportunities 57

4. International cooperation is essential to achieve a low-carbon economy 65

5. Conclusion 74

D. Carbon pricing and international trade 78

1. Introduction 80

2. Carbon pricing policies can be an important strategy to reduce carbon emissions 80

3. Uncoordinated carbon pricing policies may undermine climate action and lead to trade tensions 85

4. Greater international cooperation is required to advance ambitious carbon pricing policies 90

5. Conclusion 94

E. The decarbonization of international trade 98

1. Introduction 100

2. Accounting for carbon emissions originating from international trade is complex 100

3. International trade affects carbon emissions in multiple ways, both positive and negative 102

4. Reducing trade-related carbon emissions requires greater international cooperation 106

5. Conclusion 112

F. The contribution of trade in environmental goods and services 116

1. Introduction 118

2. There is scope for intensifying trade in environmental goods and services 118

3. Trade in environmental goods and services can contribute to climate change mitigation 123

4. The development and deployment of environmental goods and services require

greater international cooperation 127

5. Conclusion 131

G. Conclusion 134

Opinion pieces

Danae Kyriakopoulou, “Climate inaction: implications for international trade” 30

Gauri Singh, “Green hydrogen requires an appetite for action” 60

Daniel C. Esty, “Trade implications of GHG pricing” 92

Sophie Punte, “Building momentum for zero-emissions freight movement” 110

Bibliography 136

CONTENTS

1

WORLD TRADE REPORT 2022

2

Acknowledgements

The World Trade Report 2022 was prepared under

the general responsibility and guidance of Anabel

González and Jean-Marie Paugam, WTO Deputy

Directors-General, and was coordinated by José-

Antonio Monteiro and Ankai Xu.

Director-General Ngozi Okonjo-Iweala, Chef de

Cabinet Bright Okogu, Yuvan Beejadhur and Trineesh

Biswas from the Office of the Director-General,

Robert Koopman, former Director of the Economic

Research and Statistics Division, and Aik Hoe Lim,

Director of the Trade and Environment Division,

provided valuable advice and guidance.

The lead authors of the report are Marc Bacchetta,

Eddy Bekkers, Cosimo Beverelli, Mateo Ferrero,

Emmanuelle Ganne, Rainer Lanz, José-Antonio

Monteiro, Roberta Piermartini, Daniel Ramos and

Ankai Xu. Other authors are Absar Ali, Antonia

Carzaniga, Svetlana Chobanova, Lory Iunius,

Jonathan Hepburn, Thomas Kräuchi, Juneyoung Lee,

Kathryn Lundquist, Sajal Mathur, Hanh Nguyen, Yves

Renouf, Victor Stolzenburg, Enxhi Tresa, Ayse Nihal

Yilmaz, Khadija Zaidi and Ruosi Zhang.

Other written contributions were provided by Marc

Auboin, Christophe Degain, Peter Donelan, Kartikeya

Garg, Simon Hess, Gergana Kiskinova, Katharina

Laengle, Reto Malacrida, Jeanne Metivier, Marie

Isabelle Pellan, Philippe Pelletier, Rishab Raturi,

Melvin Spreij, Ludivine Tamiotti, Antony Taubman,

Jessyca Van Weelde and Xiaoping Wu.

The following colleagues in the WTO Secretariat

provided valuable written comments on drafts of the

report: Ratnakar Adhikari, Antonia Carzaniga, Mireille

Cossy, Violeta Gonzalez, Ulla Kask, Arne Klau,

Gabrielle Marceau, Clarisse Morgan, Juan Pablo

Moya Hoyos, Marie Isabelle Pellan, Cédric Pene,

Michael Roberts, Stela Rubinova, Melvin Spreij,

Karsten Steinfatt, Sainabou Taal, Antony Taubman,

Cristian Ugarte and Xiaoping Wu. Valuable research

assistance was provided by Francesco Bellelli, Basile

Feller, Tracy Frei, Benjamin Ignoto, Socrates Kraido

Majune and Xiao Yang.

External contributions were received from Daniel

C. Esty (Yale Law School), Danae Kyriakopoulou

(London School of Economics and Political Science),

Sophie Punte (We Mean Business Coalition) and

Gauri Singh (International Renewable Energy

Agency). Background research were also received

from the following WTO Chairs, in coordination

with Mustapha Sadni Jallab and with support from

Sandra Rossier of the Knowledge and Information

Management, Academic Outreach and WTO Chairs

Programme Division: Soledad Aguilar (Latin American

Faculty of Social Sciences), Osman Gulseven (Sultan

Qaboos University), Nada Hazem, Myriam Ramzy and

Chahir Zaki (Cairo University), Sufian Jusoh (National

University of Malaysia), Zhang Lei and Jiang Yue

(University of International Business and Economics),

Thuto Lucy Matobo (National University of Lesotho)

and Boopen Seetanah (University of Mauritius).

The following individuals from outside the WTO

Secretariat also provided useful comments on

early drafts of the report: Rolando Avendano,

Magnus Benzie, Chad Bown, Paul Brenton, Vicky

Chemutai, Brian R. Copeland, Rob Dellink, Klaus

Desmet, Yann Duval, Koffi Aseye Makafui Elitcha,

Robert J. R. Elliott, Daniel C. Esty, Marco Fugazza,

Ian Douglas Gillson, Christian Gollier, Jean-Marie

Grether, Stephane Hallegatte, Katy Harris, Dirk

Heine, Bernard Hoekman, Michael Jakob, Euijin

Jung, Stephen Karingi, Alexander Kasterine, Alexey

Kravchenko, Vesile Kulacoglu, Bruno Lanz, Jia Li,

Jeremy Lucchetti, Tatiana S. Manolova, Nicole

Mathys, Jason McCormack, Nanno Mulder, Hildegunn

Kyvik Nordås, Ralph Ossa, Joseph Pryor, Bernard

Sinclair-Desgagné, Ronald Steenblik, Aleksandar

Stojanov, Shawn W. Tan, Mara Tayag, Robert Teh,

Shunta Yamaguchi and Irina Zodrow.

Gratitude is also due to the speakers of the World

Trade Report 2022 Webinar Series on Trade and

Climate Change for their insightful presentations:

Brian R. Copeland, Klaus Desmet, Katy Harris, Maria

Huge-Brodin, Jenny Minier, Joseph Sarkis, Misato

Sato, Joseph S. Shapiro, Bernard Sinclair-Desgagné

and Tatiana S. Manolova. Special thanks also go to

Isabelle Albrow Gerard, Carole Boureux, Viktoriya

Lazorenko and Anne Lescure for helping with the

organization of the webinars.

José-Antonio Monteiro and Ankai Xu of the Economic

Research and Statistics Division managed the

drafting of the Report. The text production of the

Report was managed by Diana Dent and Anne

Lescure of the Economic Research and Statistics

Division. The production of the Report was managed

by Anthony Martin and Helen Swain of the Information

and External Relations Division. William Shaw and

Helen Swain edited the report. Gratitude is also due

to the translators in the Language and Documentation

Services Division for the high quality of their work.

3

Disclaimer

The World Trade Report and its contents are the sole responsibility of the WTO Secretariat, except

for the opinion pieces written by the external contributors, which are the sole responsibility of their

respective authors. The Report does not reflect the opinions or views of members of the WTO. The

authors of the Report also wish to exonerate those who have commented upon it from responsibility for

any outstanding errors or omissions.

