Customs Trade Partnership

Against Terrorism

Trade Compliance Handbook

2

CTPAT Trade Compliance Handbook | October 2022

I am pleased to present the Customs Trade Partnership Against Terrorism

(CTPAT) Trade Compliance Handbook, a resource for understanding

CTPAT’s modernized Trade Compliance program.

CTPAT has embarked on a journey over the previous four years to

reinvigorate U.S. Customs and Border Protection’s (CBP) Trade

Compliance efforts. In close collaboration with private industry and best

practices put forth by international trade groups, such as the World

Customs Organization (WCO), CTPAT has established a program that is

equipped to be the global standard for Trade Compliance.

The new CTPAT Trade Compliance program is an evolution of the former Importer Self-

Assessment (ISA) program. The goal of the program is to increase importer compliance and the

flow of legitimate cargo into the United States. In exchange for compliance with regulatory

trade requirements imposed by CBP and other government entities, the CTPAT Trade

Compliance program offers meaningful benefits to the trade as part of partnership. These

benefits are a combination of legacy CTPAT and ISA benefits, as well as benefits developed in

collaboration with partners of the CTPAT Trusted Trader Pilot (established under Federal

Register Notice 34334) and the Commercial Customs Operations Advisory Committee’s

(COAC) Secure Trade Lanes Subcommittee (Trusted Trader Working Group). These groups

worked collaboratively with CBP to understand the major challenges importers face today, and

to develop benefits that address those challenges and make program partnership worthwhile.

This handbook provides an overview of the major changes and improved industry benefits that

have led to the modernization of CTPAT’s Trade Compliance program and detailed instructions

for applying and maintaining partnership. I hope you will find this resource to be helpful as you

begin the process to join the CTPAT Trade Compliance program or begin the process of

fulfilling your annual partnership requirements.

The collaborative nature of this program presents us the unique opportunity to continually

maintain and advance a world class Authorized Economic Operator (AEO) program that

increases the security of the trade environment globally. Thank you for doing your part to

protect our Nation and support CBP’s mission.

Sincerely,

Manuel A. Garza Jr.

Director, CTPAT

Cargo and Conveyance Security

Office of Field Operations

3

CTPAT Trade Compliance Handbook | October 2022

CTPAT TRADE COMPLIANCE

TABLE OF CONTENTS

1. INTRODUCTION AND PROGRAM MODERNIZATION

1.1 P

URPOSE

1.2 BACKGROUND AND PROGRAM HISTORY

1.3 P

ROGRAM OVERVIEW AND UPDATES

1.4 S

UMMARY OF THE TRADE COMPLIANCE PROCESS

1.5 B

ENEFITS

2. PROGRAM DESCRIPTION AND REQUIREMENTS

2.1 A

PPLICANT

2.2 REQUIREMENTS AND ELIGIBILITY

2.3 E

XPECTATIONS

3. APPLICATION, PROCESSING, AND ACCEPTANCE

3.1 T

RADE COMPLIANCE PORTAL

3.2 APPLICATION

3.3 T

RADE COMPLIANCE QUESTIONNAIRE

3.4 M

EMORANDUM OF UNDERSTANDING

3.5 A

PPLICATION REVIEW

3.6 APPLICATION REVIEW MEETING (ARM)

3.7 T

RADE COMPLIANCE DECISION

3.8 F

OCUSED ASSESSMENT TO TRADE COMPLIANCE

3.9 I

NTERNAL GUIDANCE CONTROLS?

4. PROGRAM CONTINUATION REQUIREMENTS

4.1 C

ONTINUING RESPONSIBILITIES

4.2 M

ERGERS, ACQUISITIONS, AND COMPANY BUYOUTS

4.3 A

NNUAL NOTIFICATION LETTER (ANL) AND PROGRAM UPDATES

4.4 ADDING ADDITIONAL IMPORTER OF RECORD NUMBERS

4.5 T

RADE COMPLIANCE CONTINUATION REVIEW MEETING (CRM)

5. REVOCATION PROCEDURES

5.1 P

ROGRAM WITHDRAWAL

4

CTPAT Trade Compliance Handbook | October 2022

5.2 PARTNER SUSPENSION

5.3 P

ROCEDURES FOR SUSPENSION

5.4 PARTNER REVOCATION

5.5 P

ROCEDURES FOR REVOCATION

5.6 P

ARTNER RE-APPROVAL

6. APPENDIX

APPENDIX A: TRADE COMPLIANCE ELIGIBILITY QUESTIONS

A

PPENDIX B: TRADE COMPLIANCE APPLICATION QUESTIONS

A

PPENDIX C: TRADE COMPLIANCE MEMORANDUM OF UNDERSTANDING

A

PPENDIX D: GUIDANCE FOR DEVELOPING INTERNAL CONTROLS

APPENDIX E: INTERNAL CONTROL MANAGEMENT AND EVALUATION TOOL

A

PPENDIX F: RISK ASSESSMENT AND SELF-TESTING DEVELOPMENT

A

PPENDIX G: ANNUAL NOTIFICATION LETTER

A

PPENDIX H: ANL STEP BY STEP SUBMISSION

APPENDIX I: PORTAL APPLICATION PROCESS

A

PPENDIX J: CTPAT TRADE COMPLIANCE GRANT/DELETE ACCESS

5

CTPAT Trade Compliance Handbook | October 2022

HANDBOOK RECORD OF CHANGES

Version 2 Updates

October 2022

The handbook has been modified to reflect changes to forced labor requirements and to

correct several grammatical errors. Substantial updates include:

Pg 1: Updated Date to October 2022, Version 2

Pg 5: Created Handbook Record of Changes

Pg 10: Updated Disclosure benefit language

Pg 12 – Pg 16: Updated Sections 2 and 3 to include all program requirements, including

Forced Labor

6

CTPAT Trade Compliance Handbook | October 2022

Customs Trade Partnership Against Terrorism (CTPAT) Trade Compliance Program

1.

INTRODUCTION & PROGRAM MODERNIZATON

1.1

PURPOSE

The Customs Trade Partnership Against Terrorism (CTPAT) Trade Compliance program is

built on the knowledge, trust, and willingness to maintain an ongoing relationship between

Customs and Border Protection (CBP) and importers that is mutually beneficial. The goal of

the Trade Compliance program is to partner with importers who can demonstrate their

readiness to assume the responsibility of managing and monitoring their compliance through

self-assessment. Importers accepted into the CTPAT Trade Compliance program receive

tangible benefits and their participation allows CBP to redirect resources and focus on higher-

risk and unknown importers.

1.2

BACKGROUND AND PROGRAM HISTORY

The passage of the Customs Modernization Act (Customs Mod Act) in 1993 ushered in an era

of new partnership concepts between the importing community and the United States Customs

Service (now U.S. Customs and Border Protection C). Under the Customs Mod Act, CBP and

the importer share the responsibility for compliance with trade laws and regulations. The

importer is responsible for using reasonable care when declaring the value, classification, and

rate of duty applicable to entered merchandise, and CBP, through the Office of Trade, Office

of Field Operations, and other relevant stakeholders, is responsible for informing the importer

of its rights and responsibilities under the law.

In 2002, the Importer Self-Assessment (ISA) program was initiated as a voluntary approach to

trade compliance. The program was based on the premise that importers with strong internal

controls designed to ensure a high level of compliance will require fewer enforcement reviews

and less oversight. The ISA program sought to offer meaningful benefits that could be tailored

to industry needs and required that importers demonstrate readiness to assume responsibilities

for managing and monitoring their own compliance through self-assessment. The program

required that importers maintain a system of internal controls that demonstrate a sound

business operation that supports the accuracy of their import transactions.

The CTPAT Trade Compliance program is an evolution of the former ISA program with

similar goals, requirements, and improved benefits. In 2016, CTPAT launched the Trusted

Trader Strategy, which sought to integrate CTPAT Security and ISA into a consolidated

program focused on supply chain security and trade compliance. The strategy was largely

executed through the establishment of the Trusted Trader Pilot program, which provided a

forum for testing and developing new and revised program benefits and operations. Through

integration and progress made in the Trusted Trader Strategy, the program laid the foundation

for CTPAT Trade Compliance. With the full implementation of the Trade Compliance

7

CTPAT Trade Compliance Handbook | October 2022

Program, the United States Authorized Economic Operator (AEO) program now includes both

security and trade compliance.

1.3

PROGRAM OVERVIEW AND UPDATES

In addition to the above changes, CTPAT updated the program’s Minimum Security Criteria

(MSC) and integrated CTPAT Security and CTPAT Trade Compliance to create a unified AEO

program which launched in FY20. The program reflects the following outcomes as a result of

this integration:

• Global AEO Program: The program meets the highest standards of a global AEO

program because of the integration of CTPAT Security and Trade Compliance.

• New Security Requirements and Benefits: The integrated program modernized supply

chain security requirements and new benefits for CTPAT Trade Compliance.

• Impact Measurement: The program establishes clear, transparent, and measurable impact

for partners of both CTPAT Security and CTPAT Trade Compliance.

1.4

SUMMARY OF THE TRADE COMPLIANCE PROCESS

The following steps briefly summarize the CTPAT Trade Compliance application submission

requirements and review processes, all of which take place within the CTPAT Trade

Compliance Portal.

Trade Compliance Application Submission Requirements:

• An importer must be a Tier II or Tier III partner of the CTPAT Security program and in

good standing.

• An importer must meet the eligibility criteria laid out in the Eligibility Questions.

8

CTPAT Trade Compliance Handbook | October 2022

• An importer must complete a Memorandum of Understanding (MOU) and Program

Questionnaire.