ACKNOWLEDGEMENTS AND DISCLAIMER

WORLD TRADE REPORT 2022

4

Abbreviations

AoA Agreement on Agriculture

APEC Asia-Pacific Economic Cooperation

BCA border carbon adjustment

CBDR [principle of] common but differentiated

responsibilities

CPC United Nations Central Product

Classification

CO

2

e CO

2

equivalent

CTE Committee on Trade and Environment

EDB WTO Environmental Database

EG environmental goods

EGS environmental goods and services

EIF Enhanced Integrated Framework

EITE emission-intensive trade-exposed

EKC Environmental Kuznets Curve

EPP environmentally preferable products

EREG energy-related environmental goods

ES environmental services

ETS EU Emissions Trading System

EU European Union

ET environmental technologies

EWE extreme weather event

FFEDC fossil fuel export-dependent country

FFSR Fossil Fuel Subsidy Reform

G7 Group of Seven

G20 Group of Twenty

GATS General Agreement on Trade

in Services

GATT General Agreement on Tariffs

and Trade

GDP gross domestic product

GGP green government procurement

GHG greenhouse gases

GPA Agreement on Government

Procurement

GTM WTO Global Trade Model

GVC global value chain

HS Harmonized System

ICAO International Civil Aviation Organization

IDP Informal Dialogue on Plastics Pollution

and Environmentally Sustainable

Plastics Trade

IEA International Energy Agency

IMF International Monetary Fund

IMO International Maritime Organization

IP intellectual property

ITC International Trade Centre

I-O input-output

IPCC Intergovernmental Panel on Climate

Change

IRU International Road Transport Union

LDC least-developed country

MFN most-favoured nation

MSME micro, small and medium-sized

enterprise

NDC nationally determined contribution

NGO non-governmental organization

NAFTA North American Free Trade Agreement

NTB non-tariff barrier

NTM non-tariff measure

OECD Organisation for Economic

Co-operation and Development

R&D research and development

RCA revealed comparative advantage

RTA regional trade agreement

SCM subsidies and countervailing measures

SDGs United Nations Sustainable

Development Goals

SIDS small-island developing states

SPS sanitary and phytosanitary

STC specific trade concern

STDF Standards and Trade Development

Facility

TBT technical barriers to trade

TeCO

2

Trade in embodied CO

2

TESSD Trade and Environmental Sustainability

Structured Discussions

TFA WTO Trade Facilitation Agreement

TPRM Trade Policy Review Mechanism

5

TRIMs trade-related investment measures

TRIPS WTO Agreement on Trade-Related

Aspects of Intellectual Property Rights

UNCTAD United Nations Conference on Trade

and Development

TRAINS UNCTAD Trade Analysis Information

System database

UNDRR United Nations Office for Disaster Risk

Reduction

UNECE United Nations Economic Commission

for Europe

UNFCCC United Nations Framework Convention

on Climate Change

UN United Nations

US United States

WCO World Customs Organization

WMO World Meteorological Organization

WTO World Trade Organization

ABBREVIATIONS

WORLD TRADE REPORT 2022

6

Climate change is an existential threat to people’s

lives and is dramatically reshaping economic activity

and trade. This year alone, from the Horn of Africa to

China, from Europe to the Americas, we have seen

increasing heat and prolonged drought damage crops

and reduce electricity production, while low water

levels in major rivers have made it difficult to transport

industrial and agricultural goods. Severe flooding left

a third of Pakistan under water, devastating key export

crops and putting the country’s food and economic

security at risk.

The climate crisis is a problem of the global

commons, and one that demands a collective and

effective multilateral response. The World Trade

Report 2022: Climate Change and International

Trade reviews the role of trade, trade policy and

international trade cooperation in addressing climate

change. It discusses how changing temperature and

weather–and the low-carbon transition required to

contain rising greenhouse gas emissions–are likely

to impact the welfare of nations’ populations and alter

their comparative advantages.

The report argues that trade is a force for good for

climate and part of the solution for achieving a low-

carbon, resilient and just transition. While trade

itself does generate emissions from production and

transport, trade and trade policies can accelerate

the dissemination of cutting-edge technologies and

best practices, and enhance incentives for further

innovation while creating the jobs of tomorrow. Trade

is instrumental for investments in clean energy to

have the greatest reach and impacts, at lowest cost

and where they are needed the most. These are

returns we would be unwise to forego, especially

now that the big green investment push we need will

coincide with rising real costs of capital and looming

uncertainty about energy security due to geopolitical

tensions and war.

Trade and trade policies are also part of any sound

strategy for climate change adaptation, helping

individual countries, especially vulnerable developing

ones such as small-island developing states, least-

developed countries and land-locked developing

countries, better respond to and protect themselves

from extreme weather events, and, in the longer term,

to adjust to shifts in agricultural productivity and

changes in wider international competitiveness. At the

global level, what we call “re-globalization” – more

diversified and deconcentrated goods and services

production, drawing in formerly marginalized countries

and communities with the right business environment

– would promote supply resilience and inclusion in a

world of ever more frequent climate induced shocks.

This would provide better risk management than

reshoring, nearshoring or friend-shoring.

In tandem with other public policies, trade has

already been playing an important role in the global

climate response. For example, the cost of solar panel

systems has plummeted in the last three decades,

and about 40 per cent of the cost decline has been

attributed to scale economies made possible in part

by international trade and value chains. The capacity

of solar panels traded across borders in 2017

reached almost 80GW, equivalent to over 9percent

of global electricity generation.

Further opening up trade in environmental goods and

services could do more. The WTO estimates that

reducing tariffs and non-tariff measures on energy-

related environmental goods could increase total

exports of these products by 5 per cent by 2030 and,

at the same time, lead to a net reduction in carbon

emissions. There are employment benefits, too: the

International Energy Agency estimates that the shift

to clean energy could generate 14 million new jobs

in clean energy sectors and 16 million jobs in related

sectors globally by 2030.

Foreword

by the WTO

Director-General

7

FOREWORD BY THE WTO DIRECTOR-GENERAL

Beyond amplifying the impact of climate policies and

financing, greater international trade cooperation is

key to manage and minimize potential trade frictions

associated with climate action. For instance, close to

70 carbon pricing schemes are presently in operation

worldwide. Without common approaches for prices

and comparing equivalence, there is a significant risk

that unilateral measures aiming to prevent carbon

leakage and loss of competitiveness could stoke

trade tensions and create high administrative costs

for firms and governments. Uncoordinated climate

actions could also hamper decarbonization efforts by

raising uncertainty and discouraging much-needed

investment.

The ongoing proliferation of decarbonization

initiatives and standards – there are more than 20

different decarbonization standards in the steel

sector alone – creates confusion for producers and

could potentially lead to trade frictions. In line with

its longstanding role of promoting transparency vis-à-

vis policy measures affecting trade and encouraging

cooperation in the direction of comparability,

compatibility and harmonization, the WTO could play

a similar role for carbon pricing and standards. The

WTO is working with other multilateral agencies –

the International Monetary Fund, the Organisation

for Economic Co-operation and Development and

the World Bank – on bringing in a trade perspective

to discussions and research on carbon mitigation

approaches.

Clear, predictable and shared understandings about

trade-related climate measures would serve the

needs and development opportunities of businesses

and consumers in developing countries far more

effectively than the high transaction costs that

would come with a mess of varying rules for different

markets. But a just transition to a low-carbon

economy demands additional measures, including

financial support, to help low-income regions address

and overcome the potential adverse effects of carbon

pricing. The case for delivering on the US$100 billion

climate financing pledge remains strong, and a robust

response on loss and damage is urgently needed.

The Aid for Trade initiative – which is increasingly

about investment for trade – can and should help

developing and least-developed countries build

climate-friendly critical trade infrastructure. This

would support a resilient and inclusive low-carbon

transition.

This report is being launched at the same time as

the 27

th

United Nations Climate Change Conference

(COP27). What I hope to see emerge there and

elsewhere is a trade and investment facilitation

pathway in support of a just transition to a low-carbon

economy. Finance is one part of the equation – but

it is not the only part. A good trade policy framework

is necessary to turn climate investment into climate

transformation. We must start to talk about trade not

as a threat but as a solution to the climate crisis.

Achieving better trade and climate outcomes

is possible – but we will need strong political

leadership. Our success at the WTO’s 12

th

Ministerial

Conference in June 2022 – where members

unanimously agreed that trade must be part of the

solution to climate change and struck an accord on

curbing harmful fisheries subsidies that is the WTO’s

first agreement with environmental sustainability at its

core–shows that this is possible.

Looking ahead, the WTO has an opportunity to

use the present moment to strengthen its role as a

forum for coordination on trade and climate change,

to address trade policy barriers holding back the

dissemination and use of low-carbon technologies,

and to support structural changes needed to

decarbonize the global economy. I hope we will make

the most of this opportunity.

Dr Ngozi Okonjo-Iweala

Director-General

WORLD TRADE REPORT 2022

8

Key messages

•

Climate change is reshaping countries’ economic and trade prospects, and is a

major threat to future growth and prosperity. Higher temperatures, rising sea levels and

more frequent extreme weather events bring the prospect of productivity losses, production

shortages, damaged transport infrastructure, and supply disruptions. Without significant

reductions in global greenhouse gas (GHG) emissions, many countries are likely to find their

comparative advantages changing, with agriculture, tourism and some manufacturing sectors

particularly vulnerable to climate impacts.