Application Review Process:

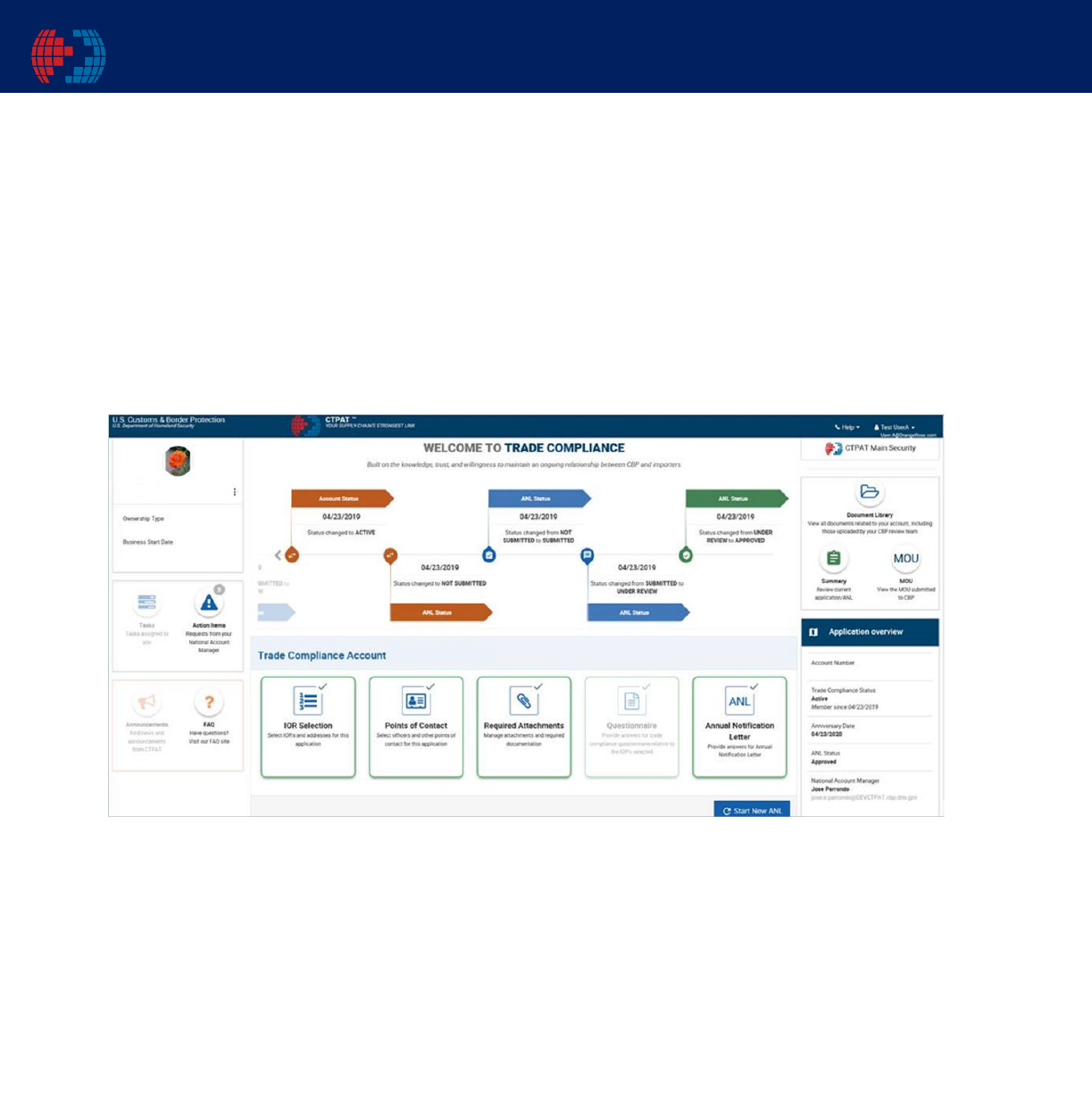

• The Trade Compliance application can be accessed through the importer’s existing

CTPAT Portal account by selecting Trade Compliance under Partnership Programs. See

Figure 1A below.

• Following the application submission, CTPAT will review the application package

within the CTPAT Trade Compliance Portal.

• CTPAT will schedule a formal meeting with the applicant, referred to as the Application

Review Meeting (ARM), which includes a risk assessment and review of the applicant’s

internal controls to determine the applicant’s readiness to assume the responsibilities for

self-assessment.

• CTPAT will establish the partnership by signing the MOU when the importer has

demonstrated readiness to assume the responsibilities for self-assessment.

• Once a partner of CTPAT Trade Compliance, the importer will receive the benefits of

both CTPAT Security and CTPAT Trade Compliance if the importer fulfills the

continuing responsibilities of the program.

Figure 1. CTPAT Trade Compliance Portal

Note: Only a company administrator can launch the CTPAT Trade Compliance Portal to create a

CTPAT Trade Compliance application.

9

CTPAT Trade Compliance Handbook | October 2022

Figure 1A. CTPAT Trade Compliance Application Process

1.5 B

ENEFITS

The CTPAT Trade Compliance program provides opportunities for importers who demonstrate a

commitment to compliance to receive related benefits that are meaningful, measurable, and

reportable. The program offers benefits to importers who demonstrate a commitment to ensuring

compliant import transactions. Below is an overview of the benefit categories one can expect to

receive:

• National Account Manager (NAM): Access to an assigned NAM, who acts as an

advisor and liaison among CBP Headquarters and the CTPAT Trade Compliance partner.

• CTPAT Trade Compliance Portal: Access to the CTPAT Trade Compliance section of

the CTPAT Portal and use of the CTPAT Portal to review and update information related

to CTPAT Trade Compliance.

• Enhanced Importer Trade Activity (ITRAC) Data Access and Automation: U.S.

Importer partners will have access to their ITRAC data directly from the CTPAT Trade

Compliance Portal.

• Expedited Rulings: Rulings and Internal Requests that are being adjudicated by the

National Commodities Division will have priority and be placed at the front of the queue

for processing within 20 days.

CTPAT Trade Compliance

10

CTPAT Trade Compliance Handbook | October 2022

• Multiple Business Units: Opportunity to apply for coverage of multiple Importer of

Record (IOR) numbers.

• Disclosure Benefit: If CBP becomes aware of errors indicating a possible violation of 19

U.S.C. 1592 or 1593a, CBP will communicate with the partner regarding such errors and

allow 30 days from the date of the communication for the partner to perform a self-

assessment and submit a written disclosure of the relevant facts to CBP. This benefit

does not apply if the matter is already a subject of an ongoing CBP investigation or if

fraud is involved.

• Removal from Focused Assessments (FA): Partners will be exempt from FA performed

by Office of Trade Regulatory Audit and Agency Advisory Services (RAAAS).

However, importers may be subject to a single-issue audit to address a specific concern.

An importer must complete an Annual Notification Letter (ANL), which allows the

partner to inform CBP of any business modifications that may have an impact on their

customs operations and to reaffirm its commitment to the requirements listed in the

CTPAT Trade Compliance MOU and other program documentation. This letter is

submitted electronically through the CTPAT Trade Compliance Portal.

Importers who are partners in CTPAT Trade Compliance also receive CTPAT Security benefits.

Examples of the CTPAT Security benefits include:

• Security Validation: As part of the validation or revalidation process, CTPAT partners

receive a comprehensive evaluation by a government Supply Chain Security Specialist

(SCSS) expert who assesses the partner’s security posture. The SCSS is an advisor that

will assist the CTPAT partner improve and maintain its security posture.

• Front of the Line Benefits: When feasible, CTPAT shipments are moved ahead of non-

CTPAT shipments for exams. Front of the Line inspection privileges apply to screening

by non-intrusive inspection (NII) equipment, examinations conducted dockside or at a

centralized examination station, and all other inspections conducted for security, trade

and/or agriculture purposes.

• Reduced Examination Rates: Reduced examination rates leading to decreased

importation times and reduced costs.

• Advanced Qualified Unlading Approval (AQUA Lane): Expedited unloading of sea

vessels through the AQUA Lane, creating an average cost savings of $3,250 per hour per

vessel for low-risk sea carriers. This benefit is applied at the ship level, not at the

container level.

CTPAT Security

11

CTPAT Trade Compliance Handbook | October 2022

• Free and Secure Trade (FAST) Lanes: Shorter wait times at the border and access to

the FAST Lanes.

• Status Verification Interface (SVI) Access: SVI Access that includes the verification of

companies yearly.

• SAFETY Act: The SAFETY Act of 2002 created liability limitations for claims resulting

from an act of terrorism where Qualified Anti-Terrorism Technologies have been

deployed. The Act applies to a broad range of technologies, including products, services,

and software, or combinations thereof. Further information regarding the SAFETY Act

of 2002 can be found at https://www.dhs.gov/science-and-technology/safety-act

• Seminars and Sponsored Events: Access to CTPAT-sponsored events such as CBP

training seminars and the CTPAT Conferences.

• Best Practices: Access to CTPAT best practices through guides, catalogs, and training

materials. CTPAT defines best practices as those that combine senior management

support, evidence of implementation, innovative business processes and technology,

documented processes, and a system of checks, balances, and accountability, also known

as the “Best Practices Framework.”

• Business Resumption: Priority entrance of goods following a natural disaster, terrorist

attack, or port closure.

• Penalty Mitigation: CBP’s Fines Penalties & Forfeitures (FP&F) will ensure that the

company's partnership status is taken into consideration and that any penalties will be

offset by the measure/level of the corrective actions taken to prevent future occurrences.

Correspondence from partners to FP&F should indicate their trusted trader status and

other pertinent information. Trusted traders requesting a penalty offset will ensure that

the cover letter to FP&F copies their NAM/SCSS.

• Mutual Recognition Arrangements (MRAs): Expedited screening with worldwide

security partners from foreign Customs administrations that have signed MRAs with the

United States.

• Marketability of CTPAT Partnership: Much like certification with other U.S.

government agencies or the International Standards Organization (ISO), CTPAT

partnership can raise a partner’s reputation and ability to secure business.

A current list of all CTPAT Security Benefits can be found here:

https://www.cbp.gov/border-security/ports-entry/cargo-security/ctpat

12

CTPAT Trade Compliance Handbook | October 2022

2 PROGRAM DESCRIPTION AND REQUIREMENTS

2.1

APPLICANTS AND ELIGIBILITY

In order to apply for the CTPAT Trade Compliance Program, Importers must:

• Be a U.S. Importer who maintains an Importer of Record Numbers (IOR numbers)

located and physically managed in the United States, or

• Be an approved non-resident Canadian importer (Canada) who is located and physically

managed in the United States.

• Have an active import history of two years or longer for all IOR numbers joining the

program

• Maintain a Tier II (validated) or Tier III (exceeding) partnership in the CTPAT Security

program, in good standing.

• Maintain evidence of no financial debt to CBP (for which the party has exhausted all

administrative and judicial remedies for relief, a final judgment, or administrative

disposition has been rendered, and the final bill or debt remains unpaid at the time of

initial application or annual renewal).

All eligibility questions are listed in Appendix A.

2.2

REQUIREMENTS

To be approved and maintain partnership for the CTPAT Trade Compliance program, Importers

must meet all general program requirements. The general program requirements include:

• Compliance with all applicable CBP laws and regulations.

• Compliance with all program requirements (see below for complete list), including the

Forced Labor requirements, as added 08/01/2022.

• Completed responses to all questionnaire questions and required attachments for

application and updates, as applicable, each year thereafter.

• Providing a company officer’s signature on the CTPAT Trade Compliance MOU at the

conclusion of the application and each year thereafter.

Specific Program Requirements and Required Attachments are included in Section 3.2 of this

document and further examples provided in Appendix D, E, and F.

2.3

EXPECTATIONS

• Members will complete all program requirements in a timely fashion.

• Members will provide trade-related updates to their NAM as needed to enable their

ability to manage the account.

13

CTPAT Trade Compliance Handbook | October 2022

• Members will submit an ANL to CBP and notify CBP of major organizational changes

(or as necessary). Members will act as positive ambassadors of the CTPAT trade

compliance program within the trade community.

3 APPLICATION, PROCESSING, AND ACCEPTANCE

3.1

TRADE COMPLIANCE PORTAL

The CTPAT Portal streamlines applications to CBP’s trade partnership programs and meets

Department of Homeland Security (DHS) mandated security requirements. The CTPAT Trade

Compliance section of the CTPAT Portal serves as a central electronic location for CTPAT

Security importers to learn more about the CTPAT Trade Compliance program and apply when

eligible. Launched in 2019, the CTPAT Trade Compliance Portal complements the existing

CTPAT Security Portal and provides an electronic and streamlined process for eligible

importers to apply and manage their status in the CTPAT Trade Compliance program. All

importers must complete the application process in the CTPAT Trade Compliance Portal to

become a partner of the Trade Compliance program.

If an importer meets the prerequisite requirements, they will be given the opportunity to begin

the application process. The first step in the application process is series of eligibility

questions (Figure 3). Once the eligibility questions are answered in full, if eligible, importers

will be directed to the CTPAT Trade Compliance application screen (Figure 3A). If an

importer is not yet eligible to apply, it will receive a CTPAT Trade Compliance ineligibility

notice (Figure 3B).

Figure 3. CTPAT Trade Compliance Eligibility Questions

14

CTPAT Trade Compliance Handbook | October 2022

All eligibility questions are available for review in Appendix A of this document.

3.2 A

PPLICATION

The Trade Compliance Application Process consists of four main components, and each is

depended on the prior in order to move forward with the application process:

1. Eligibility Questions

2. IOR Selection

3. The CTPAT Trade Compliance Questionnaire

4. The CTPAT Trade Compliance MOU

Eligibility Questions

The applicant must be able to answer yes to all eligibility questions prior to proceeding to

the questionnaire portion of the application.

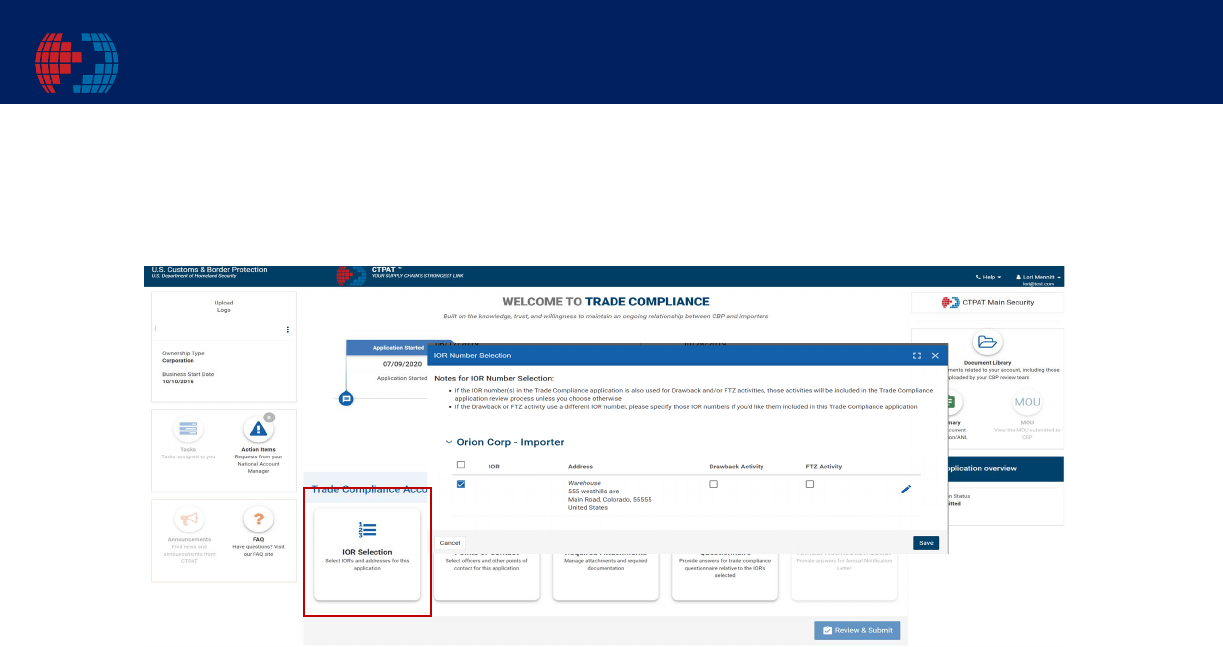

IOR Selection

All IOR numbers associated with the Importers’ CTPAT Security profile will be displayed

for selection. The Importer must carefully select which IOR numbers are included in their

Trade Compliance application and ensure the appropriate documents required cover each

IOR number.

The CTPAT Trade Compliance Questionnaire

The CTPAT Trade Compliance Questionnaire includes all of the questions and attachments

that are required to apply for the program. Responses should include applicable references

and/or inclusions for each of the IOR’s that are being submitted as part of the application.

For example, if two IOR numbers are selected and each IOR number represents a division

Figure 3B. CTPAT Trade

Compliance Ineligibility Notice

Figure 3A. CTPAT Trade

Compliance Application Welcome

Screen

15

CTPAT Trade Compliance Handbook | October 2022

with different self-testing plans, each self-testing plan must be provided with the

application.

Specific Program Requirements and Required Attachments include:

• Provide a description of the overall organization and operations that includes all members

of the compliance department or division and to whom they report.

o Required Attachment: Company Organizational Chart at the application and

corrections annually, as applicable.

• Provide a Company Logo

o Required Attachment: Company Logo

• Maintain a compliance department that oversees CBP compliance with federal regulatory

laws, regulations, and policy/guidelines.

• Implement a compliance training for internal/external parties.

o Required Attachment: Evidence of Training Program

• Track duties, fees, and import activity to ensure bond sufficiency.

• Implement a comprehensive system of internal controls including the prevention of

Forced Labor in the supply chain. Further guidance regarding a system of internal

controls may be found in Appendix D and E.

o Required Attachment: Written documentation outlining these controls (desktop

procedures)

• Maintain an audit trail from financial records to CBP declarations

• Design and execute an annual self-testing plan in response to identified risks and

implement corrective action in response to errors and internal control weaknesses.

Further guidance regarding a self-testing plan may be found in Appendix F.

o Required Attachment: Self Testing Plan

• Retain self-testing records for three (3) years.

• Partners must conduct an annual risk assessment/self-testing to identify risks compliance

with CBP laws and regulations and provide an overview of all processes during the

Annual Review Meeting

o Required Attachment: Self Testing Results

Specific Program Requirements for the inclusion of Forced Labor prevention:

• Conduct Risk Based of supply chain partners that outlines the supply chains in their

entirety and to include regions, suppliers, etc. that the importer feels poses the most risk

for forced labor, to ensure the supply chain is free from the use of Forced Labor.

(Importers are required to determine within their organization what imports are

considered high risk to their business model but should take into consideration

information that CBP provides publicly, on CBP.gov.) While no attachments are

required for the application, CBP may request unredacted proof of supply chain mapping,

regarding a particular supply chain, if at any time CBP determines the information is

needed.

16

CTPAT Trade Compliance Handbook | October 2022

• Partners must create a Code of Conduct statement that represents their position against

the use of Forced Labor within any part of their supply chain. Partners must have policies

and procedures in place that operationalize the Code of Conduct, as well as evidence of

those policies’ implementation. The Code of Conduct statement must be included in the

company's social compliance program that focuses on forced labor, as outlined in the

CTPAT Security Minimum Security Criteria.

o Required Attachment: The Code of Conduct statement must be uploaded to the

CTPAT online portal and published publicly by the partner.