•

Trade is a force multiplier for countries’ adaptation efforts, reducing costs and

increasing impact. Climate shocks will remain costly and disruptive, but trade can help

countries better prepare and respond, through access to technologies and critical goods

and services, such as food and healthcare products. This is particularly relevant for the

most vulnerable economies – least-developed countries, small-island developing states,

and landlocked developing countries. In the longer-run, open international markets would

help countries smooth necessary economic adjustment and resource reallocation, and more

diversified sources of supply for key goods and services would translate into greater resilience

against localized weather events.

•

Trade can reduce the cost of mitigation and speed up the low-carbon transition and

the creation of green jobs. Though trade, like most current economic activity, generates

GHG emissions, it also contributes to reducing them, by enabling access to cutting-edge

climate technologies; incentivizing innovation in low-carbon technologies by expanding market

size; and fostering competition and scale economies that help drive down costs. Trade and

value chains have been major factors in the dramatic fall in the cost of generating solar and

wind energy. With renewable energy now cheaper than fossil alternatives in some places, the

adoption of renewables has accelerated. But there is scope to do more: WTO simulations

suggest that eliminating tariffs and reducing non-tariff measures on a subset of energy-related

environmental goods could boost exports by 5 per cent by 2030, while the resulting increases

in energy efficiency and renewable uptake would reduce global emissions by 0.6 per cent. To

the extent trade helps speed up the low-carbon transition, it would contribute to job creation:

one estimate suggests the global shift to clean energy will generate as many as 30 million new

jobs in clean energy and related sectors by 2030.

•

International trade cooperation can make climate actions more effective, and

the low-carbon transition more just, by minimizing trade frictions and investor

uncertainty. As governments ramp up climate action towards nationally determined

contributions, there is a risk that unilateral measures aiming to prevent carbon leakage and the

loss of competitiveness of domestic industry could stoke trade tensions, create investment-

discouraging uncertainty, and impose disproportionate costs on firms and governments in

developing countries. International cooperation on trade-related aspects of climate policy,

such as carbon pricing and decarbonization standards, would reduce these risks. The WTO

could play a more valuable role as a venue for transparency, comparability and potential

harmonization of such measures. Aid for Trade, as well as trade-oriented private investment,

can help developing and least-developed countries build climate-resilient trade infrastructure,

contributing to making the low-carbon transition more just and fair.

9

EXECUTIVE SUMMARY

Executive summary

Climate change represents a severe, pervasive and

potentially irreversible threat to people, ecosystems,

public health, infrastructure and the global economy.

Left unabated, it could undo much of the progress

made over recent decades in development, poverty

reduction and prosperity creation. Developing

countries – in particular small-island developing

states and least-developed countries (LDCs) – are

likely to suffer the most, due to their greater

exposure and vulnerability to climate risks and natural

disasters, and their more limited capacity to adapt to

climate change. Leveraging trade to tackle climate

change presents several development and growth

opportunities and will require significant policy

actions to advance a just transition towards a low-

carbon, inclusive and resilient future.

In the face of this existential threat, the 2022 World

Trade Report explores the multifaceted relationship

between international trade and climate change. It

looks at how international trade might exacerbate

climate change, how the consequences of climate

change might alter trading patterns and relationships,

and how trade could be a force multiplier for the global

response to the climate crisis. The report spells out

various ways international trade cooperation, fostered

by the WTO, could support and lower the cost of

implementing the Paris Agreement and fulfilling the

Glasgow Climate Pact’s goal of net-zero greenhouse

gas (GHG) emissions by mid-century (IPCC, 2022a).

The report’s core message is clear: trade is a critical

point of leverage for transforming the global economy

and putting the planet on a sustainable trajectory.

Climate change is a problem of the global commons.

Markets do not suffice to address the threats from

GHG accumulation in the atmosphere because

firms and consumers often do not directly face

the costs of the emissions they cause. To correct

these market failures, carefully constructed climate

change mitigation policies are needed to incentivize

behavioural change and increased investment in

energy efficiency and climate-friendly technologies.

Ambitious GHG mitigation policies face a wide range

of challenges, including conflicting economic and

development priorities, divergent energy strategies

and geopolitical competition. Fragile economic

recovery from the COVID-19 pandemic, rising

inflationary pressures, increasing food security

challenges and the war in Ukraine have added further

uncertainties. While the transition to a low-carbon

economy entails substantial short-term investment

and adjustment costs, it will yield major economic

dividends and create wide-ranging opportunities

for more sustainable and fair development. A well-

managed low-carbon transition can limit climate

risks, promote biodiversity and improve food security.

Investments in clean energy also promise better air

quality, public health and quality of life for people

across the world. Bold climate actions could yield a

cumulated economic gain of US$ 26 trillion between

2018 and 2030 (Garrido et al., 2019). The low-carbon

transition could also create millions of new jobs in

clean energy and energy-related sectors and support

a more inclusive economy, not least because more

women work in the renewable energy sector than in

the fossil fuels sector (IRENA, 2021).

Because the existing build-up of GHGs in the

atmosphere makes some degree of climate change

unavoidable, adaptation strategies are also required

to make communities more resilient in the face of

sea level rise, more intense storms and changed

rainfall patterns leading to more floods, droughts and

wildfires as well as significant effects on agricultural

productivity. These consequences will profoundly

impact international trade and coping with them

requires adaptation efforts to identify, prevent and

reduce climate risks, and minimize unavoidable losses

and damages (IPCC, 2022b).

The report makes clear that trade and climate change

are deeply intertwined, and that more effective

responses to mitigate and adapt to climate change

will require stronger and better international trade

cooperation.

The report makes three key points. First, while

climate change can have profound negative impacts

on international trade, trade and trade policies

are essential elements of sound climate change

adaptation strategies. Second, although trade

generates GHG emissions, trade and trade policies

can foster the transition to a low-carbon economy by

providing access to and spurring innovation in low-

carbon technologies, disseminating best practices

and helping clean energy investments achieve the

greatest reach at the lowest cost. Third, improving the

ambition and effectiveness of climate action requires

greater international trade cooperation at the WTO.

WORLD TRADE REPORT 2022

10

Even though climate change can have profound

negative impacts on international trade, trade

and well-designed trade policies are essential

elements of sound climate change adaptation

strategies.

Climate change can cause productivity losses,

supply shortages and transport disruptions, severely

impacting trade. Because these impacts will differ

across regions, some economies will be at a

disadvantage. Export growth of agricultural products

and light manufacturing from LDCs have been found

to decrease, on average, by between 2 and 5.7 per

cent in response to a rise in the country’s temperature

by 1°C (Jones and Olken, 2010).

Extreme weather events can also affect key transport

corridors and infrastructure, potentially creating

vulnerabilities in the global trade network. Maritime

transport – which accounts for 80 per cent of world

trade by volume – is particularly exposed to climate

change, while other modes of transport can also

be impacted. Small economies and landlocked

countries, which trade through a limited number of

ports and routes, can suffer major trade bottlenecks

from climate-related disruptions. For instance, the

Paraná River transports 90 per cent of Paraguay’s

international trade of agricultural goods, but recurrent

droughts have in recent years frequently lowered

water levels, diminishing the weight barges can carry,

causing congestion and delays.

Climate-induced disruptions tend to be more severe

in heavily concentrated global value chains (GVCs)

where intermediate inputs are difficult to replace

in the short run. For example, in 2011, flooding

in Thailand disrupted the global electronic and

automotive industries, causing an estimated 2.5

percentage point decline in the rate of growth of

global industrial production (Kasman, Lupton and

Hensley, 2011). Climate-induced supply chain risks

are often exacerbated by firms’ limited capabilities to

assess climate risks and implement risk management

strategies.

Without significant reduction in GHGs, climate

change is likely to alter countries’ comparative

advantage and trade patterns by changing

endowments in natural resources or altering the

efficiency with which land, labour, capital and other

production factors can be deployed to produce

goods and services. Commodity dependence and

lack of diversification can exacerbate vulnerabilities

to climate change, underscoring the need to support

efforts to accelerate economic diversification.

Agriculture, tourism and some manufacturing

sectors are particularly vulnerable to climate change.

Agriculture is the most exposed and vulnerable

sector to changes in temperature and precipitation,

raising serious concerns about future food security.