• Partners must provide CBP with evidence of implementation of their social compliance

program (as required by CTPAT Security MSC). As part of the social compliance

program, partners must be able to identify the parts of its supply chain most at risk and

provide CBP with this information, if requested.

o Required documentation: Evidence of implementation of the social compliance

program. Examples of evidence include (but are not limited to) unredacted audits

of high-risk supply chains related to Forced Labor, internal training programs for

employees on identifying signs of Forced Labor, and mechanisms taken to show

the supply chain is completely free of the use of Forced Labor.

• Partners must provide training about the social compliance program requirements to their

suppliers that identifies the specific risks and helps identify and prevent forced labor in

the supply chain. The training should exemplify the company's position against Forced

Labor as stated in their Code of Conduct. Training requirements are determined by the

partner but must ensure that the suppliers business model and code of conduct represent

they will not partner with business that use Forced Labor. Proof of training must be

available to CBP upon request.

• Partners must maintain a remediation plan for their organization, in the event forced labor

is identified in their supply chains and provide this information to CBP, upon request.

This plan must include the process for disclosing the identification to CBP and outline the

necessary steps for the organization’s employees and suppliers to correct the issue.

• Partners must share best practices with the CTPAT Trade Compliance program, as

appropriate, to help mitigate the risk of forced labor.

17

CTPAT Trade Compliance Handbook | October 2022

Figure 4. Trade Compliance Application Progress Indicators

Once all sections are complete, the application package must be submitted electronically via the

portal. An authorized officer of the legal entity responsible for the CTPAT Trade Compliance

application must sign the MOU and the original copy must be submitted to CBP via the CTPAT

Trade Compliance Portal.

3.3 T

RADE COMPLIANCE QUESTIONNAIRE

The questionnaire and accompanying documentation are required to determine if the importer

has documented and implemented internal controls over its CBP-related processes. The

questions are available for review in advance in Appendix B of this document. Unsupported

responses will cause unnecessary delay of the CTPAT Trade Compliance application package.

3.4

MEMORANDUM OF UNDERSTANDING (MOU)

The MOU outlines importer and CBP responsibilities and identifies the company entities covered

by the MOU. Importers with multiple divisions may submit one MOU for each eligible entity

but must include the complete name and IOR number with all applicable suffixes. Once a

company is approved to participate in the CTPAT Trade Compliance program and elects to add a

business unit or importer of record number that was not previously covered under the original

MOU, the company must submit a revised MOU to reflect all current and additional business

units and associated IOR number(s) including the applicable suffix. MOU update requests must

18

CTPAT Trade Compliance Handbook | October 2022

be submitted in writing to CTPATTradeCompliance@cbp.dhs.gov and the company’s assigned

NAM.

An MOU can be amended if the amendment is agreed upon between the Importer and CBP. If

the amendment to an MOU includes adding or removing importer of record numbers, the

changes to the importer of record numbers must be completed by the Importer in the CTPAT

Trade Compliance portal prior to the activation/removal of benefits by CBP. To add or remove

benefits, the Importer must open the “IOR Selection” and place/remove a check mark next to the

IOR number impacted by the amendment. Because the MOU is signed annually, the update to

the MOU will be included in the following ANL process.

To submit an application and electronically sign the MOU, the highest-level compliance officer,

as listed in the Trade Compliance Portal, must submit the final application (note: this individual

will be prompted to enter their sign in password prior to the submission being accepted by CBP).

Once an application is submitted, the account will be officially under review and the applicant

will not be able to modify the information submitted. If questions from CTPAT arise during the

review process, an alert will appear in the “Action Items” section, and the applicant will receive

an email informing them of the awaiting message in the Action Items section (Figure 5).

Partners can also access business units and IOR numbers associated with the MOU by looking

up the Application Summary through the Document Library once the Application has been

submitted, or by clicking on Summary while completing the initial application (Figure 5).

An example of a completed MOU is available for review in Appendix C of this document.

19

CTPAT Trade Compliance Handbook | October 2022

Figure 5. Action Items and Document Library

4.5 A

PPLICATION REVIEW

The CTPAT Trade Compliance Team will assess the applicant’s internal controls to determine

readiness to assume the responsibilities of the Trade Compliance program and achieve

compliance with CBP regulations and laws. Internal controls must be documented, logical,

comprehensive, and likely to prevent or detect noncompliance in the identified risk areas. The

design of internal controls cannot be assessed through the evaluation of individual controls in

isolation. Rather, controls are assessed as a group by:

• Obtaining an understanding of the processes and flow of information through the entry

process.

• Determining what can go wrong within the entry process.

• Determining whether the controls are sufficient to address the instances of what can go

wrong within the entry process.

• Evaluating questionnaire responses and supporting policies and procedures.

The CTPAT Trade Compliance team then assesses the applicant’s readiness based on the

operating effectiveness of the internal controls derived from an evaluation of their design. If any

questions arise during the application review process, NAMs and applicants may communicate

through the Trade Compliance Portal (Figure 6).

Figure 6. CTPAT Trade Compliance Portal Chat Feature

4.6 A

PPLICATION REVIEW MEETING (ARM)

Part of the application process includes a two day in person ARM Meeting with the CTPAT

Trade Compliance team. Prior to scheduling the ARM, the CTPAT Trade Compliance team will

conduct a risk assessment of the applicant’s import activities related to the IOR(s) on the MOU.

This risk assessment is based on:

20

CTPAT Trade Compliance Handbook | October 2022

Company History of Trade Compliance

Company Risk Exposure

•

Compliance measurement data

•

Imports from specific suspect

manufacturers or suppliers

•

Previous penalty actions

•

Imports subject to quota, visa,

antidumping, or other CBP Priority

Trade Issues

•

Previous enforcement actions

•

Large volumes of imports under special

duty provisions or trade programs

•

Regulatory audits

•

Large volumes of imports under complex

tariff classifications

• Other information

Following the risk assessment, the CTPAT Trade Compliance team will contact the applicant to

schedule the ARM, provide the objective and expectations, and explain the evaluation process.

The team will provide the applicant with the risk areas along with up to five entry numbers to

walkthrough. Generally, the team selects a recent entry for each risk area and provides the entry

numbers to the applicant in advance.

4.7 T

RADE COMPLIANCE DECISION

Based on the information provided in the application and the information gathered prior to and

during the ARM, the CTPAT Trade Compliance team will determine whether a company should

be accepted into CTPAT Trade Compliance. The decision will be provided in one of three

forms:

A

CCEPTED: Acceptance entails a complete review of the internal CTPAT Trade

Compliance report, and the team leader will provide a synopsis of the evaluation, while

addressing questions or concerns. Applicants are formally notified of the Trade

Compliance team’s decision through the CTPAT Trade Compliance Portal. If accepted, CBP

will send the applicant an executed MOU, and a formal letter (including official ANL date and

NAM contact information) advising of acceptance into the program.

A

DDITIONAL INFORMATION NEEDED: If the CTPAT Trade Compliance team identifies

internal control inconsistencies or unresolved issues during the initial evaluation that

require more than 60 days to correct, the team will request a follow-up review. The CTPAT

Trade Compliance follow-up evaluation will re-assess the applicant’s readiness once the

applicant has undertaken corrective action. Generally, the applicant is given up to 120 days to

develop and implement corrective actions and/or provide additional documentation before the

follow-up evaluation is initiated. The team will remain in contact with the applicant during this

time to provide guidance as necessary. If there are still unresolved issues after corrective action,

21

CTPAT Trade Compliance Handbook | October 2022

the team will continue to work with the applicant to ensure that all identified inconsistencies and

issues have been addressed prior to initiating a follow-up evaluation (see Figure 7-8).

A

PPLICATION DECLINED: The CTPAT Trade Compliance team will provide a notice

indicating the reasons why the application was declined and will allow the applicant 90-

120 days to correct errors and resubmit the application with corrected actions and

corresponding proof.

Figure 7. Additional Information Needed

22

CTPAT Trade Compliance Handbook | October 2022

Figure 8. Communication for Additional Information Needed.

For any questions regarding the status of an applicant’s application, please reach out to the

Trade Compliance team by emailing CTPATTradeCompliance@cbp.dhs.gov.

3.8

FOCUSED ASSESSMENT TO TRADE COMPLIANCE

Tier II or Tier III Importers that have undergone a CBP Focused Assessment and have been

deemed by RAAAS to represent an acceptable risk to CBP within the last 12 months may be

eligible to transition into the Trade Compliance program without the Application Review

Meeting.

The Focused Assessment audit further examines a company’s internal systems for compliance

with customs laws and regulations and is more comprehensive the Trade Compliance Review

process. Qualified importers will not need to undergo the ARM and will need to submit a Trade

Compliance MOU and the organization’s self-testing plan. The importer may apply through the

Trade Compliance Portal and will declare their eligibility based on the Focused Assessment as

part of the Trade Compliance Questionnaire. More information regarding this process can be

found in the Customs Bulletin and Decisions, Vol. 46, No. 44, dated October 24, 2012.

3.9

INTERNAL GUIDANCE CONTROL

To assist importers in developing and evaluating their system of internal controls of CBP

operations, importers should review “Guidance for Developing Internal Controls” (Appendix D),

which is an explanation of components of an internal control program ideal for small importers,

and the “Internal Control Management and Evaluation Tool” (Appendix E), a comprehensive

guide appropriate for large importers with complex organization structures. These documents

are tools to help determine how well a company’s internal control system is designed and

functioning, and helps determine what, where, and how improvements may be implemented.

CTPAT Trade Compliance participants must maintain an internal control system that

demonstrates the accuracy of CBP transactions with two specific processes:

1. Internal controls designed to ensure compliance in import transactions, and

2. An audit trail from accounting records and payments to entry records or an alternate

system that ensures accurate values are reported to CBP.

The applicant must establish, document, and implement internal controls, conduct self-testing

(Appendix F) of transactions based on risk, maintain results of testing for three years, and make

appropriate adjustments to internal controls

23

CTPAT Trade Compliance Handbook | October 2022

Internal controls developed and implemented by one company may vary considerably between

companies due to:

• Variations in company mission, goals, and objectives

• Differences in environment and the manner in which they operate

• Variations in degree of organizational complexity

• Differences in company histories and culture

• Differences in the risks companies face and are trying to mitigate

24

CTPAT Trade Compliance Handbook | October 2022

4 PROGRAM CONTINUATION REQUIREMENTS

4.1

CONTINUING RESPONSIBILITIES

CTPAT Trade Compliance participants are responsible for continuing compliance with program

requirements. Responsibilities are as follows:

• Maintain partnership in CTPAT Security

• Continue to comply with all applicable CBP laws and regulations

• Maintain an internal control system

• Make appropriate disclosures to CBP (such as post summary corrections and

misclassification errors)

• Submit an ANL to CBP to reaffirm the participant’s continuation in meeting the

program’s requirements through the CTPAT Trade Compliance Portal

• Notify CBP of major organizational changes as soon as possible through the CTPAT

Trade Compliance Portal by submitting a new organizational chart, if the company is not

in the CBP approval process. If the company is in the CBP approval process, the

company should email CTPATTradeCompliance@cbp.dhs.gov for assistance.

4.2

MERGERS, ACQUISITIONS, AND COMPANY BUYOUTS

CTPAT Trade Compliance participants in a merger, acquisitions, company buyouts, or any other

corporate restructuring that includes adding/subtracting importer of record numbers to their

CTPAT portfolio must be reported to the CTPAT Security SCSS, the CTPAT Trade Compliance

National Account Manager, and CTPATTradeCompliance@cbp.dhs.gov via an official letter on

company letterhead. These individuals will work together to determine how to advise the

company moving forward. Because these scenarios are often complicated, each case will be

handled on a case-by-case basis.

4.3

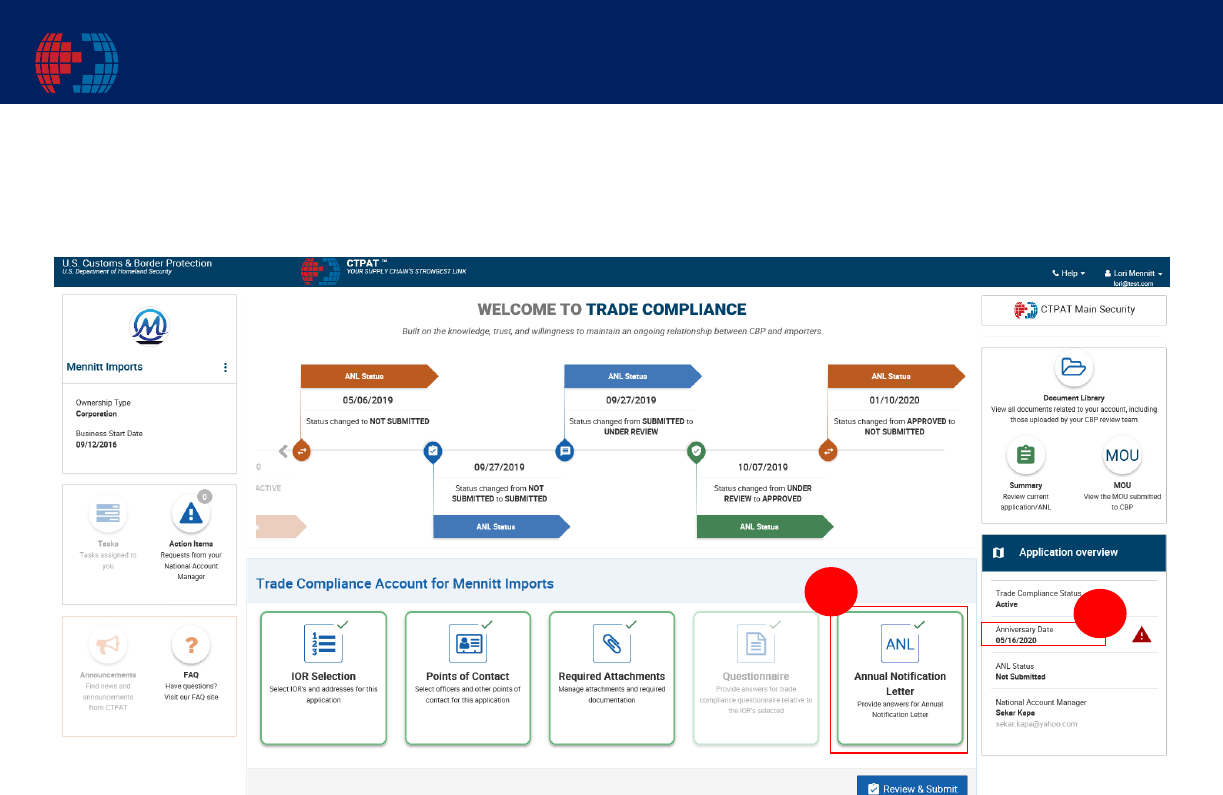

ANNUAL NOTIFICATION LETTER (ANL) AND PROGRAM UPDATES

The participants must provide written notification annually or following any significant change

to their trade compliance program or operations to show that they are continuing to meet the

requirements of the CTPAT Trade Compliance program. ANLs are due every year upon the

anniversary date of which the company was approved in the CTPAT Trade Compliance program.

The ANL should be submitted to CBP within 30 days of the applicant’s acceptance anniversary.

Importers will use the Trade Compliance Portal to submit their ANL information. This date is

reflected in the CTPAT Trade Compliance portal under the application overview section.

25

CTPAT Trade Compliance Handbook | October 2022

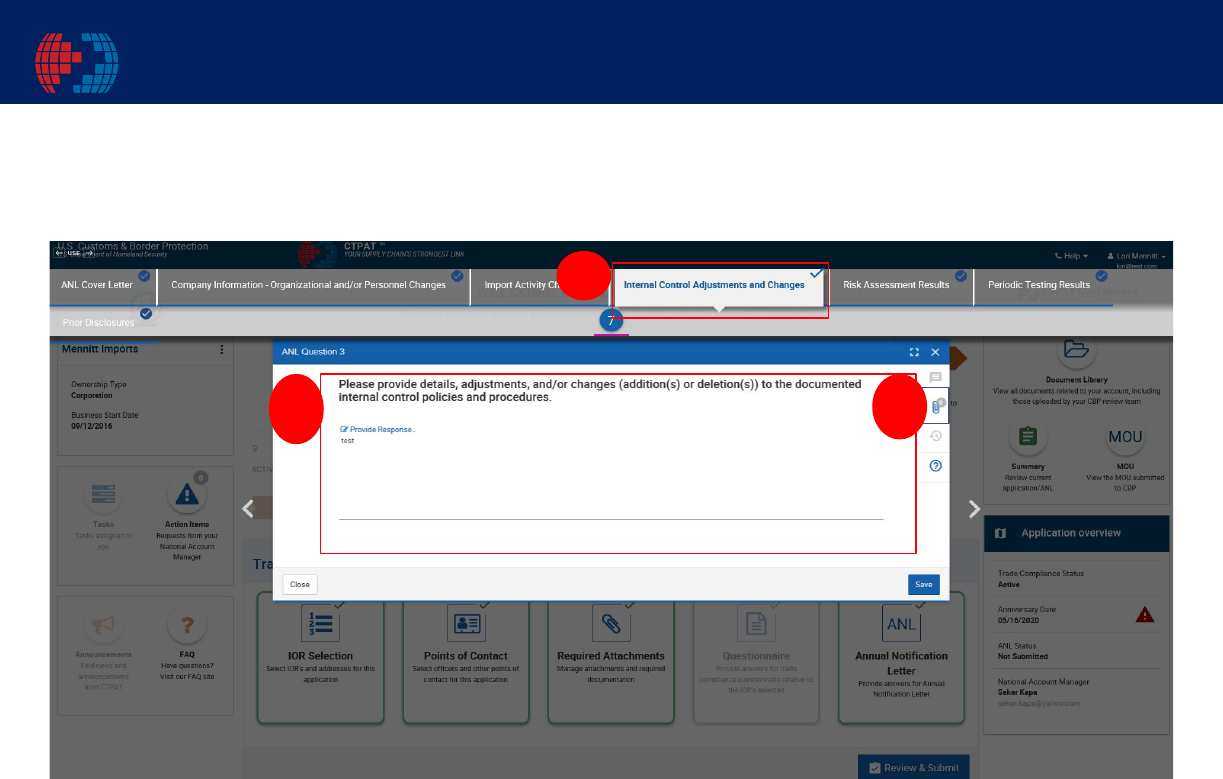

The information submitted in the ANL is captured in six categories and must be submitted

through the Trade Compliance Portal:

1. Company Information: Organizational and/or Personnel Changes

2. Import Activity Changes

3. Internal Control Adjustments and Changes

4. Risk Assessment Results

5. Periodic Testing Results

6. Prior Disclosures, Post Summary Corrections, and Post Entry Amendments

Figure 9. ANL Status Screen

For a complete guide to the ANL process including guidance on questions and required

responses, see Appendix G and Appendix H in this document.

Extensions for the ANL due date must be submitted in advance of the due date to

CTPATTradeCompliance@cbp.dhs.gov with a copy to the importer’s assigned NAM. The

request must include the amount of time needed to complete the extension and a valid reason

why the extension is needed. Extension requests are not guaranteed and are considered on a

case-by-case basis.