Sub-Saharan Africa and South Asia are expected to

experience larger adverse agricultural yield shocks

than other regions; and given their high share of

agricultural employment, they may face more severe

labour market disruptions. Changes in climate might

also reduce the touristic appeal of long-favoured

destinations, while sea level rise and extreme

weather events could permanently damage tourism

infrastructure. Manufacturing sectors dependent on

climate-sensitive inputs, such as food processing,

could suffer from reduced access to raw materials.

Labour-intensive production could also be adversely

affected as rising temperatures diminish capacity to

work and raise risks of accidents and heat exhaustion.

Adapting to climate change is a sustainable

development imperative. Without understating how

costly and disruptive adaptation will continue to be,

trade can make an important contribution to climate

risk prevention, reduction and preparedness.

Trade can facilitate the development and deployment

of pro-adaptation technologies, such as climate-

resistant crop varieties, early warning systems and

water conservation and storage systems. By fostering

higher economic growth, trade can generate

additional financial resources to invest in adaptation

strategies such as climate-resilient infrastructure.

Trade openness also allows for wider access to

services that help prepare for climate-related

shocks, such as weather forecasting, insurance,

telecommunications, transportation, logistics and

health services.

Access to imported essential goods and services,

such as food and medical supplies, can help

economies cope and recover after an extreme

weather event hits. Facilitating imports of

construction materials can contribute to post-disaster

reconstruction. Allowing trade to resume faster after

climate-induced shocks can also support economic

recovery. Even in the absence of extreme weather

events, long-term shifts in weather patterns can still

cause crop yields to fall, and trade can help alleviate

food insecurity by allowing regions to import food

to fill demand gaps. Overall, countries more open

to trade tend to have a greater capacity to adapt to

climate change (see Figure 1).

The role of trade in coping with climate change

underlines that trade policies must be an integral

11

EXECUTIVE SUMMARY

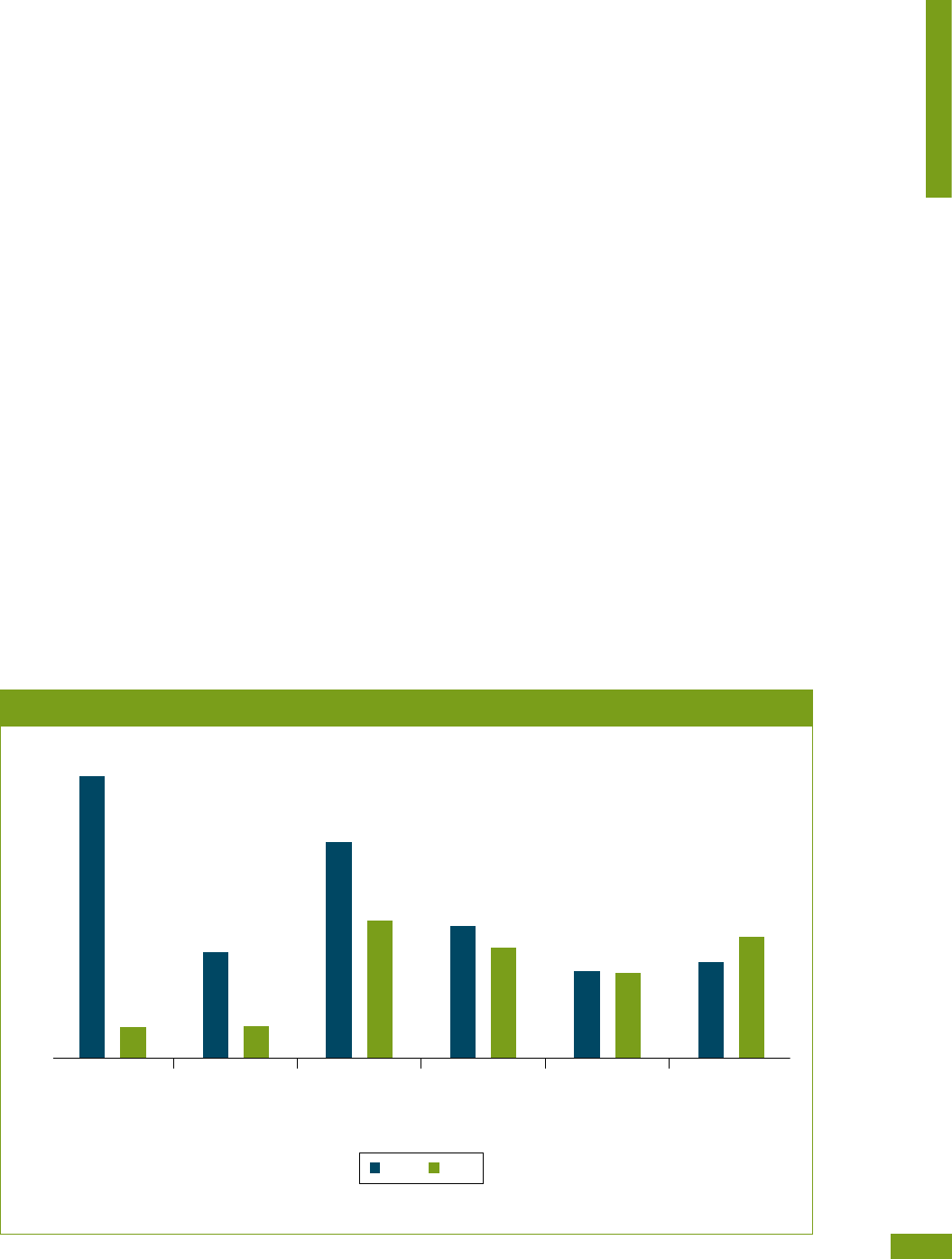

Figure 1: Greater capacity to adjust to climate change tends to be associated with greater

openness to trade

So

urces: Authors’ calculations based on ND-GAIN Climate Readiness Index and the trade openness index for 2020 from the World

Development Indicators.

Note: The climate change readiness index measures a country’s ability to leverage investments and convert them to adaptation actions.

The trade openness measures the sum of a country’s exports and imports as a share of that country’s GDP in percentage.

part of climate change adaptation strategies. A small

but increasing number of trade measures notified by

WTO members between 2009 and 2020 are related

to climate change adaptation, though these measures

– which mostly take the form of support in the

agricultural sector – account for less than 4per cent

of all notified climate-related trade measures (161 out

of 4,629).

Trade and trade policy are, however, not a panacea

to adapt to the highly disruptive consequences

of climate change. Addressing the factors and

conditions underpinning the vulnerabilities and

exposures to climate risks is essential. In addition,

well-functioning markets, including in the areas of

infrastructure, finance, food and labour, are important

to facilitate adjustment.

Although trade generates GHG emissions, trade

and trade policies can be part of the solutions

to support a low-carbon transition.

Trade, like most economic activities, emits GHGs.

The world share of carbon dioxide (CO

2

) emissions

embodied in world goods and services exports

peaked in 2011 and was estimated to account for

around 30 per cent of global carbon emissions in

2018. This share indicates the close relationship

between production, trade, consumption and the

consequent emissions under current technologies

and production processes.

International trade has complex effects, both positive

and negative, on GHG emissions, going well beyond

the emissions released during the production and

0.1

0.5

0.7

1 1.4 21.2 1.6 2.2

Trade openess index (in logarithm)

1.8 2.4 2.6

0.2

0.3

0.6

0.8

0.4

Climate change adaptation readiness index

Low-income Middle-income High-income

WORLD TRADE REPORT 2022

12

transportation of the exported goods and services.

The overall impact of trade on carbon emissions

depends, among others, on the sector and countries

involved as well as the energy sources, production

methods and modes of transport.

On the positive side of the ledger, international trade

increases the worldwide diffusion and deployment of

lower-emission goods, services, capital equipment

and know-how. It also reduces the costs of these

products through efficiency improvements, economies

of scale and learning-by-doing. For instance, the cost

of solar electricity has plunged by 97 per cent since

1990. A significant part of the cost decline of solar

panel systems has been attributed to GVCs, which

have enabled producers to lower production costs

and reap economies of scale by locating different

production stages in different countries (WTO and

IRENA, 2021). Market opportunities for low-carbon

exports can also spur more investment and innovation

in new low-carbon technologies and encourage

efforts to better adapt these technologies to local

conditions.

In addition, trade opening can reduce the carbon

intensity of economic output by shifting resources to

more productive and cleaner firms, as firms engaged

in international trade tend to be more competitive

and energy efficient than purely domestic firms. The

higher incomes typically associated with greater

integration into global trade also give individuals the

space to demand higher environmental quality and

to pressure governments to adopt more stringent

climate regulations and provide additional financial

resources for environmental protection.