26

CTPAT Trade Compliance Handbook | October 2022

4.4 ADDING ADDITIONAL IMPORTER OF RECORD NUMBERS

This section does not apply to situations where mergers, acquisitions, or company purchases

occur. Please reference Section 4.2 of this document for further information regarding these

scenarios.

Companies requesting to add additional IOR numbers to their CTPAT Trade Compliance

account must send an official letter on company letterhead to their CTPAT Trade Compliance

National Account Manager and the CTPATTradeCompliance@cbp.dhs.gov mailbox. The letter

must include the additional Importer of Record numbers along with a complete justification of

the addition.

All CTPAT Security processing must be completed, approved, and added to the Importers

CTPAT portal account prior to proceeding with CTPAT Trade Compliance. Once approved by

CTPAT Trade Compliance, the Importer must include the new Importer of Record number on

the “IOR selection” in the portal, as this will ensure all Importer or Record numbers will be

referenced on the signed MOU. The company must also include updates to the company

handbook, internal control manuals, and self-testing plans to reflect added Importer or Record

number(s) during the next Annual Notification submission period.

National Account Managers and/or the CTPAT Trade Compliance Branch are available to assist

companies with the addition of new Importer of Record numbers. It is highly suggested that

companies utilize this assistance to avoid inadvertently removing benefits for any Importer of

Record numbers in the company’s profile.

4.5

TRADE COMPLIANCE CONTINUATION REVIEW MEETING (CRM)

After an importer has been in the CTPAT Trade Compliance program for five (5) years, a

Continuation Review Meeting (CRM) may be considered. However, risk indicators or non-

compliance with program requirements may warrant a CRM prior to the 5-year period. The

purpose of the CRM is to assess whether the participant is continuing to fulfill the CTPAT Trade

Compliance program requirements. If CBP identifies weaknesses or noncompliance, the

participant will be notified as early as possible and can correct any issues.

CBP will remove participants from the program for any issues that pose a significant risk to

compliance with CBP laws and regulations and/or failure to demonstrate they have fulfilled

program requirements. The Trade Compliance team will decide whether the company may

continue to participate.

27

CTPAT Trade Compliance Handbook | October 2022

5. PROGRAM WITHDRAWAL & REVOCATION PROCEDURES

5.1 Program Withdrawal

An importer (or an IOR number within a company profile) reserves the right to withdraw from

the program at any time. If a company determines it no longer wishes to participate in the

CTPAT Trade Compliance program, it must notify its NAM via email using a memo on official

company letterhead. The company’s assigned NAM will initiate the formal withdrawal process.

Once withdrawn from the CTPAT Trade Compliance program, the assigned NAM will be

removed from the company profile and will no longer be available to support the company. The

Trade Compliance Branch will provide the company a formal notification through a letter

submitted to them in their CTPAT Trade Compliance account.

5.2 Partner Suspension

CTPAT Trade Compliance partnership is dependent on satisfactory partnership of the CTPAT

Security program. If an Importer (or any IOR number within the company profile is suspended

from CTPAT Security, the partner will be automatically suspended from CTPAT Trade

Compliance. When this occurs, the company will be notified through the CTPAT Trade

Compliance Portal. From there, CTPAT is committed to working with the importer to take the

proper steps required to reinstate partnership, if applicable.

CTPAT Security partnership is not dependent on Trade Compliance partnership and therefore a

company (or any IOR number associated with the company) can be suspended from the Trade

Compliance program but remain in the CTPAT Security Program.

CBP may suspend participants from the CTPAT Trade Compliance Program for reasons

including, but not limited to:

• Suspension from the CTPAT Security Program

• Failure to comply with all applicable CBP laws and regulations

• Failure to maintain the internal control system, execute an annual self-testing plan,

and perform annual risk assessments

• Failure to share appropriate disclosures with CBP

• Failure to reaffirm that the partner is meeting program’s requirements by failing to

submit an ANL through the CTPAT Trade Compliance Portal within 30 days of the

anniversary of the program acceptance date

• Failure to notify CBP of major organizational changes through the CTPAT Trade

Compliance Portal as soon as possible, but not later than the submission of the ANL

28

CTPAT Trade Compliance Handbook | October 2022

5.3 Procedures for Suspension

Typically, each suspension is preceded by extensive outreach efforts to provide the company

with the opportunity to demonstrate compliance with program requirements. In addition, after

suspending the company’s benefits, additional outreach efforts are conducted to help the partner

address gaps, vulnerabilities, or weaknesses that lead to the proposal of suspension. If CTPAT

determines there is a basis for proposing the suspension of a participant, a notice of proposed

suspension will be sent through the CTPAT Trade Compliance Portal to apprise the participant

of the facts that warrant their suspension. The participant may respond to the proposed

suspension through the portal. The participant’s response should be submitted within 60 days of

the date of the notice. The response should address the facts outlined in the notice and how

compliance will or has been achieved. CBP will issue a final written decision on the proposed

suspension after the 60-day response period has closed. CTPAT will continue to work with the

company to take the proper steps required to reinstate partnership, if applicable.

During the suspension period, the importer is expected to continue to comply with the program

requirements, including the submission of the ANL if the anniversary date falls within the

suspension period.

5.4 Partner Revocation

CTPAT may revoke participants from the CTPAT Trade Compliance Program for reasons

including but not limited to:

• Participation in the program was obtained through fraud or misstatement of f act

• Participant is convicted of any felony or has committed acts that would constitute a

misdemeanor or felony involving theft, smuggling, or any theft-connected crime

• Participant refuses to cooperate with CBP in response to an inquiry, audit, or

investigation

• Participant fails to fulfill the terms of the MOU

• CRM concludes the participant is not meeting the requirements of the program

If CTPAT determines a removal from the program is warranted, Trade Compliance partners will

be removed from the program in the following ways:

1. Lack of Compliance with MOU: If the Trade Compliance branch determines that the

account (or any IOR number associated to the company) is not fulfilling the terms of

the MOU, the account will be subject to removal from CTPAT Trade Compliance. If

the account wishes to reapply in the future, the NAM will work with the account on an

action plan to put the account in a position to assume the responsibilities of CTPAT

Trade Compliance.

29

CTPAT Trade Compliance Handbook | October 2022

2. Program Suspension: If a company (or any IOR number associated with a company)

is suspended from CTPAT Security, the partner will be automatically suspended from

CTPAT Trade Compliance. When this occurs, the company will be notified through

the CTPAT Trade Compliance Portal. From there, CTPAT will work with the

company to take the proper steps required to reinstate partnership, if applicable.

3. Non-Approval and Lack of Desire for Participation: If the account is not approved to

participate in Trade Compliance or determines it no longer wants to continue to

participate, the Trade Compliance Branch will send the partner a letter indicating that

the company is removed from the program and will no longer be assigned a NAM.

4. Immediate Removal: In cases where public health or safety interests are concerned, a

removal from the program may be effective immediately as a final action.

5.5 Procedures for Revocation

If CBP determines there is a basis for the removal of a participant, a notice of proposed removal

will be sent through the CTPAT Portal to apprise the participant of the facts that warrant their

removal. The participant may respond to the proposed removal through the portal. The

participant’s response should be submitted within 60 days of the date of the notice. The response

should address the facts outlined in the notice and how compliance will or has been achieved.

CBP will issue a final written decision on the proposed removal after the 60-day response period

has closed. Once a participant has been removed from the program, the company will be eligible

to reapply at the discretion of CTPAT Leadership. In cases where public health or safety

interests are concerned, a removal from the program may be effective immediately as a final

action.

5.6 Partner Re-Approval

CTPAT Trade Compliance partners who withdraw from the program or are removed from the

program are eligible to reapply. If a participant has been removed from the program, the

company will be eligible to reapply at the discretion of CTPAT Leadership.

Q

UESTIONS

For any additional questions about the CTPAT Trade Compliance program, please visit

the CTPAT Website, or reach out to the NAM if assigned one, or by emailing

CTPATTradeCompliance@cbp.dhs.gov.

30

CTPAT Trade Compliance Handbook | October 2022

6. CTPAT TRADE COMPLIANCE HANDBOOK APPENDIXES

Appendix A: Trade Compliance Eligibility Questions

#

Eligibility Questions / Requirements

Yes

No

1.

Do you have a general authority to do business without requiring the approval of

another person outside the United States or Canada?

2.

Are you an active United States importer or Non-Resident Canadian importer

who meets the requirements set forth in 19 CFR Part 141, including in particular,

sections 141.17 and 141.18?

3.

Do you maintain separate books and records for your United States / Canada

operations, prepare separate financial statements, maintain accounts for the

imported goods, and are you responsible for payment of import duties and taxes?

4. Do you possess a valid continuous importation bond filed with CBP?

5.

Are you willing to complete a Memorandum of Understanding (MOU) and

Trade Compliance Questionnaire?

6.

Do you maintain an internal control system that is designed to provide assurance

of compliance with CBP laws and regulations?

7.

Do you perform annual risk assessments to identify risks to compliance with

CBP laws and regulations?

8.

Do you maintain and make appropriate adjustments to the system of internal

controls?

9.

Have you designed an annual self-testing plan in response to identified risks? Do

you implement corrective action in response to errors and internal control

weaknesses disclosed by self-testing?

10.

Do you maintain an audit trail of financial records to CBP declarations, or an

alternate system that ensures accurate values are reported to CBP?

11.

Do you make appropriate disclosures through a prior disclosure, reconciliation,

post summary corrections, or a supplemental letter to CBP?

12.

Are you willing to submit an Annual Notification Letter (ANL) certifying that

you continue to meet CTPAT Trade Compliance requirements as listed in the

Handbook?

13.