International trade in renewable energy and electricity

has also the potential to help compensate for the

uneven geographical distribution of usable sunlight

and wind, though this will hinge on important

technological breakthroughs – notably in energy

storage. More developing countries are already

moving to harness their abundant renewable energy

potential. For instance, Morocco hosts the world’s

largest solar power station, while Egypt is building a

solar photovoltaic park touted to become the world’s

largest.

On the negative side of the ledger, trade opening

raises GHG emissions by increasing the production,

transportation, consumption and disposal of

products. The fragmentation of production

represented by GVCs involves more transport and

therefore more emissions. Trade may–in the absence

of relevant policies – incentivize emissions-boosting

deforestation.

Changes in the sectoral composition of

production–a standard result of trade opening–can

also increase or reduce GHG emissions, depending

on whether the country in question has a comparative

advantage in carbon-intensive industries, which

in turn depends on factors including resource

endowments, technological level and environmental

and energy policies (WTO, 2021a).

Rising concern about trade-related GHG emissions

has led to calls to limit imports in favour of producing

and consuming local goods and services. But if

countries close their borders to trade, meeting

demand for previously imported goods and services

would cause domestic production and associated

GHG emissions to rise; while foregoing the broader

gains from trade would cause living standards to fall.

Instead of re-shoring, the low-carbon transition

would be better supported – and accelerated – by

cleaner trade, which would involve reducing the

carbon intensity of production, transportation and

GVCs, developing and deploying climate-friendly

technologies and promoting trade in climate-friendly

goods and services. Major decarbonization pathways

for international transport include switching to

lower-carbon fuels, improving vehicle efficiency and

phasing-out carbon-intensive vehicles.

Well-designed trade policies must support the role

of trade in deploying and disseminating climate

mitigation technologies. Trade and trade policies are

an integral part of a limited but increasing number

of countries’ plans to achieve carbon emission-

reduction targets under the Paris Agreement’s

nationally determined contributions. Complemented

by other policies, trade policies can help countries

diversify away from reliance on carbon-intensive

sectors, create new jobs and increase the ambition

of mitigation efforts. Between 2009 and 2020,

WTO members notified 3,460 trade-related climate

change mitigation measures explicitly addressing

climate change mitigation, energy conservation and

efficiency, and alternative and renewable energy.

Support measures and technical regulations are the

main types of notified trade-related climate change

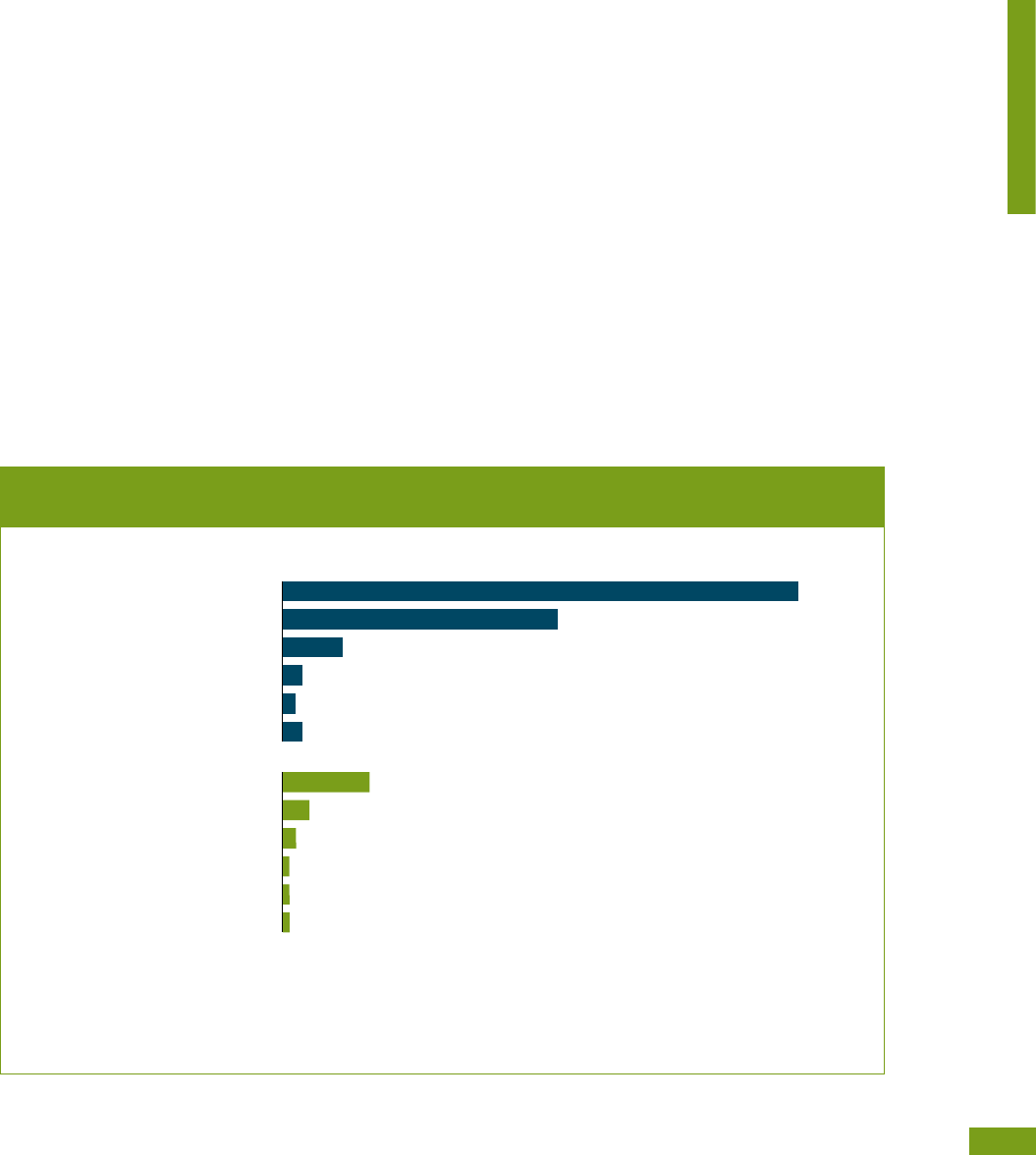

mitigation measures (see Figure 2).

Despite the benefits of opening trade in the

environmental industry, barriers to trade in

environmental goods and services remain significant.

In addition, tariff and non-tariff barriers tend to be

lower in carbon-intensive industries than in clean

industries (Shapiro, 2021).

Removing barriers to trade in environmental products

can contribute to addressing climate change. WTO

13

EXECUTIVE SUMMARY

simulation analysis suggests that eliminating tariffs

and reducing non-tariff measures on some energy-

related environmental goods and environmentally

preferable products could increase global exports

in these products by US$ 109 billion (5 per cent)

and US$ 10.3 billion (14 per cent), respectively,

by 2030. The resulting improvements in energy

efficiency and renewable energy adoption are

estimated to reduce net carbon emissions by 0.6 per

cent, while the knock-on effects of accelerating the

spread of environmental innovation would do much

more, including increasing the demand for ancillary

services relating to the sale, delivery, installation and

maintenance of environmental technologies.

That said, harnessing the full potential of international

trade in renewable energy and other environmental

goods and services also requires ambitious climate

policies and actions to upgrade power-generation,

transmission and distribution infrastructure as well as

to build a well-functioning quality infrastructure.

Improving the ambition and effectiveness

of climate change action requires greater

international trade cooperation.

Addressing climate change requires global

cooperation on all fronts, and international trade

cooperation, at the WTO and elsewhere, is an integral

part of the efforts.

The bottom-up international climate regime, with

nationally determined contributions and mitigation

actions, encourages broad-based participation and

underlines the urgency of climate action. But it also

results in widely varying levels of climate ambition

across jurisdictions, with the attendant risks of carbon

leakage and competitiveness loss, especially in

carbon-intensive and trade-exposed sectors. These

risks have prompted some countries to consider

border carbon adjustment measures. Uncoordinated

trade-related climate policies, however, could give

rise to trade tensions and heighten marketplace

uncertainty in ways that discourage much-needed

Figure 2: Support measures and technical regulations are the most common trade-related

climate change mitigation measures

Sources: Authors’ calculation, based on the WTO Environmental Database.

Note: The category “technical regulations” includes conformity assessment procedures. One notified measure can cover more than one

type of policy.

Support measures Technical regulations Other measures

Notified climate change mitigation measures

2017 2018 2019 202020152014 2016201320112009 2010 2012

338

304

444

139

415

312

233

324

360

231

160

187

WORLD TRADE REPORT 2022

14

low-carbon investment. Avoiding such outcomes

calls for leveraging every opportunity at the WTO and

elsewhere for improving cooperation on the trade-

related aspects of climate change policies.

At the regional level, a limited but increasing number

of trade agreements, namely 64 out of 349 notified

regional trade agreements (RTAs), explicitly contain

climate change-related provisions. Some of these

RTAs commit parties to effectively implement the

Paris Agreement and adopt climate change policies,

including carbon pricing, while a few others remove

some trade and investment barriers to climate-friendly

goods, services and technologies.

At the global level, as noted above, the open and

predictable international markets underpinned by the

multilateral trading system already facilitate access to

environmental technologies, food and other critical

supplies. WTO members notify climate-related

measures and discuss potential concerns, as well

as the underlying environmental rationale, in various

WTO bodies such as the Committee on Trade and

Environment. These discussions are also a venue for

exchanging national experiences and practices.

The WTO agreements expressly recognize the

rights of members to adopt measures to protect

the environment, so long as they are not applied

arbitrarily and are not more restrictive than necessary

to meet the objective in question. Climate objectives,

rather than the protection of domestic producers,

must be the central rationale for the development

and implementation of trade-related climate policies.

Trade-related climate policies should also consider

their impact on other nations’ climate efforts. The

protection and enforcement of intellectual property

rights, as provided by WTO rules, is also essential

to support innovation in environmental technologies

while promoting the transfer of technology.

But WTO members can do much more to enhance

the contribution of trade and trade policy to their

climate objectives.

First, with the increasing number of trade-related

climate measures being taken nationally, there

is a strong case for strengthening the role of the

WTO as a forum for coordination and dialogue,

and for identifying potential action on trade and

climate change. The committee process could be

used to identify transparency and knowledge gaps,

opportunities for coordination, capacity needs and

perspectives of developing countries, and areas

for further work, including potential negotiations. At

the 12

th

Ministerial Conference in June 2022, WTO

members concluded an agreement that prohibits

certain types of fisheries subsidies. Continuing

work on additional provisions for a comprehensive

agreement on fisheries subsidies would further

contribute to sustainable management of marine

resources and biodiversity.

Second, members are already beginning to pursue

a new generation of sustainability driven initiatives

aimed more at using trade as a means to help achieve

global public goods than at correcting a particular

trade distortion. These initiatives include the

Trade and Environmental Sustainability Structured

Discussions, the Informal Dialogue on Plastics

Pollution and Environmentally Sustainable Plastics

Trade, and the Fossil Fuel Subsidy Reform initiative.

Some of these discussions focus on traditional fare

for trade negotiators, namely tariff and non-tariff

policies. For instance, removing trade barriers on

environmental goods and services would lower costs,

expand markets and boost the deployment of climate-

friendly technologies. Pursuing greater alignment on

low-carbon standards would lower compliance costs

and encourage greater scale and investment.

Other initiatives focus instead on generating new

knowledge that can inform and improve governments’

efforts to integrate trade into their environmental

and climate change strategies. This could involve a

better understanding of the environmentally harmful

impacts of subsidies or of trade-related linkages with

the circular economy. Finding a balance between

support incentives for low-carbon technologies

while minimizing negative spillovers on trading

partners would also provide more predictable and

credible market signals for low-carbon investment

and consumption. The dialogue on plastics seeks to

generate knowledge on plastic trade flows in order

to support negotiations on an international plastics

treaty under the auspices of the United Nations

Environment Programme.

Third, WTO members could work on supply side

factors to enhance the climate resilience of their

supply chains. Deepening and diversifying supply

and transport networks would not just help reduce

vulnerability to the kinds of supply chain disruptions

seen since the start of the pandemic; it would also

enhance resilience in the face of localized climate

events. Stronger information sharing and monitoring

would help food and energy security for all members,

while helping them manage risks related to supply

chain bottlenecks. An example of how this might

work in practice is the Agricultural Market Information

System, which is a platform of international agencies,

including the WTO, which tracks the supply of key

agricultural commodities and provides a forum for

15

coordinated policy responses when needed to

prevent markets from seizing up. At the 12

th

Ministerial

Conference, WTO members vowed to address the

global food security challenges by exempting from

export restrictions food bought by the World Food

Programme for humanitarian purposes and pledging

to facilitate trade in food, fertilizers and other

agricultural inputs. Implementing these decisions

could contribute to managing the knock-on effects of

surging food prices during a crisis, thus increasing

food security.

Fourth, improving the ability to understand and

manage climate-related risks and investment

opportunities would improve the synergies between

climate finance and Aid for Trade. Climate finance

to developing countries continues to fall short

of the US$ 100 billion goal for 2020 (OECD,

2022a) and has not achieved the balance between

adaptation and mitigation finance set out in the Paris

Agreement (UNEP, 2021a, 2021b). However, the

Aid for Trade initiative, supported by the WTO and

other organizations, can help developing countries,

particularly LDCs, to build climate-resilient trade

capacity and infrastructure, and support trade

policies to foster a low-carbon transition. Between

2013 to 2020, Aid for Trade disbursements related

to climate action totalled US$ 96 billion, with a

larger share of the disbursements directed at climate

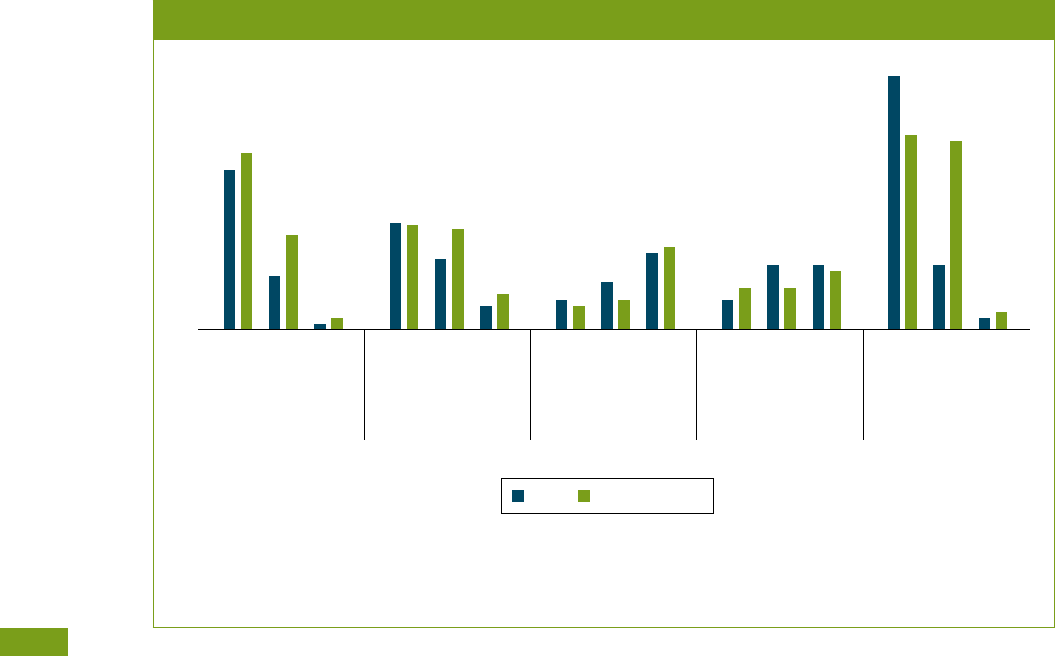

mitigation (see Figure 3).

Finally, reinforcing the WTO’s existing cooperation

with international and regional organizations, including

in the areas of climate risk prevention, climate-

induced disaster relief, transport decarbonization

and climate finance, is important to advance trade

cooperation on climate change. Over the past few

years, WTO members have started to address some

of these issues. However, the scale and urgency of

the climate crisis demand additional efforts in support

of a more inclusive and just transition to a low-carbon

economy and a more resilient future.

Figure 3: Aid for Trade disbursements related to climate change have increased over

the past decade

Sources: Authors’ calculations, based on Organisation for Economic Co-operation and Development DAC-CRS (Development Assistance

Committee Creditor Reporting System) Aid Activities Database.