Do you agree to notify CBP of all major organizational changes?

31

CTPAT Trade Compliance Handbook | October 2022

Appendix B: Trade Compliance Application Questions

I. Company Information

1. Company Information (Required Document)

• Date Prepared:

• Company Name:

• Business Address:

• Phone Number:

• Company Website:

• Company Type: Public or Private

• Business Fiscal Year:

• Name, Title, Phone Number, and e-mail address of company contact:

• Please describe the overall organization/operating structure and provide

organizational chart of the company.

2. IOR(s) Numbers:

• Note, if the IOR number (s) in the Trade Compliance application is also used for

Drawback and/or FTZ activities, those activities will be included in the Trade

Compliance application review process unless you choose otherwise.

• If the Drawback or FTZ activity use a different IOR number, please specify those

IOR numbers if you’d like them included in this Trade Compliance application.

• Provide the names and addresses of any related f oreign and/or domestic

companies, such as the company’s parent, sister, subsidiaries, or joint ventures,

etc.

3. Do all of your company’s business units/subsidiaries operate under a centrally controlled

customs compliance policy/system? (Y/N)

• If no, describe how the compliance system operates in other

divisions/subsidiaries. (Open Text)

4. Does your company maintain an in-house compliance department dedicated to

maintaining and updating your company’s operations in adherence to government

regulations, laws, executive orders and procedures that will affect your CBP operations?

(Y/N)

• If so, please provide details on management and operational activities performed

by this department. (Required Document—Organizational Chart/ Free Text)

5. If not in house (per #4 above), do you have a contract with a CBP brokerage house or

consulting service to provide this advisory assistance? (Y/N)

• Would you like this company/firm to participate with you in the Trade

Compliance application/review process? If yes, which company/firm? (Y/N –

Free Text)

32

CTPAT Trade Compliance Handbook | October 2022

6. Does the company have compliance training (external, internal, or both) that provides

pertinent training for its internal compliance office and other departments that are

involved with CBP related activities? (Y/N)

• If so, evidence of the training program, such as a training log that describes

course taken and attendees, must be included in the application. (Y/N –

Required Document)

7. Is your company applying to Trade Compliance due to successfully completing a

Focused Assessment (FA)? If so, please provide your invitation letter from the Trade

Compliance Branch. (Y – Required Document)

II. Import Activity

8. Does the company monitor/track its annual duties, fees, and taxes paid to CBP to ensure

bond sufficiency?

• If yes, briefly describe how this is done and include how payments of duties and

fees are made? (i.e. PMS, ACH, Debit, Credit or by Broker)? (Y/N – If Y,

Supporting Text Required)

9. Has the company’s surety been required to pay a claim on its behalf in the past 5 years?

• If yes, please provide claim details. (Y/N – If Y, Supporting Text Required)

10. Does the company own, or hold a license to use, trademarks, or copyrights for goods it

imports into the United States? (Y/N)

• If yes, please identify the imported merchandise that falls under the license

agreement or pertains to the company owned intellectual property rights (IPR).

(If Y, Supporting Text Required)

11. Does the company import products that are subject to an exclusion order from the

International Trade Commission (ITC)? (Y/N)

• If yes, please list them. (If Y, Supporting Text Required)

III. System of Internal Controls

12. Does your company have a written, comprehensive system of internal controls for its

import processes that is consistent with the five interrelated components of internal

control as defined by Committee of Sponsoring Organizations of the Treadway

Commissions (COSO) published report entitled “Internal Control-Integrated

Framework”: (Y/N – Check)

• Control environment

• Risk assessment

• Control activities

• Information and communication

33

CTPAT Trade Compliance Handbook | October 2022

• Monitoring

13. Does the company’s written internal control procedures focus on ensuring trade

compliance for the following areas? (Y/N Check all of the applicable options below.

Documents Required)

• Value

o All elements of costs are included.

o All additions to the price paid or payable such as assists are also

included etc.

• Drawback

• Foreign Trade Zone

• Classification

• Country of Origin

• Free Trade Agreements

• AD/CVD

• Forced Labor

• Other

IV. Risk Assessment Results

14. Is your company prepared to provide risk assessment testing results to include areas of

potential risks? (Y/N)

• If so, please summarize the risk management and assessment process. (Free Text)

V. Periodic Testing Results

15. Do the company’s internal control procedures include a process for conducting periodic

self-testing to include reporting results and implementing corrective actions? (Y/N)

• If so, please provide details. (Free Text)

16. Do you make adjustments to your internal control system when tests or other information

shows a need for improvement with your compliance procedures? (Y/N)

• If so, please provide details. (Free Text)

17. Does your internal control process include a record keeping system that maintains

evidence of testing and testing results for at least three years and enables you to submit

documents in a timely manner to CBP upon request, to include tests and test results?

(Y/N)

• If so, please provide details. (If Y, Supporting Text Required)

VI. Prior Disclosures

34

CTPAT Trade Compliance Handbook | October 2022

18. What processes do you have in place to initiate appropriate disclosures to CBP when

issues are discovered through your self-testing?

• Provide Response. (Free Text)

VII. Government Agency Affiliation

19. Do you participate in any other partnership programs with any other government

agencies? (Check one or more of the applicable options below) (Y/N Check One)

• FDA

• CPSC

• Not Applicable

• Other

35

CTPAT Trade Compliance Handbook | October 2022

Appendix C: Trade Compliance Memorandum of Understanding (MOU)

U.S. Customs and Border Protection

Trade Compliance Program

Memorandum of Understanding

This Memorandum of Understanding (MOU) is the document that describes very broad concepts

of mutual understanding, goals and plans shared by the parties. As such, (company name)

requests to participate in the Trade Compliance program (program) (formerly the Importer Self-

Assessment Program). This agreement is made between (company name) hereinafter referred to

as the account and U.S. Customs and Border Protection, hereinafter referred to as CBP. We

acknowledge that the primary objective of the Program is to maintain a high level of trade

compliance with customs laws through a cooperative CBP/ account partnership.

The account and CBP recognize the need to jointly address trade issues in order to maintain an

efficient and compliant import process. This MOU is designed to strengthen the account’s

ability to maintain a high level of compliance with CBP requirements through effective internal

controls of CBP activities and a cooperative interchange of ideas and information with CBP.

The program represents an opportunity to establish a joint informed compliance effort, in a

process built on knowledge, trust, and the desire to maintain an ongoing CBP/ account

relationship. The program provides CBP with the means to recognize and support the account’s

efforts to achieve compliance and offers the account the opportunity to demonstrate compliance

and receive related benefits.

This MOU does not exempt the account from statutory penalties or sanctions in the event of non-

compliance. However, the extent to which the account has shown compliance with the terms of

this MOU will reflect favorably and may be a mitigating factor toward any CBP decision or

recommendation on final case disposition.

The following are the account and CBP’s responsibilities under this MOU. More specific

information detailing the roles and responsibilities of the account and CBP are provided in the

CTPAT Trade Compliance Program Handbook.

ACCOUNT ROLES AND RESPONSIBILITIES

• Be a CTPAT partner;

• Complete the Trade Compliance Memorandum of Understanding and Questionnaire;

• Comply with all applicable CBP laws and regulations;

• Develop, update, and maintain an internal control system that is designed to provide

reasonable assurance of compliance with CBP laws and regulations;

36

CTPAT Trade Compliance Handbook | October 2022

• Conduct analysis and perform annual risk assessments to identify any risks related to

compliance with CBP laws, regulations and related transactions;

• Design and execute a periodic self-testing plan in response to identified risks;

• Implement corrective actions in response to errors and internal control weaknesses disclosed

by self-testing:

Maintain results of testing for three years and make test information available to CBP

upon request;

Make the necessary adjustments to internal controls in a timely manner;

Maintain an audit trail of financial records related to CBP declarations or an alternate

system that ensures values reported to CBP are accurate;

• Make accurate and complete disclosures;

• Notify CBP of major organizational changes as soon as possible;

• Immediately inform CBP of incidents related to Priority Trade Issues (PTIs) which represent

high-risk areas that can cause significant revenue loss, harm the U.S. economy, or threaten

the health and safety of the American people;

• Timely submit an Annual Notification Letter (ANL) to CBP in accordance with the

requirements listed in the Trade Compliance program Handbook.

CBP ROLES AND RESPONSIBILITIES

• The account will be assigned a National Account Manager (NAM).

• CBP will provide guidance related to compliance, risk assessments, internal controls, etc.

providing the account with greater business certainty; The account will be removed from the

RAAAS audit pool established for focused assessments.

• The account will be removed from RA’s audit pool for Drawback and Foreign Trade Zones if

they requested to have these programs included in the Trade Compliance program.

• The audit exemptions will apply to each specific area when it is determined that adequate

internal controls are in place, to ensure compliance with CBP laws and regulations.

However, accounts may be subject to on-site examinations for single-issue reviews.

• The account will be able to obtain their Importer Trade Activity (ITRAC) data via the

CTPAT Portal on a quarterly basis.

• If CBP becomes aware of errors indicating a possible violation of 19 U.S.C. 1592 or 1593a,

CBP will communicate with the partner regarding such errors and allow 30 days from the

date of the communication for the partner to perform a self-assessment and submit a written

disclosure of the relevant facts to CBP. This benefit does not apply if the matter is already a

subject of an ongoing CBP investigation or if fraud is involved.

• The account participation in the Trade Compliance program may be considered as a

mitigating factor in the disposition of assessed civil penalties or liquidated damages cases.