Note: Only projects with an explicit objective of adapting to or mitigating climate change and projects identifying climate change as

important but secondary objective are considered as climate change-related official development assistance. Projects can be cross-

cutting and have both adaptation and mitigation objectives.

Energy Transport and storage Agriculture, forestry and fishing Others

Climate change adaptation

Aid for Trade disbursements related to climate change

(current US$ billion)

Climate change mitigation

2013

2014

2015

2016

2017

2018

2019

2020

6.5

6.6

7.9

9.5

12.0

12.2

13.4

12.3

2.9

3.4

4.1

4.6

4.9

4.9

4.9

5.7

EXECUTIVE SUMMARY

A

Introduction

Tackling climate change requires a transformation of the global

economy. While limiting consumption and changing lifestyles

would help, reducing greenhouse gas emissions to net zero will be

impossible without technological and structural change on a global

scale. This transformation will involve costs, but also opportunities

– not just to head off an environmental catastrophe, but to reinvent

the way the world generates energy, manufactures products and

grows food. Just as trade helped to drive economic progress in

the past – by incentivizing innovation, leveraging comparative

advantages and expanding access to resources and technologies

– trade can play a central role in driving progress towards a low-

carbon global economy. But harnessing the potential of trade will

demand new policies and more cooperation.

Contents

1. The next great transformation 18

2. Harnessing the transformative power of trade 20

3. Overview of the report 23

18

WORLD TRADE REPORT 2022

1. The next great transformation

Paradoxically, economic progress is both the cause

of and the solution to the climate crisis. To head off

dangerous climate change, the Paris Agreement aims

to limit the global warming to 1.5°C this century. This

means that greenhouse gas (GHG) emissions need

to be cut by roughly 50 per cent by 2030 and reach

net zero by 2050.

1

The most realistic way modern

economies can achieve this goal – without cutting

back living standards in richer countries and cutting

short development in poorer ones – is by modernizing

even more, harnessing human innovation, ingenuity

and entrepreneurship to advance low-carbon

technologies and to use the planet’s resources more

sustainably.

Dramatic advances in automation, transportation

and industrialization – all powered by fossil fuels –

have driven the exponential growth of the global

economy over the past two and half centuries,

resulting in rising living standards, increased mobility,

and improved material well-being for a fast-growing

global population. In important ways, the industrial

revolution was also an energy revolution (Wrigley,

2010). By discovering how to convert fossil fuels into

mechanical energy, starting with the steam engine,

humanity unlocked seemingly limitless supplies of

energy to power seemingly limitless economic growth

and development.

But ever-expanding growth has also released ever-

greater amounts of heat-trapping GHG emissions

into the atmosphere – from electricity generation,

transportation, industry, agriculture and deforestation

– which in turn has contributed to the warming of the

planet and its negative climactic and environmental

knock-on effects. Almost three-quarters of global

GHG emissions come from energy consumption;

another 18.4 per cent from agriculture, forestry and

land use; 5.2 per cent from industrial processes; and

3.2 per cent from waste (Ritchie, Roser and Rosado,

2020). As long as the world remains dependent on

high-carbon technologies, increasing economic

production will almost inevitably lead to increasing

GHG emissions.

Yet, while technological and economic progress has

“fuelled” the climate crisis, it is also indispensable

to mitigating and overcoming it. Replacing fossil

fuels with renewable energies – solar, wind and

geothermal power, and others – is essential to

avoid and reduce GHG emissions, as are steps to

decarbonize transportation, steel production, cement

manufacturing and agriculture, and to make economic

ecosystems less wasteful and more resource-

efficient overall.

Adapting to the adverse effects of climate change

will also require technological solutions – from

developing drought-resistant crops and resilient

water supplies, to building flood defences, improving

weather forecasting and setting up early warning

systems (UNFCCC, 2016a).

Given that many lower carbon technologies – from

solar panels and electric cars to vertical farms and

electric arc furnaces – already exist, the challenge

is to scale up their production and deployment. One

influential study argues that two-thirds of economies,

including major emitters like the United States, the

European Union and China, could reduce their GHG

emissions by 80 per cent by 2030, and achieve

carbon neutrality by 2050, through the mass adoption

of electrification based on existing wind, hydro and

solar technologies (Jacobson et al., 2017).

Even more cutting-edge technologies, such as green

hydrogen or direct air carbon capture and storage,

are also advancing rapidly. Then there are the

myriad “soft” climate technologies – data-crunching,

information-sharing, training and education – which

are easier to adopt, and which will be just as critical

to shift economies towards low-carbon alternatives.

It is also important to focus not just on what

technologies are needed, but on how they are used. It

has long been recognized that it is only by using new

technologies that we learn how to optimize and exploit

their full potential (Arrow, 1962). This “learning-by-

doing” dynamic can take time (David, 2002). In the

same way that it took decades for the invention of the

dynamo to translate into mass electrification, it could

take years to realize the full potential of solar power or

carbon farming. Thus, it makes sense to scale up new,

clean, low-carbon technologies now, even if the initial

investment costs are high, as expanding capacity

early on can encourage usage, improve performance,

drive down prices, and ultimately make renewable

technologies more attractive and competitive.

Realizing the potential of one innovation also often

hinges on marrying it to another innovation (Harford,

2017). Just as the explosion of the internet after

the mid-1980s depended on parallel innovations in

satellite and fibre optic telecommunications, electric

vehicles are now poised to revolutionize clean-energy

transportation because they are benefitting from

other technological breakthroughs, including the

mass production of affordable lithium-ion batteries,

the roll-out of electric vehicle charging networks and

more readily available renewable energy.

Conversely, the absence of synergistic technologies

can significantly slow or block economic progress.

CLIMATE CHANGE AND INTERNATIONAL TRADE

A. INTRODUCTION

19

For example, the lack of affordable and efficient

technological solutions to the challenge of long-term,

large-scale energy storage – a challenge arising from

the intermittent nature of some lower carbon energy

technologies such as solar and wind power – is a key

missing piece of the renewable puzzle which urgently

needs to be “discovered” if renewables are to become

a reliable replacement for fossil fuels worldwide.

This positive process of technological interaction,

cross-fertilization and mutually reinforcing innovation

takes place at the global, not just the firm, level. The

fact that photovoltaic (PV) cells, which convert solar

energy into electricity, are increasingly affordable and

available is the result of mutually supportive back-and-

forth innovations across several continents, including

US investments in PV cell research and development

(R&D) in the 1960s and 70s; European policies to

accelerate domestic solar panel installation in the

1990s and 2000s; and Chinese efforts to improve

and scale production after 2011 (IEA, 2022a).

Technological cooperation, competition and cross-

fertilization do not just spur innovation; they also

encourages needed technological diffusion. Many

developing countries have abundant renewable energy

potential that access to low-carbon technologies and

infrastructure could unleash (IRENA, 2022). This is

starting to happen. Kenya is already a world leader in

the number of solar panel systems installed per person,

while 90 per cent of Nepal’s electricity comes from

hydro-electric power. Locally generated renewable

energy allows developing and least-developed

countries to bypass many of the logistical difficulties

and high costs involved in the transmission and

distribution of fossil-fuel energy, improving their energy

access and self-sufficiency. Bringing clean energy to

the 759 million people in the developing world who

still lack access to electricity would not only stimulate

economic growth and job creation and reduce poverty,

but would significantly improve essential services,

such as healthcare, education and the internet.

The shift to low-carbon farming – especially

climate-smart agriculture techniques that focus

on intercropping, crop rotation, agroforestry, and

improved water management – can bring similar

benefits to developing-country farmers in terms

of improved productivity, greater resilience, less

deforestation, and reduced reliance on fertilizers and

fuels (Brakarz, 2020). In short, the diffusion of low-

carbon technologies can provide poorer countries

with the essential tools they need both to limit GHG

emissions and to accelerate their development.

Achieving a shared and “just” transition to a low-

carbon global economy is not just the right thing to

do; it is also in everyone’s interests. Climate change

will not be stopped if only wealthy economies have

access to low-carbon technologies while poor

economies continue to have to rely on fossil fuel-fired

power plants and internal combustion engines. Since

everyone is impacted by climate change, everyone

has an interest in ensuring that the technological

tools and resources to reduce emissions are as

widely available as possible.

Wealthy economies can also benefit in more direct

ways from technological development in poorer

countries. A striking example of North-South

technological collaboration is the ambitious plan to

deliver Moroccan solar and wind farm electricity to

UK consumers via an underwater cable stretching

3,800 km – the world’s longest cable of this kind.

When completed in 2030, it is hoped that the Xlinks

Morocco-UK Power Project will deliver low-cost, clean

power to over 7 million UK homes, representing 8 per

cent of current UK electricity needs (Hook, 2021).

Indeed, the transition to a low-carbon global economy

will create enormous investment, employment and

growth opportunities – not just adjustment costs –

for developed and developing countries alike. For

example, global investment in the low-carbon energy

transition – across sectors ranging from power

generation, energy storage and electric vehicles, to

sustainable materials, electrical efficiency and carbon

capture – already totalled US$ 1.3 trillion in 2021,

doubling the investment of US$ 655 billion in 2017

(IEA, 2022b). In order to reduce GHG emissions to

net zero by 2050, cumulative investment in renewable

energy would need to reach US$ 131 trillion over the

next 30 years (McKinsey & Company, 2022).

Similarly, massive investment opportunities are

opening up in the steel, cement, farming, forestry

and waste management industries as they shift to

low-carbon technologies and processes. Building

low-carbon industries and infrastructure will not

only require new investment and equipment; it will

also require new workers and skills. Shifting to clean

energy, for instance, could generate 14 million new

jobs in clean energy sectors and 16 million additional

jobs in energy-related sectors globally by 2030 (IEA,

2021). In short, the transition to a low-carbon economy

will entail the construction of a new economy.

The good news is that low-carbon technologies are

expanding – and at a faster pace than many predicted

(Naam, 2020).

2

For example, renewables accounted

for roughly 11 per cent of global primary energy and

30 per cent of electricity generation in 2021 (IEA,

2022b). Despite supply chain bottlenecks, rising raw

material prices and growing geopolitical tensions,

20

WORLD TRADE REPORT 2022

the International Energy Agency (IEA) projects that

renewables are on track to account for almost 95 per

cent of the increase in global power capacity through

2026, with solar power alone providing more than

half of that increase. The IEA expects the amount

of renewable capacity added between 2021 and

2026 to be 50 per cent higher than between 2015

and 2020 – and even these optimistic forecasts may

underestimate the speed and scale of the transition.

The bad news is that although global renewable

energy capacity is growing rapidly, overall global

energy demand is growing almost as fast, so fossil

fuel consumption continues to rise (see Figure A.1).

Nearly 80 per cent of the world’s energy is still

generated by burning fossil fuels, notably oil, coal

and gas, partly because supplies of renewable

energy need to be scaled up, and partly because

fossil fuel consumption is still subject to strong path

dependence due to technological, infastructural,

institutional and behavioural lock-ins. Global energy-

related carbon emissions rose by 6 per cent in 2021

to 36.3 billion tonnes – their highest level ever, and

65 per cent higher than they were in 1990 (IEA,

2022c). The IEA estimates that the current pace of

renewable power capacity growth will need to double

over the next decade if the global economy is to stay

on a pathway to net zero emissions by mid-century.

Other sectors also face the challenge of accelerating

the shift to low-carbon technologies and practices.

The challenge is especially daunting in agriculture

– compared to power generation or transportation,

for example – because the emissions-reduction

technologies are more amorphous and the sector

is more diffuse, requiring changes to how over

two billion people farm and how billions more eat

(McKinsey & Company, 2020). At the same time,

the challenge is intensified because of agriculture’s

unique vulnerability to climate change – including

extreme weather events, frequent droughts, and

invasive species and pests – and because of an

expanding global population’s growing need for food.

2. Harnessing the transformative

power of trade

What role will trade play in the transition to a low-

carbon global economy? In the past, trade has been

part of the problem, contributing to climate change

both directly, by generating increasing transport

emissions (shipping, air freight, trucking and rail), and

indirectly, by helping to drive carbon-intensive global

growth. But in the future, with the right policies in

place, trade can be a major part of the solution.

Figure A.1: Fossil fuels remain the dominant energy source despite increasing use

of renewables

Source: Authors’ calculations, based on Smil (2017) and BP Statistical Review of World Energy (2017).

Traditional biomass Coal Oil Nuclear RenewableGas

160,000

140,000

120000

100,000

80,000

60,000

40,000

20,000

1800

1806

1812

1818

1824

1830

1836

1842

1848

1854

1860

1866

1872

1878

1884

1890

1896

1902

1908

1914

1920

1926

1932

1938

1944

1950

1956

1962

1974

1968

1980

1992

1983

1998

2010

2016

2004

Terawatt-hours

0

A. INTRODUCTION

21

CLIMATE CHANGE AND INTERNATIONAL TRADE

Trade can increase counties’ access to lower-

emissions goods, services and capital equipment,

and can help to diffuse critical technologies

and know-how. It can drive down the costs of

environmental products by encouraging efficiency,

economies of scale and learning-by-doing. Perhaps

most importantly, it can spur innovation by opening

up new market opportunities for low-carbon exports

and investments and by incentivizing entrepreneurs

and industries to compete to fill them.

If low-carbon production reaches the point where

it beats high-carbon production on price and

performance – because environmental costs are

internalized in high-carbon production through taxes

and other policies or because technological advances

alone make low-carbon alternatives cheaper and

better – then market forces will increasingly drive the

transition and progress will accelerate.

This is already happening. Scientific advances,

more efficient production processes, and rising

global demand – all supported by open world trade

– have driven an astonishing reduction in price

and improvement in performance of low-carbon

technologies (see Figure A.2). The price of solar

power, for example, has fallen by almost 90 per cent

since 2010, while the efficiency of solar panels has

doubled since 1980. Last year alone, the cost of

electricity from onshore wind fell by 15 per cent,

and from offshore wind by 13 per cent. The price of

lithium-ion batteries has plunged by 97 per cent since

1990, while their energy density has nearly tripled in

just 10 years.

Even more challenging sectors, such as steel

production, managed to cut energy use in half

between 1975 and 2015 – with reductions continuing

– because of technological advances and a shift from

traditional blast furnaces toward electric arc furnaces

(IEA, 2020). As a result of these dramatic price and

performance improvements, low-carbon technologies

are becoming more economically competitive, not just

more environmentally sustainable, alternatives. For

example, almost two-thirds of the world’s new wind

and solar power plants are able to generate electricity

more cheaply than the world’s cheapest new coal

plants (IEA, 2022a; WTO and IRENA, 2021).

The fundamental driver of this change is

improvements in technology and production, which

are in turn being driven by strong learning-by-doing

effects. As the world gets better at building, installing

and using solar panels, for example, the price falls

and the technology improves. It has been estimated

that every time the number of solar panels installed

doubles, their price drops another 30 to 40 per cent

(Naam, 2020). By helping to create a competitive,

dynamic and integrated a global marketplace for solar

and other clean technologies, trade plays a central

Figure A.2: The price of renewables has plunged in the last 10 years

Source: Authors’ calculations, based on Lazard’s Levelized Cost of Energy Analysis (2019).

Solar

photovoltaic

Onshore wind

Gas peaker

Solar thermal

tower

Gas

(combined cycle)

Nuclear

Electricity price from new power plants

(US$ per megawatts)

359

40

135

41

275

175

168

141

111

109

123

155

2009 2019

22

WORLD TRADE REPORT 2022

role in underpinning and accelerating this process. It

is significant that between 2010 and 2020, exports

of solar panels increased and their prices fell sharply

(see Figure A.3).

But the contribution of trade and trade policy to a

just low-carbon transition could be strengthened

and improved. One positive step would be to reduce

trade-distorting measures on climate-friendly

goods, services and technologies and to strengthen

supply chains. Opening up trade across a range of

low-carbon products and services would expand

global access, increase competition and lower

prices, making it easier and cheaper for economies

to transition to low-carbon energy, mobility and

production alternatives, and thus reducing overall

emissions. Conversely, by making it more difficult

to import key environmental technologies, e.g., by

raising tariffs or imposing restrictions, the shift from

a high- to a low-carbon economy will only be slowed

and impeded.

Another key issue is the interface between trade and

environmental subsidies and other support measures.

A growing number of countries use subsidies either

to encourage producers to invent, adopt and deploy

low-carbon technologies, or to encourage consumers

to purchase environmentally sustainable products

and services. If they are well-targeted and non-

discriminatory, environmental subsidies can play

a positive role in scaling up new technologies and

making climate-friendly products more affordable.