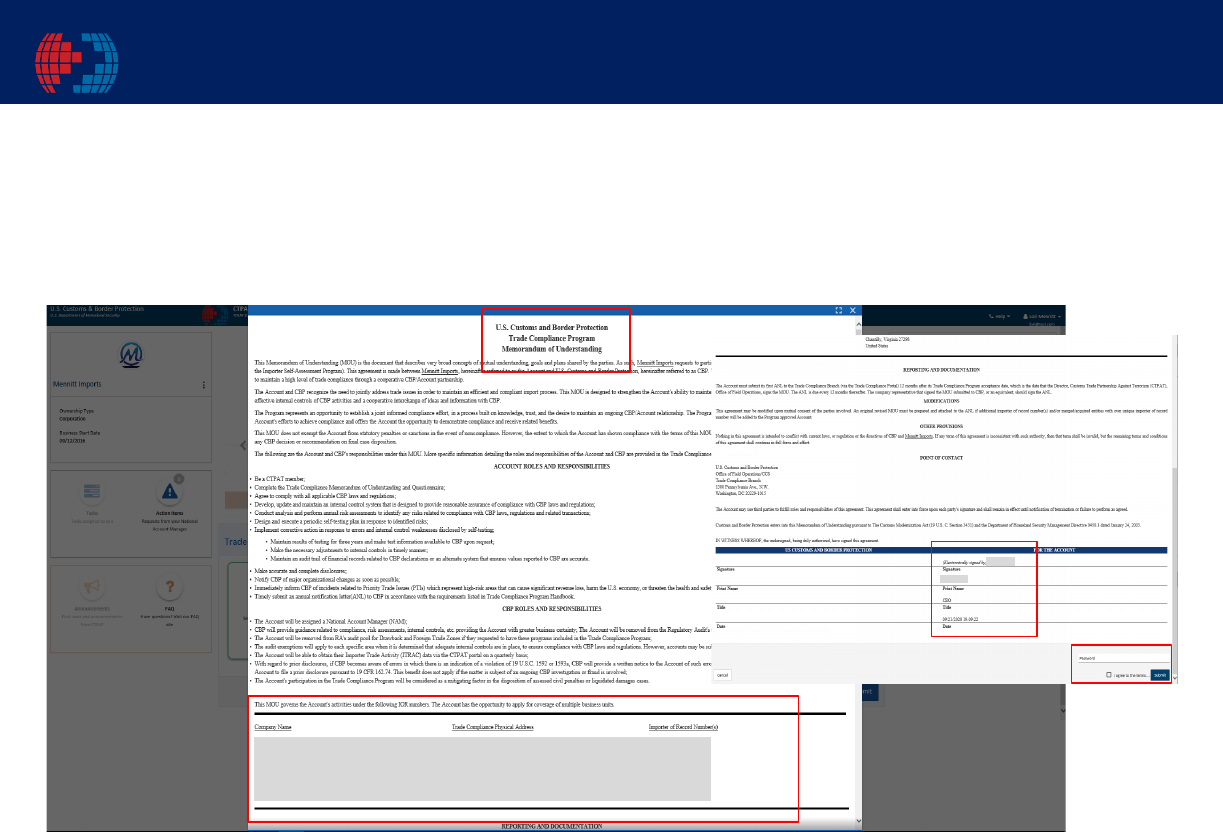

This MOU governs the account activities under the following IOR numbers. The account

has the opportunity to apply for coverage of multiple business units.

37

CTPAT Trade Compliance Handbook | October 2022

Company Name Trade Compliance Office Physical Importer of Record

Address Number (s)

REPORTING AND DOCUMENTATION

The account must submit its first ANL to the Trade Compliance Branch (via the Trade

Compliance Portal) 12 months after its Trade Compliance program acceptance date, which is the

date that the Director, Customs Trade Partnership Against Terrorism (CTPAT), Office of Field

Operations, signs the MOU. The company representative that signed the MOU submitted to

CBP, or an equivalent, should sign and submit the ANL.

MODIFICATIONS

This agreement may be modified upon mutual consent of the parties involved. An original

revised MOU must be prepared and attached to the ANL if additional importer of record

number(s) and/or merged/acquired entities with own unique importer of record number will be

added to the program approved account.

OTHER PROVISIONS

Nothing in this Agreement is intended to conflict with current laws, regulations, or the directives

of CBP and ____ (company name) ____. If any term of this agreement is inconsistent with such

authority, then that term shall be invalid, but the remaining terms and conditions of this

agreement shall continue in full force and effect.

POINT OF CONTACT

U.S. Customs and Border Protection

Office of Field Operations/Cargo and Conveyance Security

Trade Compliance Branch

1300 Pennsylvania Ave., N.W.

Washington, DC 20229-1015

The account may use third parties to fulfill roles and responsibilities of this agreement. This

agreement shall enter into force upon each party’s signature and shall remain in effect until

notification of termination or failure to perform as agreed.

38

CTPAT Trade Compliance Handbook | October 2022

Customs and Border Protection enters into this Memorandum of Understanding pursuant to The

Customs Modernization Act (19 U.S. C. Section 3431) and the Department of Homeland

Security Management Directive 0450.1 dated January 24, 2003.

IN WITNESS WHEREOF, the undersigned, being duly authorized, have signed this agreement.

FOR U.S CUSTOMS AND BORDER FOR THE ACCOUNT

PROTECTION

______________________ ______________________

Signature Signature

______________________ ______________________

Print Name Print Name

______________________ ______________________

Director, CTPAT Title

______________________ ______________________

Date Date

39

CTPAT Trade Compliance Handbook | October 2022

Appendix D: Guidance for Developing Internal Controls

GUIDANCE FOR DEVELOPING INTERNAL CONTROLS

The following guidance is provided to assist a company in developing internal controls.

Please note that the list is not all-inclusive and that CTPAT Trade Compliance partners should

design their program to fit the circumstances, conditions, and risks relevant to the situation of

the company. A more extensive guide and management tool is available in Appendix G.

An effective system of internal control should contain the following components:

Control Environment: The company establishes and maintains an environment that

supports CBP compliance, including fostering a system that supports compliance,

maintaining competent personnel, and maintaining an organizational structure that

supports compliance.

Management conveys the message that integrity and ethical values must not be

compromised. Management and employees have a positive and supportive attitude

toward CBP internal controls and conscientious management of CBP- related operations.

Management has a philosophy and operating style that is appropriate to the development

and maintenance of effective internal controls for CBP, as evidenced by the following:

•

A commitment to the competence of personnel responsible for CBP-related activities.

The company educates and trains employees about CBP programs that are affected by

the employees’ jobs. The employees should be educated on the importance of CBP

activities related to or affected by their job and the possible impact of errors. The

employees should be trained to successfully perform the job.

•

The company’s organizational structure and the way in which it assigns authority and

responsibility for CBP operations contribute to effective internal controls.

•

The company’s management cooperates with auditors, does not attempt to hide

known problems from them, and values their comments and recommendations.

Risk Assessment: The Company identifies risks to the goal of CBP compliance, analyzes

them for possible effects, and designs control activities to manage those risks. The company

has established clear and consistent company- wide objectives and supporting activity-level

objectives related to CBP activities. The following evidence risk assessment activities:

•

Management has made a thorough identification of risks pertaining to CBP activities,

from both internal and external sources, which may affect the ability of the company

to meet those objectives.

•

An analysis of those risks has been performed, and the company has

appropriate approach for risk management.

•

Mechanisms are in place to identify changes that may affect the company’s

ability to achieve its missions, goals, and objectives related to CBP activities.

40

CTPAT Trade Compliance Handbook | October 2022

Control Activities: The company documents and implements policies and procedures and

other control activities to ensure complete and accurate reporting to CBP as well as

compliance with other CBP requirements. Procedures should include the correct reporting

of information for value, classification, special trade programs, special duty provisions, and

other CBP issues such as quota, antidumping duties, and countervailing duties.

Appropriate policies, procedures, techniques, and control mechanisms must be developed and

in place to ensure adherence to established CBP requirements. The following evidence

control activities:

•

Proper control activities have been developed and documented for each of the company’s

CBP activities.

•

The control activities identified as necessary are actually being applied properly.

•

All documentation of transactions and records are properly managed,

maintained, and reviewed, as necessary.

•

Control procedures are reviewed and revised, as necessary.

Information and Communication: The company establishes and maintains processes to

ensure that relevant, reliable information pertaining to CBP is recorded and communicated

through the organization to those who need it and that information provided to CBP is

complete and accurate.

Information systems are in place to identify and record pertinent operational and financial

information relevant to CBP activities. Management ensures that effective internal

communications take place. The company employs various forms of communications

appropriate to its needs and manages, develops, and revises its information systems in a

continual effort to improve communications. The following evidence effective information

and communication f or CBP:

•

Appropriate information is identified, recorded, and communicated to management

responsible for CBP activities and others within the company who need it, in a form

that enables them to carry out their duties and responsibilities efficiently and

effectively.

•

Effective external communications occur with groups that can affect the achievement of

the company’s missions, goals, and objectives related to CBP activities.

•

Individual roles and responsibilities for CBP activities are communicated through

policy and procedure manuals.

Monitoring: The Company monitors its CBP activities to assess the quality of performance

over time and ensure that issues and deficiencies are promptly resolved and that procedures

are corrected to prevent recurrence. Monitoring will include some testing of CBP

compliance on a periodic basis. Results of testing will be maintained for three years and will

41

CTPAT Trade Compliance Handbook | October 2022

be provided to CBP on request. Company internal control monitoring assesses the quality of

performance related to CBP activities over time. The following evidence monitoring:

•

Procedures to monitor internal controls occur on an ongoing basis as a part of the

process of carrying out regular activities.

•

Separate evaluations of internal controls are periodically performed, and

deficiencies found are investigated.

•

Procedures are in place to ensure that the findings of all audits and other reviews are

promptly evaluated, decisions are made about the appropriate response, and actions

are taken to correct or otherwise resolve the issues promptly.

If you would like to know more about risk assessment and internal controls related to CBP